Noah Smith recently discussed a study that suggests a new approach to business cycles:

Gennaioli and Shleifer explain these patterns by turning to their own preferred theory of human irrationality — the theory of extrapolative expectations. Basically, this theory holds that when asset prices rise — home values, stocks and so on — without a break, investors start to believe that this trend represents a new normal. They pile into the asset, pumping up the price even more, and seeming to confirm the idea that the trend will never end. But when the extrapolators’ money runs out, reality sets in and a crash ensues. Gennaioli, Shleifer, and their coauthors have been only one of several teams of researchers to investigate this idea and its implications in recent years.

When extrapolative expectations are combined with an inherently fragile financial system, a predictable cycle of booms and busts is the result. At some point during good economic times, irrational exuberance takes hold, pushing stock prices, house values, or both into the stratosphere. When they inevitably come down, banks collapse, taking the rest of the economy with them.

Except for the “predictable” part, this is pretty much the standard view of the Great Recession. Obviously I think it’s completely wrong, but today I’ll focus more on how it became the standard view.

In the past, I often point to the 27-month period from January 2006 to April 2008, when the housing market crashed and the banking system came under severe stress. The unemployment rate was pretty stable during this period, rising from 4.7% to 5.0%. So obviously a housing crash and banking stress don’t directly cause a Great Recession, at least not immediately.

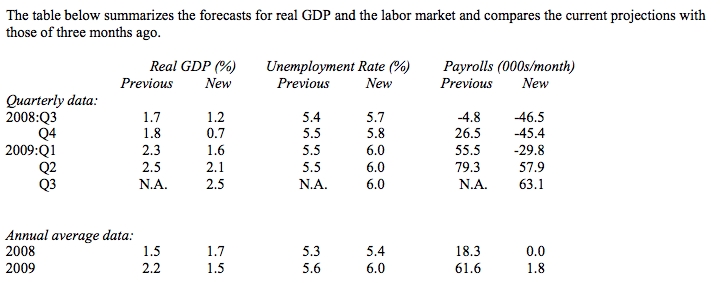

One counterargument is that these problems made a Great Recession inevitable, but with a lag. That may be true, but it’s important to emphasize that the economics profession as a whole did not accept this theory in mid-2008. Not even close. For instance, here’s the consensus forecast of professional economists in the 3rd quarter of 2008, when the Great Recession was already well underway:

The profession did expect a sluggish performance over the next 12 months, but certainly no big recession. Importantly, when this forecast was made the profession was fully aware of the severe housing slump, and also the stress on the banking system. Banks had already sharply tightened lending standards due to the subprime fiasco. It’s true that Lehman had not yet failed, but that’s just one bank. And soon after the Lehman failure the other big banks were bailed out.

The profession did expect a sluggish performance over the next 12 months, but certainly no big recession. Importantly, when this forecast was made the profession was fully aware of the severe housing slump, and also the stress on the banking system. Banks had already sharply tightened lending standards due to the subprime fiasco. It’s true that Lehman had not yet failed, but that’s just one bank. And soon after the Lehman failure the other big banks were bailed out.

In September 2008, the Fed met and decided not to ease policy after Lehman failed, because they were worried that the economy might overheat if rates were cut. So even after knowing about everything that supposedly caused the Great Recession, the Fed was not expecting this economic outcome after Lehman failed. More importantly, there was little criticism of Fed policy at this time, which represented something close to the consensus view of the profession. (In contrast, I was quite critical of the Fed.)

Before explaining how the profession changed its mind, I’d like to emphasize one point very strongly. Although my current view of the Great Recession is now regarded as wildly implausible, it was close to the standard view as of mid-2008. That is, severe housing slumps combined with highly stressed banking industries do not cause big recessions. You may not agree that I am correct, but it’s important that you see that this was the standard view a decade ago.

So then what happened?

1. My view is that tight money caused NGDP growth to plunge, and this led to both the Great Recession and also worsened the housing/banking crisis. This view might be right or it might be wrong, but it’s certainly consistent with mainstream macro circa 2008. Today it’s a highly heterodox view.

2. The other view is that the housing/banking crises caused the Great Recession. This view was once heterodox, but is now standard.

Why did economists abandon the mainstream view circa 2008? You could argue that there was new information; they saw a housing/banking crisis followed by a Great Recession. But why assume any causal link? Why not just assume that is was tight money that caused NGDP to plunge? After all, history is littered with dozens of examples of financial crises associated with severe recessions, including the early 1930s. It’s not like we learned anything new from 2008-09. We didn’t learn anything that we didn’t already know before the Great Recession. Why change the standard model?

