With the recent resignation of Shinzo Abe, there have been a number of articles analyzing the record of Abenomics. There seems to be pretty general agreement on two points:

1. Japan’s economy improved after Abe took office at the beginning of 2013. Deflation came to an end, nominal GDP began rising, the public debt was brought under control, and unemployment fell to just over 2%.

2. The policy was not completely successful. Most notably, inflation continued to run well below the 2% target set by the Bank of Japan.

I believe that summary is correct. Where I part company with other pundits is in the lessons that Abenomics offers for monetary and fiscal policy. The Economist is fairly typical:

The first lesson is that central banks are not as powerful as hoped. Before Abenomics, many economists felt Japan’s persistent deflationary tendencies stemmed from a reversible mistake by the Bank of Japan (boj). It had combined fatalism with timidity, blaming deflation on forces outside its control, and easing monetary policy half-heartedly. In 1999 Ben Bernanke, later a Fed chairman, called on the boj to show the kind of “Rooseveltian resolve” that America’s 32nd president showed in fighting the Depression. . . .

The central bank is doing everything it can to revive private spending. Until it succeeds, though, the government has to fill whatever gap in demand remains. The shortfall in private spending is what makes government deficits necessary.

This seems to be the consensus as to the “lessons” of Abenomics. Monetary stimulus is not enough; you also need fiscal stimulus. And yet if you look at the actual record of Abenomics, there’s not a shred of evidence to support this claim, indeed the opposite seems to be the case.

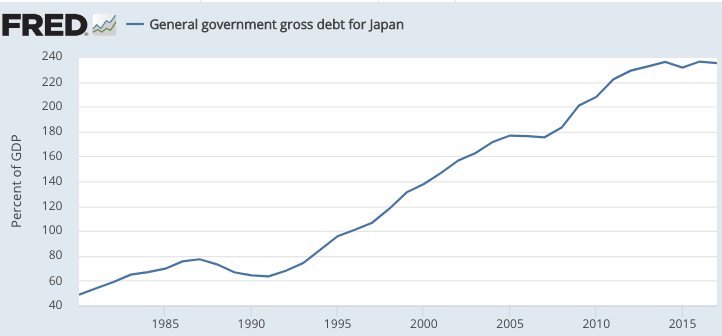

For nearly two decades before Abe took office, Japan ran perhaps the largest combined monetary/fiscal stimulus in human history, at least during peacetime. Remember, combined fiscal/monetary stimulus is the new consensus, the policy that most pundits in academia and the media now favor. And what was the result of this massive stimulus? Basically zero growth in nominal aggregate demand for almost two decades, a record even worse than seen in slow growing Italy. If you’d told economists in the early 1990s that over the following 20 years Japan would mostly hold interest rates close to zero and increase the national debt from less than 70% of GDP to roughly 230% of GDP, and still have virtually no growth in nominal GDP, they would have responded that we need to abandon the standard textbook model of economics, as what we are teaching our students is clearly wrong. Instead, we responded to this amazing analytical failure by doubling down on the very same flawed theory.

The massive fiscal stimulus came to an end with Prime Minister Abe. Taxes were raised several times and the national debt leveled off at just over 230% of GDP. Instead of a combined monetary fiscal stimulus, Abe relied on monetary stimulus and fiscal austerity. And the Japanese economy actually improved!

I must admit that I am perplexed as to how my fellow economists draw their “lessons” from this record. When people question monetary stimulus by pointing to the fact that Japan fell short of its 2% inflation target under Abe, I respond, “so do more”. This doesn’t seem to convince anyone. People seem to think I’m cheating, coming up with a theory that’s unfalsifiable. “Yeah, you can always say they didn’t do enough.”

