I frequently argue that the fiscal multiplier is roughly zero in an economy where the central bank targets some variable linked to aggregate demand, such as inflation or NGDP. I don’t claim it is precisely zero, just that zero is a good baseline assumption to start the analysis.

This claim is often viewed as being quite heterodox. In fact, at the upper levels of economics it is a quite mainstream view of how things work when the economy is not at the zero bound (like right now.)

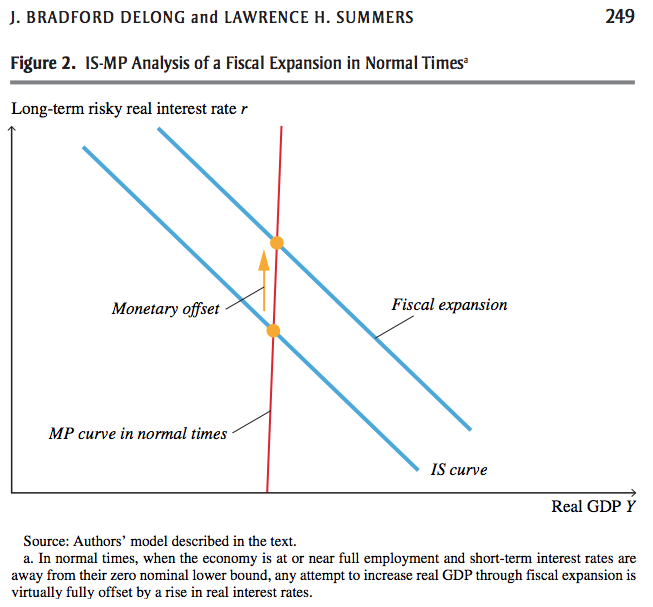

Here are DeLong and Summers (2012):

From the time of Keynes’ General Theory to the 1960s, the default assumption was that interest rates would remain constant as fiscal policy changed, because the central bank and the fiscal authority would cooperate to support aggregate demand: fiscal expansion would be accompanied by monetary policy accommodation that produced not crowding out but crowding in. With the changes in macroeconomic thinking and the inflationary experience of the 1970s, the natural assumption in the United States came to be that the Federal Reserve was managing aggregate demand. Thus, changes in fiscal policy, just like changes in private investment demand, would be offset as the Federal Reserve pursued the appropriate balance between inflation and investment. Today, however, at least until the economy exits from the zero lower bound or cyclical unemployment drops substantially, the economy is once again in a regime in which real interest rate movements amplify rather than offset the effects of fiscal stimulus.

Their paper has a nice graph that illustrates the case when interest rates are positive:

In 1997, Paul Krugman wrote an article criticizing “vulgar Keynesianism”, which is the version of Keynesianism that tries to apply ideas such as the “paradox of thrift” to modern economies with positive interest rates and inflation targeting central banks:

Consider, for example, the “paradox of thrift.” Suppose that for some reason the savings rate–the fraction of income not spent–goes up. According to the early Keynesian models, this will actually lead to a decline in total savings and investment. . . .

Or consider the “widow’s cruse” theory of wages and employment (named after an old folk tale). You might think that raising wages would reduce the demand for labor; but some early Keynesians argued that redistributing income from profits to wages would raise consumption demand, because workers save less than capitalists (actually they don’t, but that’s another story), and therefore increase output and employment.

Such paradoxes are still fun to contemplate; they still appear in some freshman textbooks. Nonetheless, few economists take them seriously these days. There are a number of reasons, but the most important can be stated in two words: Alan Greenspan.

But putting Greenspan (or his successor) into the picture restores much of the classical vision of the macroeconomy. Instead of an invisible hand pushing the economy toward full employment in some unspecified long run, we have the visible hand of the Fed pushing us toward its estimate of the noninflationary unemployment rate over the course of two or three years. To accomplish this, the board must raise or lower interest rates to bring savings and investment at that target unemployment rate in line with each other. And so all the paradoxes of thrift, widow’s cruses, and so on become irrelevant. In particular, an increase in the savings rate will translate into higher investment after all, because the Fed will make sure that it does.

To me, at least, the idea that changes in demand will normally be offset by Fed policy–so that they will, on average, have no effect on employment–seems both simple and entirely reasonable. Yet it is clear that very few people outside the world of academic economics think about things that way.

The one area I disagree with modern Keynesians is the effect of fiscal policy at zero interest rates. They argue that the fiscal multiplier becomes strongly positive, whereas I am skeptical—due to examples such as the fiscal austerity of 2013, which was successfully offset by the Fed.

But even there the differences are more a question of nuance. I concede that monetary offset does not always occur. Under the gold standard, central banks may have difficulty in offsetting fiscal shocks. (On the other hand, even Keynes acknowledged that the gold standard also makes fiscal stimulus much harder to do, due to the risk of a loss of confidence.) And there may be dysfunctional fiat money central banks (the BOJ or the ECB?) that do not fully offset fiscal shocks due to incompetence. Still a fiscal multiplier of roughly zero is the baseline assumption I use when considering shocks such as the recent Japanese tax increase. I doubt it will significantly impact employment, although it might briefly impact GDP.

