During the period following the 2020 Covid pandemic, many countries experienced relatively high inflation. This reflects two factors:

1. All countries were hit by shocks such as Covid-related supply chain disruptions and the Ukraine war.

2. Most countries enacted very extensive stimulus programs, which had similar effects in each case.

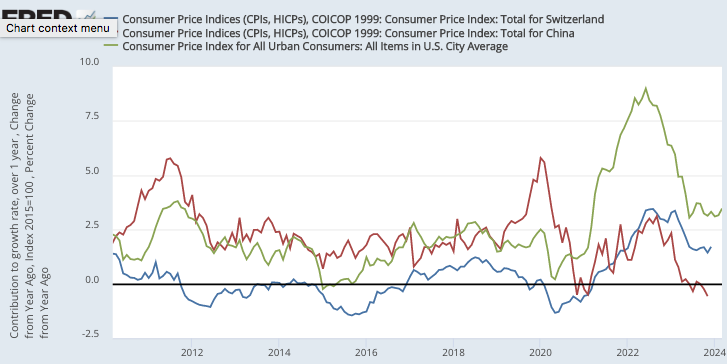

It was appropriate to allow some increase in inflation in response to negative supply shocks. That’s the whole idea behind “flexible” average inflation targeting. But the actual rate of inflation also reflected excessive aggregate demand growth, and thus was inappropriately high in many countries, including the US. I worry when people seem to suggest that there wasn’t much the Fed could have done about the inflation surge because it also occurred in many other nations. In fact, not all countries experienced extremely high inflation. Notice that China (red line) and Switzerland (blue line) experienced some increase in inflation, but much less than in the US (green line):

In a podcast with David Beckworth, former Fed vice-chair Richard Clarida suggests that the similar pattern experienced by most countries suggests that differences in monetary policy regime were not crucial in this particular case:

The most important thing to remember about the lessons learned from the inflation surge post-pandemic is that it was very similar across countries, across implementation, and across policy strategies. So, single mandate inflation targeters, like the Bank of England, inflation was too high. Single mandate inflation targeters, for the Eurozone, inflation was too high.

Inflation was too high in Switzerland. It was too high in Australia. It was too high in Canada. Moreover, with the exception of the SNB and the Norwegian Central Bank, all of the other advanced economy inflation targeters also chose to fall behind the curve, in that they did not begin to hike rates until core inflation in their country had moved well above target. So, it was something about initial conditions— inflation had been too low for a decade— about the magnitude and complexity of the shocks, because they impacted both supply and demand, that led central banks to do very similar things and to have very similar liftoffs, very similar inflation history, and now very similar disinflation.

So, I think and I predict that, with the passage of time, scholars will look back on this period and they will not think that it revealed very much about inflation targeting versus flexible average inflation targeting versus single mandate versus dual mandate. They think it will reveal something about the initial conditions and the magnitude and the complexity of the shocks.

I would argue that the cross country pattern we see suggests that some policy regime differences are more important than others. For instance, consider the case of China, which has seen its inflation rate fall to levels below even those of Japan, indeed to slightly below zero. Why might this have occurred?

It’s worth noting that Japan’s currency has recently depreciated very sharply against the US dollar, whereas China’s currency has depreciated only very modestly. Some pundits have suggested that China is reluctant to allow a sharp currency depreciation for fear that it would trigger a protectionist response in the US. Whatever the reason, China seems to have fallen into an excessively tight monetary policy because it is reluctant to allow a dramatic fall in the foreign exchange value of its currency.

This is one more example of where the price of money approach to policy can be much more powerful than the interest rate approach, a point I emphasized in my recent book. Once China decided not to allow a sharp fall in its nominal exchange rate, it could only achieve an equilibrium real exchange rate by allowing price level deflation. A similar pattern occurred in Argentina in the late 1990s, when a fixed exchange rate combined with a strong US dollar led to price deflation.

PS. Nothing in the Clarida interview made me optimistic about the upcoming review of the Fed’s policy regime. It seems clear to me that, at a minimum, the average inflation targeting regime needs to be made symmetrical, but I don’t see Fed officials advocating that sort of change. I hope I’m wrong, but I expect more of the same—a policy “rule” that allows far too much discretion.

READER COMMENTS

Rajat

May 7 2024 at 12:52am

I’m glad you wrote a post on that interview, because I was similarly disappointed. I don’t see how one can say that the experience shows that differences in policy regime aren’t important. All it shows is that discretionary policy is fraught. My mind keeps going back to David Beckworth’s interview with Jason Furman in June 2021, in which Furman chided David for supporting NGDPLT:

This tells me that had the US had forward-looking NGDPLT back then, even if applied highly imperfectly, it would have likely avoided much of the excess demand inflation that subsequently transpired.

Scott Sumner

May 7 2024 at 1:44am

That’s right. None of the other central banks that also overshot their targets had any form of level targeting.

robc

May 8 2024 at 11:37am

I made a comment on reddit yesterday about ngdp targeting and got the response of “Scott Sumner? Is that you?”

Scott Sumner

May 8 2024 at 12:54pm

No.

robc

May 8 2024 at 5:46pm

I think you misunderstood. Someone asked me if I was you.

I told them no of course.

marcus nunes

May 7 2024 at 8:29am

The Fed is not confident that inflation will move down to the 2% target!

(100) The pathway for Powell & the FOMC to gain confidence (substack.com)

Scott Sumner

May 7 2024 at 11:46am

In the short run.

Michael Sandifer

May 7 2024 at 5:42pm

I strongly suspect the Fed will move to a symmetric FAIT, but will not define the time period for the average. Also note that I think they will leave “Flexible” in the name, which will mean there will still be unnecessary uncertainty in their target at times.

It would be better to specify a time frame over which to average 2%, as you pointed out previously, at say 10 years, but I don’t think that will happen. And leaving in the word “Flexible” will reserve additional discretion that they shouldn’t have.

It’s progress, but very incremental.

Jonathan

May 8 2024 at 12:23pm

Something is strange about this story. The US has experienced high inflation relative to China and Japan, which would typically cause the dollar to depreciate against the Yuan and Yen. Yet the Yen has depreciated, and you say that China has had to run very tight monetary policy to avoid a depreciation of the Yuan. This implies a significant real appreciation of the dollar. What is the cause of this? A strong US economy relative to China and Japan?

Scott Sumner

May 8 2024 at 12:55pm

Partly a strong economy (and stock market), partly the high real interest rates associated with big budget deficits, etc.

The dollar is also strong against most other currencies.

Comments are closed.