In my view, Fed policy during 2020 has been contractionary, as both NGDP and price level forecasts have declined. Many people prefer to look at monetary policy in a different way, focusing on the money that the Fed injects into the banking system. And by that measure, policy has indeed been expansionary.

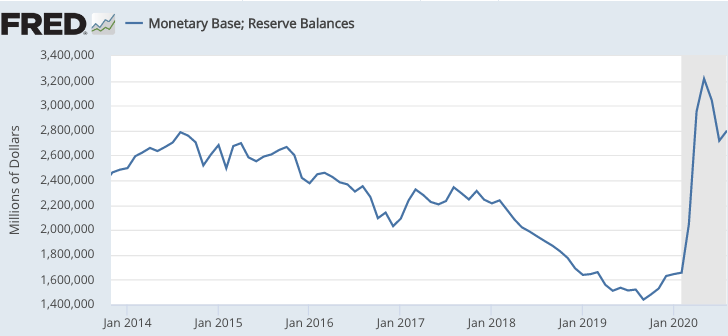

But perhaps not as expansionary as you might assume. Six years ago, total commercial bank reserves balances at the Fed totaled $2.8 trillion. The most recent data indicates that total reserve balances at the Fed are $2.8 trillion. That’s no growth in 6 years, even in nominal terms. (Reserves have obviously declined as a share of GDP.)

Again, both the overall monetary base and the part of the base held as bank reserves at the Fed have increased sharply this year, after declining from a peak in August 2014. But the current level of reserves is not extraordinary; at least not in the way that this year’s budget deficit is historically unprecedented. (The deficit rose from below $500 billion in 2014 to $3.1 trillion this year.)

The Fed could have injected vast sums of money into the US economy, many times more than they injected during the Great Recession. They chose not to do so for reasons that I cannot explain. Someone should ask Jay Powell, especially given that he’s calling for even more trillions in fiscal stimulus. Monetary stimulus does not add a penny to the national debt.

READER COMMENTS

marcus nunes

Oct 11 2020 at 9:08pm

marcus nunes

Oct 11 2020 at 9:12pm

I wanted to paste the last chart from this post but didn´t succeed. Powell is cheer leading for fiscal policy while letting monetary policy wither-away!

https://thefaintofheart.wordpress.com/2020/10/09/is-the-new-monetary-policy-framework-ait-an-improvement/

Garrett

Oct 12 2020 at 8:15am

Interestingly, 10-year zero coupon inflation swaps are currently trading at 2%. The S&P500 tracks these prices pretty well. It seems like traders in this market believe the Fed’s 2% average inflation target.

I’m not sure what drove the dip in the second half of September and subsequent recovery. Fed comments?

Scott Sumner

Oct 12 2020 at 12:12pm

Garrett, Are those inflation swaps based on the CPI or the PCE. If it’s the CPI, then they need to be at about 2.3%.

Garrett

Oct 12 2020 at 12:54pm

Right, they’re CPI. Momentary forgetfulness on my part.

Thomas Hutcheson

Oct 12 2020 at 3:28pm

How should one compare the swaps cited with TIPS expectations?

How do you arrive at the CPI target equivalent of PCE?

TIPs expectations of 5 year inflation below that of 10 year (both of which are less than 2% CPI) which seems inconsistent with needing inflation to be higher during a period of supply restraint.

Garrett

Oct 13 2020 at 8:48am

Thomas,

The swaps I cited are one tradable market instrument, whereas the TIPS spread would require going long the TIPS and short the nominal to implement a breakeven trade. Therefore I believe that the swap is a “more pure” signal of the market’s inflation expectations.

CPI runs 20 to 30 bps higher than PCE, so if the market is implicitly forecasting 2% CPI then that means PCE is expected to be 1.7-1.8%.

marcus nunes

Oct 12 2020 at 10:08pm

Time Warp

Powell (2020) The recovery will be stronger and move faster if monetary policy and fiscal policy continue to work side by side.

James Tobin (1962) The Council sought to liberate mon pol to focus it squarely on the same macroeconomic objectives that should guide fiscal policy.

Comments are closed.