This reminds me of science in ancient times. There’d be an eclipse and then a week later a severe earthquake. The priests would claim the eclipse somehow made the earthquake inevitable. The Great Recession is now seen as being caused by housing/banking problems, because it followed housing/banking problems.

Actually, a severe recession was still not inevitable in mid-2008—it was excessively tight money that caused NGDP to plunge and unemployment to soar.

HT: Tyler Cowen

READER COMMENTS

Lorenzo from Oz

Aug 3 2018 at 8:09pm

And a tendency for monetary policy to not cope with the upsurge in demand for money that financial crises generate would be sufficient to generate the tendency for recessions to follow financial crashes.

Also, perhaps there should be a study: herd behaviour among economists.

Benjamin Cole

Aug 3 2018 at 8:56pm

Macroeconomics is often just politics in drag.

The 2008 collapse happened on the watch of President George Bush.

The GOP quickly launched a narrative that the collapse was caused by lax lending to urban D-party residents, forced by the Clintons, CRA and other federal regulations.

A bona fide contributing factor to house price instability, that is property zoning, has yet to be fully recognized by the macroeconomic profession. You have the “invisible hand” in free markets but in property markets you have the “invisible man”—-that is, property zoning.

And for reasons that appear to be buried deep in right-wing DNA ( or maybe is just a variant of class warfare) any deviation from tight money rigidity is regarded as a prime determinant of financial doom.

In this particular case, the macroeconomics profession appeared to subscribe to GOP dogma. Who knows how think tanks and academia are funded.

By the way, I think left-wing and Democratic Party dogma are just as bad.

Politics determines which totems are sacralized .

Add on: are not these recent studies just Hyman Minsky all over again?

Dylan

Aug 3 2018 at 9:33pm

OT, but I was wondering if you’ve had a chance to review this paper on GDP forecasting from a team of physicists?

http://www.nature.com/articles/s41567-018-0204-y

Scott Sumner

Aug 4 2018 at 1:03am

Lorenzo, Good point.

Dylan, I’m generally not particularly interested in that sort of study, as I don’t think those sorts of models are reliable. I prefer market forecasts.

Jerry Brown

Aug 4 2018 at 4:30am

In some ways Scott you are like one of those ancient priests you mention. In that you believe monetary policy as can be practically applied by the Fed is always the cause of everything economic. The housing price crash followed by/causing the banking crisis and recession has a reasonably logical story behind it, one that includes the time lags you mention. Nothing like an eclipse causing an earthquake.

Super simple story- A lot of overleveraged people had to cut back on their spending and then, eventually, could not pay back what they borrowed. Causing some overleveraged financial institutions to fail and other banks to frantically try to reduce their risks and not lend. Causing more people to reduce their spending. It is hard for me to see how easy monetary policy applied at that point really changes anything. If the Fed caused the great recession it was in the years before when it may have allowed some banks to extend so much credit while doing such bad underwriting.

Philo

Aug 15 2018 at 1:11pm

“It is hard for me to see how easy monetary policy applied at that point really changes anything.” No, Jerry, it’s easy: pumping up the money supply increases spending.

Alan Goldhammer

Aug 4 2018 at 8:28am

I’m not an economist, just a humble investor who tries to make sense of what is going on in the economic world. I understand (I think) where Scott is coming from and have done a lot of reading on NGDP. However, one cannot overlook all the bizarre financial derivatives that were created in the run-up to the Great Recession. Once one of the cards at the bottom of the house of cards fell, things started to get bad in a hurry. We had the ‘shadow banking’ system that was beyond the Fed’s reach react in a really bad way. Were it only Lehman who was in trouble, that failure alone would not have caused all the trouble but the systemic rot was in a lot of places.

There were enforced bank mergers that attempted to solve some problems (we had a Wachovia checking account one day and the next it was Wells Fargo!!!). AIG was on the hook for a lot of greed and in the end rotten business decisions. Perhaps the definitive history still remains to be written though Andrew Ross Sorkin’s book, “To Big to Fail” makes for compelling reading but is not as analytical as Roger Lowenstein’s “When Genius Failed” about Long Term Capital Management.

We will never know what the magnitude of the meltdown would have been had steps to stabilize all this ‘rot’ not been taken. I don’t think any discussion of the financial meltdown can ignore this aspect of leverage gone amok.

Meets

Aug 4 2018 at 2:58pm

Scott, why not write a paper on this? Would it get publiahed?

Scott Sumner

Aug 4 2018 at 5:14pm

Jerry, You said:

“In that you believe monetary policy as can be practically applied by the Fed is always the cause of everything economic.”

