“Modern Monetary Theory” or MMT comes in two broad versions, the economic version and the political-gospel version. It is not easy to distinguish them.

The economic version claims that a national state can finance its interventions, or some of them, by using unemployed resources or, at full employment, by diverting (that is, grabbing) employed resources through deficits financed by money creation. If inflation ensues, the theory continues, it can be countered by more visible ways of grabbing resources such as higher taxes, wage and price controls, capital controls, rationing, and such. The few economists who defend MMT invoke bits and pieces of economic theories that are not exactly “new,” those of John Maynard Keynes or Abba Lerner, for example, but their theory remains very marginal.

They often have strange ideas, such as “Anything that is technically feasible is financially affordable,” as Professor Stephanie Kelton has written. George Selgin corrects her:

That something is technologically feasible means, not that it’s “affordable,” but only that it might be done at some finite cost. Perhaps Professor Kelton does not recognize, or does not want her readers to recognize, the difference. But a difference exists nonetheless, and it’s a lu‐lu. For all I know, we might populate the moon, equip every U.S. citizen with a Ferrari, or fill Lake Meade with champagne, technically speaking. But I’m quite certain we can’t afford to.

The idea that the state could dramatically increase its reach and substitute public choices to individual choices on a grand scale without facing serious budget constraints has understandably enflamed those who believe it should control a larger part of economic life (and therefore a larger chunk of personal lives, for the people’s own good). In fact, MMT seems mostly defended by activists and academics who see it as a promise to make possible the sort of society they want.

Hence the political-gospel version of MMT. MMT claims that we can get all the “nice things” that “we” want at no cost to anybody among us. The sovereign state only needs to create dollars (or other national currencies under foreign sovereign states) to pay for them. A movement called Our Money, created by Baptist pastor Delman Coates, wants exactly that. The gospel aspect of MMT has been identified as such, and not disowned, by The New Republic (Osita Nwanevu, “Spreading the Gospel of Modern Monetary Theory,” October 3, 2019). Says the pastor:

We need more leaders, more infuencers becoming evangelists for this incredible good news … that our economy does not have to be predicated on scarcity.

The fact that many economists on the left, notably Larry Summers and Paul Krugman, have warned against the fallacies of MMT does not stop the movement’s preachers from clamoring for free money to finance the Green New Deal, a federal job guarantee, and God knows what. (Incidentally, slaves did have a job guarantee.) Snake oil is not only for sale on the right.

One representative of the MMT gospel is D.T. Cochrane, an economics lecturer at York University in Toronto. In an article that was reproduced on a site for Canadian accountants, “How Government Deficits Fund Private Savings,” Mr. Cochrane explains that the worries about budget deficits “are largely based in misrepresentation or ignorance of government debt and money.” Many good critiques of MMT exist (besides George Selgin, you may want to read Scott Sumner and Patrick Horan and Warren Coats) and I will concentrate here on only one argument Mr. Cochrane echoes. The objection that creating money to finance government expenditures will lead to hyperinflation like in many countries such as Venezuela, he claims, is invalid. Inflation, he argues, came from the fact that “production had collapsed”; the relation between inflation and the increase of the money supply is not necessarily true.

In a Cato Journal article, Sebastian Edwards reviews the case of Venezuela, which Cochrane invoked. Inflation was already a problem when Hugo Chávez was elected in 1998–partly, as many other populist leaders, with a mandate to stop inflation. In fact, he continued to increase the monetary base at high annual rates (10%-30% until 2003, and still higher until data became unavailable in 2013). Probably because of high oil prices, the regime was able to cap inflation at these high rates, until it reached 43.5% in 2013. GDP collapse in 2014, when annual inflation was 57.3%. Hyperinflation ensued with 1,000% in 2017, 130,000% in 2018, and even more since then (in prices denominated in the national “sovereign” currency), but it is clearly incorrect to say that inflation reared its ugly head only after GDP had collapsed.

Edwards also review in detail the cases of Chile in 1971-1973 and Peru in 1985-1990. In these cases too, money creation and high inflation preceded GDP collapse. The collapse of production was in large part a result of high inflation and the consequent distortions in the economy. Of course, when high inflation becomes hyperinflation, production collapses even more. Speaking of episodes of runaway inflation in Latin America, Edwards writes:

In most of these episodes—Argentina, Bolivia, Brazil, Chile, Ecuador, Nicaragua, Peru, and Venezuela—policymakers used arguments similar to those made by MMTers to justify extensive use of money creation to finance very large increases in public expenditures.