But when it comes to fiscal policy, this skepticism goes right out the window. If I point out that the huge Japanese fiscal stimulus of 1992-2012 failed boost aggregate demand, they say the Japanese should have done even more fiscal stimulus, as if boosting the national debt from less than 70% to 230% of GDP is not enough. When I point out that the Bush tax cuts of 2008 failed, they say the tax cuts should have been even bigger. When I point out that the Obama stimulus of 2009 led to an unemployment rate that was far higher than proponents predicted even in the absence of stimulus, they say the stimulus should have been even bigger. When I point out that the economy actually sped up in 2013, despite widespread Keynesian predictions that it would slow due to austerity, they say that without austerity it would have improved even more. When I point out that the economy did not fall off the cliff at the end of July when Congress failed to renew the fiscal stimulus, they say it would have improved even more with additional stimulus (even though the fall in unemployment in August was the second largest in history.)

Now it’s certainly possible that I’m wrong and the Keynesians are right about fiscal stimulus. Counterfactuals are tricky. Maybe in all of these cases if they had only done more the results would have been better. But in that case I’m honestly confused as to why I’m not allowed to argue the BOJ should have done more monetary stimulus. Especially since while fiscal stimulus might become costly in the future if interest rates rise above zero, monetary stimulus is actually profitable, as central banks earn income on the assets they purchase with zero interest base money. It’s monetary policy that seems to have truly unlimited “ammunition”, not fiscal policy.

Nonetheless, I’ve been beating my head against the wall for so long on this issue that I feel I need to change the argument. Thus I’ve recently focused not so much on the claim that Japan needed to do more, rather that Japan needed to do different. The ultra-low rates and massive QE are actually a symptom of previous tight money mistakes.

For example, the yen was about 124 to the dollar in mid-2015. Today it’s roughly 105 to the dollar. If Japan had simply pegged the yen to the dollar at 124 back in 2015, Japanese interest rates actually would have been higher over the following 5 years, mirroring the rise in interest rates in the US during this period (due to interest parity). Monetary policy would have looked tighter to the Keynesian skeptic who (wrongly) feels that the actual Japanese monetary policy was highly expansionary, and ineffective. And yet because the yen would have been far weaker, Japan would have actually experienced higher inflation than otherwise. Indeed Lars Svensson made essentially this argument back in 2003, when he described a “foolproof” way for Japan to escape a liquidity trap. He also noted that the higher nominal interest rates would be nothing to worry about, as this policy would have reduced the real interest rate in Japan, due to higher inflation expectations.

There are political difficulties with pegging the yen to the dollar, but Japan could have achieved a similar result by setting an aggressive price level target combined with a “whatever it takes” approach to QE.

So today I say to Japan, “don’t do more, do different.”

And I say to my fellow economists, “use the same criterion for drawing lessons from monetary policy as you use for drawing lessons from fiscal policy.”

PS. Some economists do econometric tests of fiscal policy efficacy. Elsewhere, I’ve criticized those tests for ignoring monetary offset.

READER COMMENTS

Mark Barbieri

Sep 21 2020 at 1:47pm

Why can’t the BOJ start a policy of monetizing Japan’s huge debt? Surely there is a level of debt monetization that will cause low but positive inflation.

I’m baffled by the large number of people I know that simultaneously believe that MMT will lead to hyperinflation and also believe that the Fed cannot meet their 2% target because interest rates are too low already.

Scott Sumner

Sep 21 2020 at 4:28pm

Good questions.

dtoh

Sep 21 2020 at 11:21pm

Scott,

The lesson of Japan is simple.

“You can’t have economic growth with a confiscatory tax policy.”

Nobody is going to invest if the expected real after tax return is negative.

If you don’t have investment and the size or your work force is stagnant, you will have nil or negligible growth.

Most productivity growth from technology comes in the form of bigger faster machines (that require investment) not from miracle inventions.

Almost all of Japan’s growth over the last decade or so has resulted from an increase in the female LFPR (which is about to hit its limits.)

Abenomics failed because it did not implement the structural reforms upon which it was premised.