Obviously you are not familiar with my views–I suggest reading some of my older posts.

As far as the housing story “making sense”, if it’s so logical why didn’t economists accept this view in 2008? And why was the recession much worse in Europe?

Meets, I’m working on a book.

James

Aug 4 2018 at 7:43pm

Scott,

You wrote above “I’m generally not particularly interested in that sort of study, as I don’t think those sorts of models are reliable.”

Isn’t the reliability of predictive models something that is determined by measurement (out of sample rmse) rather than by thinking?

Jerry Brown

Aug 4 2018 at 7:43pm

Well Scott, I’ve been reading your blog The Money Illusion since around 2012. I realize that is no guarantee that I haven’t been misinterpreting your writing that whole time of course. But if I have, more reading probably won’t be the solution.

As to why economists might have changed their mind since 2008? Well the facts changed. I’m under the impression that a fair amount of economists (or at least some of them) in the early 2000’s thought the Fed had basically solved the business cycle, and that we would not see large recessions again. That was obviously not the case and even the more stubborn had to recognize we had a fairly deep recession by 2009 I would think.

Why was the recession so much worse in Europe? Well many of the countries use the Euro which limits both their own monetary policy, but also fiscal policy. Plus, I think many of the European Banks were in even worse shape and more overleveraged than US banks.

Jerry Brown

Aug 8 2018 at 4:38pm

“Before 2008, both academic macroeconomics and macroeconomic policy were strongly committed to the notion that conventional monetary policy, operating through a single overnight interest rate, was fully sufficient to offset any fluctuations in aggregate demand. The complacent view of future Obama administration CEA chair Christina Romer, offered on the verge of the crisis, is typical: “The Federal Reserve is directly responsible for … the virtual disappearance of the business cycle in the last 25 years… The story of stabilization policy in the last quarter century is one of amazing success. … We have seen a glorious counterrevolution in the ideas and conduct of short-run stabilization policy.” (Romer 2017)”

Just a short excerpt from a much longer post by J.W.Mason.

http://jwmason.org/slackwire/macroeconomic-lessons-from-the-past-decade/

keenan

Aug 7 2018 at 11:12am

Scott,

I think a good analogy for your approach to monetary policy is someone steering a ship towards dead north. The wheel is straight, all is good to start. However, *for some reason*, the ship starts to veer 45 degrees East. If the captain turned the wheel 30 degrees West, so the ship was now going 15 degrees East, the public/economics profession may very well say “the captain is being accommodative”. Especially if the wheel has never been more than 30 degrees in either direction before. However, you would say, it’s not accommodative *enough*. The captain should turn the wheel 45 degrees West: that is his job.

When you say “tight money caused NGDP growth to plunge”, it seems you are saying just this. The captain only turned the wheel 30 degrees, not 45. But I think it would be very useful if you addressed WHY the ship started going 45 degrees east in the first place. I’m guessing your answer is “I don’t know”, which is fine. But, I think it’s confusing to people when you say “the ship is going too far East because the captain is causing it to go too far that way”, when in reality he’s just doing his job poorly, and some outside force (wind maybe) is causing him to change the wheel’s position.

Yaakov

Aug 7 2018 at 6:59pm

I think Lorenzo made a very important point. I think the way to convince that you are right is to discuss the mechanism which produces tight money.

Corey

Aug 8 2018 at 4:28pm

What else happened in the summer of 2008? Oh yeah, $160 oil! I’m amazed that nobody lists that as a contributing factor.

bill

Aug 9 2018 at 4:00pm

I’d add that until late 2007 or so, the consensus was that the housing crash would be caused by Rising interest rates on all the ARMs.

People defaulted on their mortgages in spite of the rates falling 400 to 500 basis points because they lost their jobs. They lost their jobs because of Fed mistakes. If the unemployment rate had remained steady, there would have been no foreclosure crisis, far fewer bank failures, etc.

TMC

Aug 15 2018 at 3:22pm

Seems to be similar to the great depression. Bernanke was famous for being a student of the depression, but seemed to get weak knees when it came around again.

Scott Sumner

Aug 15 2018 at 10:22pm

Jerry, You said:

“That was obviously not the case and even the more stubborn had to recognize we had a fairly deep recession by 2009 I would think.”

Why would that change the way economists look at business cycles? Didn’t AD fall sharply? That’s what we’ve always thought causes deep recessions.

Keenan, I don’t really like that analogy, at least for the period around 2007-08. It wasn’t just a failure to offset wind, it was reckless turning the steering wheel.

Yaakov, I’ve done that in many posts.

TMC, Bernanke had opposition from within the Fed.

Comments are closed.