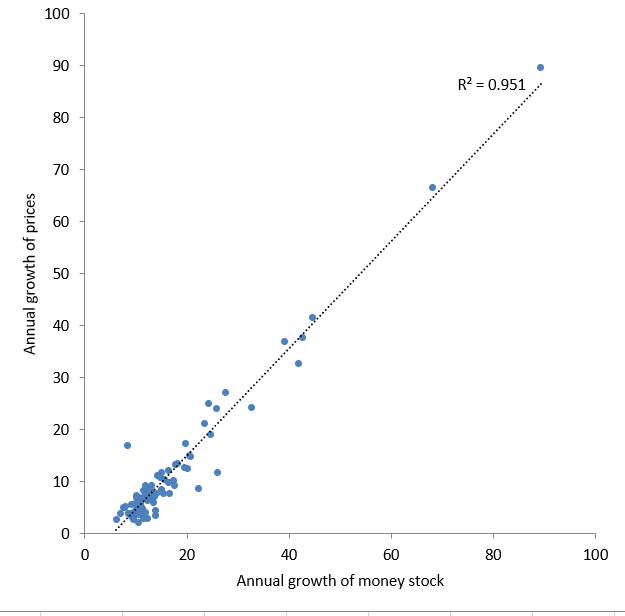

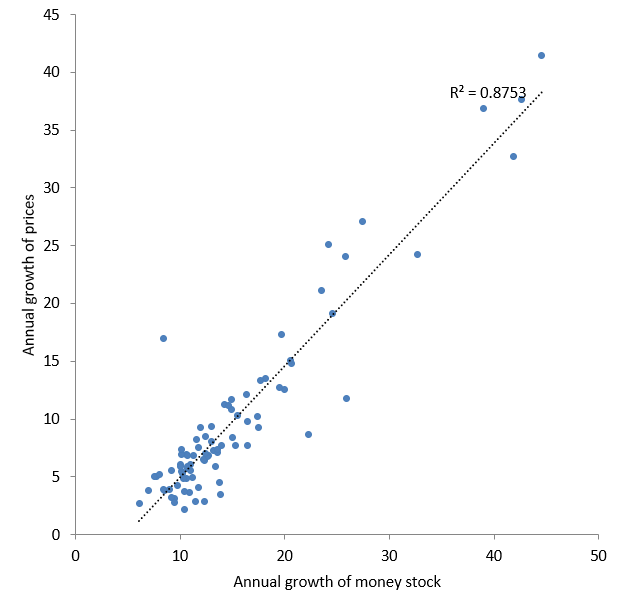

A wider empirical study published in 2004 by Professor John Frain of Trinity College Dublin confirms the prediction of standard economic theory: increasing the money stock necessarily, at some point (when the increase does not follow an increased demand for money by individuals), leads to inflation (John C. Frain, “Inflation and Money Growth: Evidence from a Multi- Country Data-Set,” Economic and Social Review 35:3, [2004], 251–266). Frain built a series for 87 countries’ average money growth rates and average rates of inflation between 1948 and the early 2000s. Drawn from his data, the two charts below show the close correlation between the two variables. (The second chart excludes the two outliers of the first one, Nicaragua and Argentina, in order to reduce the scale of the graphic and show more clearly that the correlation continues to hold for the other countries.) The correlation coefficients are high and the parameters of the two regression lines are highly statistically significant.

Growth of Money Stock and Price Inflation in 87 Countries, Second Half of the 20th Century (Source: John C. Frain, “Inflation and Money Growth: Evidence from a Multi- Country Data-Set,” Economic and Social Review 35:3, [2004], 251–266)

Growth of Money Stock and Price Inflation in 85 Countries, Second Half of the 20th Century (Source: John C. Frain)

On the contrary, Edwards notes, MMT supporters “have offered very little empirical evidence on how the policy would function.”

To summarize: From what we know, financing government expenditures by creating money is highly inflationary and leads to serious or catastrophic economic problems and, indeed, to the collapse of production. With MMT, this time would not be different.