(There is a longer more subtle argument to be had with respect to the fx effects of Japanese monetary policy, and I agree with you that this could have been effective… but for different reasons and mechanisms than those you mention.)

Scott Sumner

Sep 22 2020 at 1:21pm

Yes, supply side reforms would have helped. I was looking at demand side policies.

dtoh

Sep 23 2020 at 5:26am

Scott,

You said “supply side reforms would’ve helped.” In fact supply side reforms are the only thing that would’ve helped. I believe you have stated before that once an economy reaches full employment (for any given set of supply side conditions) any further growth from monetary stimulus would be entirely nominal. By the way I don’t agree with that (I think the ratio of nominal to real growth increases at an accelerated rate, but that you still get some real growth even once you reach full employment.) But in either case, for Japan’s current supply side conditions there is very little real growth to be squeezed out of the economy with monetary policy. The only thing monetary policy could have achieved was higher inflation with very little real growth.

In addition, and I’ve mentioned this before, if wages and prices were not sticky, then monetary policy would both be totally ineffective and totally unnecessary. In the case of Japan, 20 years of stagnant wages and a very competitive pricing environment, have wrung most of the stickiness out of wages and prices, which I guess is another way of saying that the Japanese economy is at full employment because the labor market has been able to adjust simply through the normal pricing mechanism.

Postkey

Sep 23 2020 at 3:31am

“The lesson of Japan is simple.”?

‘Princes of the Yen: Central Bank Truth Documentary’

https://www.youtube.com/watch?v=p5Ac7ap_MAY

Postkey

Sep 22 2020 at 4:01am

From a ‘Thatcherite’ monetarist.

“Japan – like the USA – may prove another fascinating test of different theories. Over the last 30 years it has had both the lowest rate of broad money growth in the world and the lowest rate of increase in nominal GDP. (For years the Bank of Japan has declared a 2% inflation target, and inflation has remained stubbornly beneath it. If 5% plus money growth [at an annual rate] now emerges, inflation of above 2% would be expected by a quantity-theory economist.) On 16th March the Bank of Japan announced that it would buy “aggressively” exchange-traded funds at an annual pace of around ¥12 trillion (about $110b.), double the amount previously planned. The budget deficit has also widened dramatically and – as elsewhere – will be financed to some extent from banks. An upturn in money growth has occurred, with the three-month annualised rate of increase to May reaching 15.7%, which is an extraordinary figure by Japanese standards. If Japan in the next few quarters hits and exceeds its 2% inflation target, this might persuade sceptics that inflation is indeed a monetary phenomenon and not a by-product of “national psychology” or some such nonsense. It might also persuade the far too numerous monetary economists who focus on the base and narrow money that an all-inclusive, broadly-defined aggregate is the one to watch. “

https://mv-pt.org/wp-content/uploads/2020/07/Monthly-e-mail-2007-Global-money-round-up.pdf

Brian Donohue

Sep 22 2020 at 11:38am

Excellent post!

Lizard Man

Sep 22 2020 at 10:12pm

Are there political constraints on central banks that prevent them from, in effect, simply printing money and giving that money to people?

So long as an institution has the ability to print and distribute money, I fail to see how it could ever be powerless to raise inflation. If inflation is too low, then all they need to do is print more money. The reductio ad absurdum of infinite money printing and no rise in inflation is obvious. So why wouldn’t the analysis be something along the lines of the central bank having limited ability to increase the money supply? That would make more sense from an analytical standpoint.

Scott Sumner

Sep 23 2020 at 12:36pm

I don’t believe the Fed can just give money away, nor should it be allowed to. That’s fiscal policy, and those decisions (i.e. who gets the money) should be made by government officials.

There’s no doubt that that would raise inflation, but then there’s also no doubt they can raise inflation by purchasing enough assets.

Lizard Man

Sep 24 2020 at 7:53pm

What if they run out of assets?

Comments are closed.