So why do so many people believe in the fiscal multiplier, even when rates are positive? Perhaps it reflects memories of EC101 classes, where professors cover the fiscal multiplier but rarely get to the subject of monetary offset. Paul Krugman is clearly frustrated that so many people believe in the vulgar Keynesian model:

What has made it into the public consciousness–including, alas, that of many policy intellectuals who imagine themselves well informed–is a sort of caricature Keynesianism, the hallmark of which is an uncritical acceptance of the idea that reduced consumer spending is always a bad thing.

READER COMMENTS

Thaomas

Oct 25 2019 at 12:34pm

The degree to which a “fiscal multiplier” is greater than zero depends on the degree with which the additional spending which would be generated by governments continuing to apply (or starting to apply) an NPV rule falls on otherwise unemployed resources (assuming that the Fed in fact accommodates “additional spending” and does not offset it.

Don Geddis

Oct 25 2019 at 5:41pm

You seem to be hypothesizing a very strange Fed. It can see “unemployed resources” about, but stubbornly refuses to engage in additional monetary stimulus. But then when fiscal stimulus happens, it decides to “accommodate additional spending and does not offset it” — despite the fact that it was unwilling to choose that level of increased aggregate demand itself.

Yes, an incompetent central bank is surely possible. But an incompetent central bank could do anything. For example, it could choose to make the fiscal multiplier negative, “punishing” the fiscal government by engaging in more monetary offset than whatever fiscal stimulus is managed.

You need a more compelling argument, than merely that it is technically possible. The question instead is, why would such a bizarre situation be at all plausible?

Thaomas

Oct 26 2019 at 9:11am

I’m not “hypothesizing” anything. I am describing our very own Fed 2009-to … 🙂 My interpretation for this strange behavior is that the Fed knew that more stimulus was needed, knew that it was below it’s unemployment and inflation targets, but felt constrained by how much QE it could do (and later how long it could resist “normalizing” interest rates). The additional deficit that was occasioned by the “fiscal stimulus” was consequently not offset.

Kevin Erdmann

Oct 25 2019 at 1:23pm

I second Thaomas, and maybe would take it a step further. Even if fiscal spending uses completely unemployed resources, the range of the potential effect of that spending on real GDP is huge.

Considering the cost disease that has struck American cities – where a subway extension that should cost $1 billion costs $4 billion – the details of what the spending accomplishes seem more important than ever. Too important to be indicated with a line that moves mechanically to the right as spending increases.

The office building full of planning department bureaucrats, environmental reviewers, permit issuers, etc., that ends up making the subway cost $4 billion was funded by fiscal expansion. What was the effect of that spending on real GDP?

What is the effect of Trump’s border wall on real GDP? The Iraq War? Mass incarceration?

It seems like before this debate even gets off the floor, the premise deserves a lot of doubt.

Matthias Görgens

Oct 26 2019 at 7:54am

I don’t think Scott made any pronouncements on real GDP here. So that’s a completely separate topic.

I think some of his other writings imply that most private spending is superior to most public spending when it comes to real GDP. But that’s a pretty orthodox position for an economist.

The post here was purely about nominal GDP and the nominal fiscal multiplier.

Thaomas

Oct 26 2019 at 7:33pm

But nominal ~equals real in the dis-inflationary environment of a recession.

P Burgos

Oct 25 2019 at 1:31pm

I think this is either implied or just stated in the article, but the summary about views before and the 1970’s makes me think that whether or not you see a fiscal multiplier depends upon whether the central bank had an overall goal of disinflation or reinflation of an economy. Coming out of the Great Depression, it seems that the Fed had a disposition towards reinflating the economy. After the oil shocks of the 1970’s, the Fed wanted to disinflate the economy. Now the Fed seems to be creeping towards a reinflationary disposition, though hopefully in a more intelligent way than before.

Mike Sandifer

Oct 26 2019 at 1:04am

Earlier this year, I calculated the correlation between inflation and the Fed Funds rate to be about .75. so, obviously, this is consistent with Scott being roughly correct.

Kevin Erdmann

Oct 26 2019 at 1:55pm

Matthias Görgens, sorry, I don’t know how to reply to a comment in this interface, so I have to put my comment here.

The x-axis in the graph in the post is labelled “real GDP”.

Actually, now that I look at it, I would also take issue with the y-axis. Long term risky real interest rates is a whole can of worms.

On the other hand, the inability to figure out how to reply to a comment may be a decent poll test that isn’t a signal in my favor.

Scott Sumner

Oct 26 2019 at 5:16pm

Kevin, Good point. Their graph should have had nominal GDP on the vertical axis.

Comments are closed.