READER COMMENTS

P Burgos

Feb 3 2020 at 9:54am

Isn’t it true by definition that using unemployed or underemployed resources leads to economic growth without much inflation? Isn’t that what happens with catch up growth in developing countries and immigration into developed countries? If the labor pool for factories and construction are people living in rural areas the world over, that is nearly half the world’s population. So if you what you want to do is build physical things, it seems the constraint would only be whatever white collar labor is required.

Jon Murphy

Feb 3 2020 at 10:48am

For certain definitions of “unemployed/underemployed,” yes that is true. But, as the economy approaches full employment, the inflationary pressures mount. The MMT crowd contends that even at full employment the increase on money supply can be “sanitized” and not lead to high inflation rates if 1) the country controls its own monetary base and 2) the taxation rate is constantly adjusted to remove “idle” savings from the economy and put it back into the Treasury.

Thomas Hutcheson

Feb 3 2020 at 11:35am

It’s not clear just what the MMT “crowd” contends. 🙂

Deficits at full employment can be “sanitized” and not lead to excessive inflation. That is exactly what the Fed is doing right now (slightly too much, in my view, as they have not yet achieved average inflation at their supposed target rate). “Sanitization” does not make the pattern of taxing and spending decisions that produced the deficits wise.

Thaomas

Feb 3 2020 at 11:22am

No. This is a slightly different view. The “developmental” strategy you mention is ultimately build on the idea that the investment needed to bring “rural” laborers and train them to work in “modern” activities has a very high rate of return. “Keynesian” unemployment rests on the idea that there are unemployed or partially unemployed resources that can be employed with higher aggregate demand.

[I suppose that with sufficient effort on could bring both ideas into the same formal statement, but I do not think it would be helpful.]

Thaomas

Feb 3 2020 at 11:13am

This is, of course, perfectly true. A state can “finance” it’s interventions with taxes. This seems like a perfectly mainstream view. The issue is for any given intervention is if it wise to do so.

I’m afraid that MMT is not yet well enough defined even to be wrong.

Mark Z

Feb 3 2020 at 8:09pm

Yeah, I was gonna say, “if inflation ensues” and we have to resort to taxation, then MMT has failed. The whole point of MMT is that there is no tradoff, we don’t need to give up other kinds of consumption (through taxation) to enjoy more state-provided goods/services.

Pierre Lemieux

Feb 5 2020 at 1:58pm

@Mark: In a sense, you are right: it would show that MMT has failed. However, it cannot fail because its promoters do include a host of coercitive measures waiting in the background, such as wage and price controls, rationing, and forced savings (all are mentioned by Yeva Nersisyan and L. Randall Wray, “How to Pay for the Green New Deal,” May 2019).

Pierre Lemieux

Feb 5 2020 at 2:02pm

@Thaomas: In a sense, MMT, as I understand it, is indeed just a mainstream theory of government intervention, with monetary addendums, such as the power of monetary policy to influence real variables and the use of fiscal policy (like taxes) to control inflation.

Phil H

Feb 3 2020 at 1:00pm

The problem as I see it is that this is just the old politics with new fancy terminology, isn’t it?

Lemieux says: “increasing the money stock necessarily, at some point (when the increase does not follow an increased demand for money by individuals) leads to inflation”

wecanhavenicethings.com says: “We can provide a well-paying job for anyone who wants one. Medicare-for-All. Child care… excellent public schools…Yes, there are limits… Our spending limit is inflation”

There’s no difference, except for this one: L doesn’t believe that people want those things. Because if individuals did want those “nice things”, even if the government provided them, that would not cause inflation (according to L).

I suppose it’s obvious in some ways that economic theory will correlate with political stance. But inevitably, it also makes the economic reasoning look motivated.

Christophe Biocca

Feb 3 2020 at 1:38pm

I don’t follow, where does he say that?

Phil H

Feb 4 2020 at 2:35am

I don’t think he says it explicitly. I infer it from these premises: (1) L says that IFF individuals demanded that money, printing it would not cause inflation; (2) L says that if the government uses money for big projects like the green new deal, inflation would follow. I think that means he believes there is insufficient demand on the individual level for the green new deal, and the other big government projects mentioned.

Christophe Biocca

Feb 4 2020 at 9:29am

“demand for money” means demand for money per-se (as in cash/cash-like entities). If people suddenly want lots of cash to bury in their back yard/stuff in their mattress (to pick an extreme example), the government can satisfy that demand without affecting inflation at all (because the money will not actually be used in bidding for anything at all). Note that there’s a converse to this: if people’s demand for money decreases (all those same people decide to dig up the money from earlier and spend it), the government might need to take some of it out of circulation (decrease the money supply) to stop inflation from happening.

It is not a stand-in for “things money can buy” (otherwise demand for money is always unboundedly high, which would predict that inflation is impossible).

Phil H

Feb 4 2020 at 10:45pm

Huh, I think you’re right! It means demand to hold money… Which does mean I was wrong about the equivalence of those two statements. Thank you!

Pierre Lemieux

Feb 5 2020 at 1:50pm

Yes, thanks to you, and to @Phil for graciously accepting this important precision.

Mark Z

Feb 3 2020 at 8:03pm

No, the difference is MMT supporters think that there is no opportunity cost to having the government buy all these things for everyone. Doing so would not divert labor and resources from production of other things, because there’s a massive underutilization of resources in the ‘natural’ state of affairs which would instead be mobilized, and thus the price of everything else would remain the same (no inflation). What opponents of MMT are saying is that, no, large scale spending increases funded by money-creation would in fact divert resources from elsewhere, driving up the prices of other things (inflation).

There is agreement that inflation is the limitation, but disagreement over whether (or at what point) inflation would result from such printing press-financed projects, or where the limit is. Who wants what is irrelevant. The question is, when the government prints money to buy things to give people, will the new free stuff be an absolute increase in production, or will it come from a diversion of resources from the production of other stuff? And whether there’s inflation is an indicator of that. Or, put in a less binary way, at what point (how much free stuff can the government buy us) will it start diverting resources from production of other things.

Phil H

Feb 4 2020 at 2:31am

Lemieux says: “when the increase does not follow an increased demand for money by individuals”

Mark Z says: “Who wants what is irrelevant.”

You’re clearly arguing something different from Lemieux. I understand your opportunity cost point, but that’s not the point he’s making, given that he thinks individual demand (which also imposes opportunity cost) *is* a decisive factor.

Mark Z

Feb 4 2020 at 10:30pm

I don’t think we are arguing different things. A real increase in production (and consumption) tends to go hand in hand with an increase in demand for money. There’s more stuff to buy, so for prices to stay the same, there needs to be more money. So I think whether or not there’s an increase in the demand for money to meet the increase in supply reflects whether there’s an increase in total production or just more money chasing the same amount of goods.

Thaomas

Feb 4 2020 at 12:51pm

But if there were lots of unemployed resources and the government created demand for their employment (invested in lot of projects having very high net present values because the opportunity cost plugged into the equation would be near zero) and no no more inflation resulted than the Fed was targeting, what’s “modern” about that? Or if there was a mistake in estimating the opportunity cost of the project inputs and the fed had to tighten monetary policy, What’s “modern?”

I just do not see what’s new. Possibly it’s a new way of estimating the amount of underemployed resources, but then it’s funny to call that a “monetary” theory.

I’m sticking with,”not even wrong.”

Thaomas

Feb 5 2020 at 8:34am

IFF that is what MMTists think (Pierre’s restatement may give it more coherence than it is due) a) it’s not a “monetary” theory but a theory about resource markets not clearing and b) if that theory about markets not clearing were the case, non-MMT would also predict no inflation.

‘Tis a great enigma.

zeke5123

Feb 3 2020 at 2:41pm

I am not sure Selgin is precisely correct. The questions that needs to be answered isn’t whether we can equip U.S. citizen with a Ferrari, fill Lake Meade with champagne, and populate the moon separately but together.

That is technically infeasible (i.e., each one on its own may be achievable, but together it is not). Stated differently, Keaton’s claim seems to be one that opportunity cost does not exist where technology permits (think Star Trek replicators — the idea of opportunity cost becomes silly). Selgin’s response implicitly assumes technically infeasibility by stating “we can’t afford.” The reason we can’t afford to is that it is not technically feasible to give everyone a Ferrari, fill Lake Meade with champagne, and populate the moon (i.e., the people and resources needed to do all three things would conflict). Because of this scarcity, there must be a trade-off between the three.

So in that sense Keaton is correct — if it was technically feasible to have X, Y, and Z, then we could afford them. But where she is wrong is that she seems to change the formulation to if we can do X, Y, or Z, then cost doesn’t matter. The moment it is an or, then cost necessarily matters because scarcity matters.

Christophe Biocca

Feb 3 2020 at 3:07pm

I think Selgin picked these examples precisely because they can’t be afforded at that scale (as in it would cost more than the entire US GDP to do such things).

Setting up a moon base for 10 people to stay for a few weeks is both feasible and affordable for NASA (at just a few 10’s of billions). Populating the moon with 1,000,000 permanent residents is technically feasible (just repeat the process over and over) but utterly unaffordable (at least barring massively cheaper launch vehicles).

Filling a swimming pool with champagne is technically feasible and could be afforded by an individual with more money than sense, but filling Lake Meade is technically feasible (just make more champagne) but requires increasing total champagne production by 3-4 orders of magnitude. We’d convert all of our farmland, and basically starve to death before we got there.

Not 100% sure the Ferrari example is true (depends on the variable-cost component), but if we assume that each car has a labor cost of manufacturing of ~$80,000 then we can’t afford giving every American one without putting more than the entire population of the country to work on making them.

Pierre Lemieux

Feb 4 2020 at 10:36am

Zeke5123: Two issues have to be carefully distinguished: whether something is technologically feasible or not; and whether something that is technologically feasible is affordable (economical) or not. (Building a factory for the mass production of six-finger gloves is technically feasible; but nobody would want to pay for it.)

zeke5123

Feb 4 2020 at 1:48pm

I am certain we agree, but framing is different. My point is that “affordable” assumes the technically feasible. Imagine a world with Star Trek replicators. Discussing affordable in that context doesn’t make sense.

Affordable only makes sense in the world of trade-offs (which alas is the world we live in).

Keaton obfuscate the trade-off by focusing on whether the particular item is technically feasible to achieve, and then claims it is affordable because it is feasible. But to prove her last point, Keaton would need to say that the item is technically feasible to achieve without changing the production / consumption of all other goods. Indeed, if it was technically feasible to do so, then of course it would be feasible. But there are trade-offs and thus Keaton claim fails.

Does that clarify what I was trying (but failing) to communicate?

Pierre Lemieux

Feb 9 2020 at 11:53pm

I think so. Feasibility is a necessary but not sufficient condition for affordability, right? Or are you saying more than that?

Ed Zimmer

Feb 4 2020 at 5:32pm

The idea that “money” is some tangible thing should have died 50 years ago.

GDP is the measure of our productive economy. GDP is the sum of household, business and government spending (and likewise the income of those sectors equals that spending because all spending is another’s income). Our economy depends on household spending (2/3 of GDP). That spending is limited by household income (which comes only from those three sectors). Business provides that income to the extent demand (business opportunity) exists, and government provides the rest (by way of bookkeeping entries to household bank accounts). All that’s important to the economy is maintaining this flow, and with a fiat currency (whose value, by definition, depends ONLY on currency-users perception), there are no limits other than that perception.

Christophe Biocca

Feb 4 2020 at 9:57pm

Which is how Venezuela, which saw its nominal GDP (denominated in their own currency) increase ~1000-fold in ~5 years, became a utopia.

Ed Zimmer

Feb 5 2020 at 11:42am

A meaningless strawdog. Incapable of logic?

Christophe Biocca

Feb 5 2020 at 12:12pm

When your statement is that increasing nominal GDP is the only thing that matters, expect people to point to counterexamples. Feel free to fix your statement by using real GDP, or more generally stop confusing the measurement with the thing being measured.

Jon Murphy

Feb 5 2020 at 9:26am

A quick technical point:

GDP is a measure of economic well-being, not the measure of a productive economy. A lot of productive activities are not included in GDP such as the exchange of used goods, the purchase and use of imports, parenting, volunteer work, etc. Likewise, a lot of unproductive activities are included in GDP, like much government spending (indeed, Simon Kuznets, who originally derived the measurement, wanted to exclude government spending).

Ed Zimmer

Feb 5 2020 at 11:45am

You’re using your own definition of “productive” – BEA has a very well-defined definition, which they try very hard to <b>measure</b>. Much government spending is not included in GDP until its recipients spend it on actual goods and services (in the interim it’s accounted as transfer payments). Our economy consists of a <b>productive</b> economy (as measured by NGDP) and a <b>non-productive</b> (largely consisting of the financial industry (aka, the big casino).

Jon Murphy

Feb 5 2020 at 12:33pm

No, I am using the standard one the BEA is trying to measure (see, for example The Economic Way of Thinking by Hayne, Boettke, and Prychitko, pg 282). Do not confuse the definition of the measurement with the definition of the concept.

This misconception leads to your incorrect distinction between the “productive” and “non-productive” economy. It would imply that, say, me making a sandwich at home is a non-productive activity, despite the fact it is clearly productive.

Correct. Transfer payments are not included in GDP so as to avoid double-counting (same with imports). But other forms of government spending are included in.

Pierre Lemieux

Feb 5 2020 at 1:45pm

I agree with this, @Jon, but I think both your and @Ed Zimmer’s definition or characterization of GDP is not correct (at least as expressed). As the BEA writes, “GDP is defined as the market value of the goods, services, and structures produced by the economy in a given period” (see Concepts and Methods of the U.S. National Income and Products Accounts, November 2019, p. 2-7). GDP is production–and emphatically not a measure of welfare, although it can be an indicator. GDP is only measured, not defined, by the sum of final expenditures or by the sum of income payments, which is @Ed’s first mistake (see ibid., p. 2-9, where you’ll find a very useful chart). By the way, there is a third way to measure GDP, closer to its definition, which is gross value added.

Jon Murphy

Feb 5 2020 at 2:07pm

I agree with that. My original point was poorly stated.

Pierre Lemieux

Feb 5 2020 at 1:48pm

@Ed: GDP is production and can be measured by expenditures or incomes. See my answer to @Jon, where you will also find a reference to a BEA handbook. This error leads you to confuse GDP and money.

Ed Zimmer

Feb 5 2020 at 4:52pm

Pierre,I’ll claim that NGDP both defines AND measures the productive economy as BEA clearly defines every measured line item (as well as GDP). Their method of measurement IS expeditious (compared with the sum-of-value approach), but rational given the quality of data they’re given to wwork with. If you want to argue that what cannot be definedd AND measured can be believed, I’d like to have that argument. Blair Fix has a good article on that today at https://economicsfromthetopdown.wordpress.com/2020/02/05/how-do-you-spot-a-crank . And for a good MMT vs. mainstream comparison, I think Bill Mitchell did an especially good job at that today at http://bilbo.economicoutlook.net/blog/?p=44219 , The Old Guard Trying To Stay Relevant And Failing.

Glenn Corey

Feb 5 2020 at 7:14pm

So Ed, It seems like MMT is making empirical claims. What would have to happen for it to be discredited? Or is it a faith-based initiative that can’t be refuted? Eventually, it seems like it’s going to be tried because those politicians who favor it are gaining traction, so can you say what would convince you that the critics of MMT are right?

Pierre Lemieux

Feb 10 2020 at 12:24am

Ed: A couple of quick points.

The BEA does establish the important distinction between nominal and real GDP.

Certainly, some things that can be defined cannot be measured, except very imperfectly and indirectly. Utility (take it in the modern ordinal, Hicks-Samuelson sense) can be defined but only indirectly measured–by revealed preferences–and only in certain cases. Moreover, utility, as defined subjectively, cannot be compared among individuals. You must agree with this at least in certain cases, for you seem to distinguish best and “expeditious” measures.

I agree with “Top Down” that there is no algorithm for identifying a crank, but I don’t agree with all his criteria. About criteria #4, for example, perhaps he should read Hayek’s The Counter-Revolution of Science.

I wonder how Bill Mitchell imagines that “collective control over politics and society” works. With a social-welfare function? What about Arrow’s Impossibility Theorem? I have some reflections on this in my Econlib article on “The Vacuity of the Political ‘We’.”

Rebes

Feb 5 2020 at 6:18pm

Question for MMT. If the amount of debt incurred to finance deficits is not an issue because the government can print money, why borrow at all? Why not print money now to cover the deficit?

dede

Feb 6 2020 at 11:39pm

“why borrow at all?”

To hand out taxpayers’ money to the rich capitalists who can afford to buy government bonds. It does not make sense at zirp though so I may have to take off my marxist glasses and agree that MMT is yet another BS marxist solution…

Comments are closed.