The global economy experienced an inflationary boom during 2022. Prices rose rapidly and unemployment fell close to historical lows. This is what happens when you get excessive demand stimulus—fast rising NGDP and high employment. So how did traditional models do in 2022?

In a new Bloomberg column, Tyler Cowen points out that 2022 was a good year for traditional macroeconomic theory. We saw a great deal of monetary inflation, and we saw that the old rules regarding opportunity cost still apply. Here’s Tyler:

Not long ago, economists insisted that demand shortfalls were perpetual and that stimulus was almost never excessive. That extreme version of the Keynesian view has been laid to rest, while a version of Milton Friedman’s monetarism is ascendant once again.

Nonetheless, I see a few problems with Tyler’s analysis:

One of the most classical of economic lessons is that supply constraints truly matter. Along these lines, energy price hikes, most of all in Europe, showed that downturns and recessions can be brought on by old-fashioned scarcity. Sadly, this was the year that Nobel Laureate Edward C. Prescott passed away. Critics mocked Prescott for emphasizing the supply side as a force behind business cycles, but this year showed that Prescott was right. If not for the war in Ukraine and its associated energy supply disruptions, the global economy would be in much better shape.

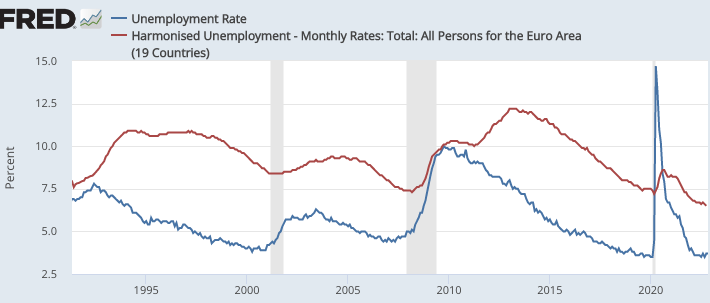

In fact, Prescott’s “real business cycle theory” cannot explain the business cycle, and 2022 was another example of this failure. Fluctuations in employment are driven by changes in NGDP growth, whereas real factors play only a minor role. In both the US and the eurozone, the unemployment rate fell close to an all time low during 2022:

An expansionary monetary policy in 2022 generated fast NGDP growth, and that’s why we saw such robust job creation. Real business cycle theory has never provided a plausible explanation of fluctuations in the unemployment rate in highly developed economies such as the US. (Developing countries are a different story.) Notice that RBC theory doesn’t even explain the (booming) labor market in Europe, which was affected much more directly by the Ukraine War. Economists should focus on NGDP when explaining the business cycle, and real factors when explaining long run growth trends.

It is possible that there will be a recession in 2023, but if there is it will be caused by a sharp slowdown in NGDP growth. It is fluctuations in NGDP (i.e. monetary policy) that drive the business cycle. Real shocks do affect living standards, but have little impact on the business cycle.

I would also reject Tyler’s claim that RBC theory is part of traditional macroeconomics. It is a contrarian theory that is rejected by most macroeconomists, at least as an explanation of business cycles. So in that sense the recent failure of RBC fits in with Tyler’s broader claim that contrarian theories did poorly in 2022.

Meanwhile, Tyler has this to say about the UK:

As for the UK: Economists predicted that a move away from free trade with the EU would hurt the British economy. And it has.

Tyler is 100% correct about Brexit. But there is no discussion of the Liz Truss fiasco. Truss’s proposed budget provided an almost textbook example of reckless fiscal stimulus. After the markets reacted very negatively, the Conservative Party replaced her with a more orthodox figure—Rishi Sunak. Perhaps this oversight is due to the fact that in this one area it was Tyler himself that was a contrarian:

I know an unpopular economic policy when I see one. And the consensus among economists about the tax cuts and deregulations announced last week by UK Prime Minister Liz Truss is almost universally negative. Larry Summers noted: “I think Britain will be remembered for having pursued the worst macroeconomic policies of any major country in a long time.” Willem Buiter described it as “totally, totally nuts.” Paul Krugman is skeptical. As Jason Furman summed it up: “I’ve rarely seen an economic policy that is as uniformly panned by economic experts and financial markets.”

The contrarian in me rebels against such harsh assessments — even as I remain unconvinced that Truss’s plan will materially boost the rate of economic growth in the UK. Allow me to explain why I am not in a state of panic.

READER COMMENTS

Thomas Lee Hutcheson

Dec 30 2022 at 11:49pm

Greater than expected shocks are reasons for a central bank to temporarily raise inflation rate above target (assuming the target had been optimized or average shocks) and they may be asymmetrically prone to raisin too uv more tan raisin too little

TGGP

Dec 31 2022 at 2:26am

I recall it was Tyler who said that prior to the arrival of central banks, most business cycles were real business cycles. Perhaps he forgot that Europe has central banks 🙂

Andrew Wallen

Jan 2 2023 at 11:24am

I don’t know if 2022 saw robust job creation as much as it was people continuing to return to work after COVID. The 2019 pre-COVID employment level was 157,530K and the 2022 employment level was 158,276K … ~0.5% growth which is below historical norms for year over year growth.

As a side note, if we are evaluating the strength of the economy, should we be normalizing the unemployment rate with the labor participation rate given the secular decline in the participation rate since ~2000? If we normalized to 2006 (i.e., the 2022 unemployment rate if the labor participation rate was at 2006 levels) then unemployment would be much higher (~9.4%). This may give us a better idea of the strength of the economy with respect to the labor market because it includes a measure of the incentive people have to engage in the workforce.

Scott Sumner

Jan 2 2023 at 1:26pm

That’s not a good idea. Unemployment is supposed to measure people who are looking for work but cannot find jobs. There are relatively few such people in today’s economy. Changes in immigration, boomers retiring, long Covid, and many other facts affect the trend rate of growth in the labor force. You cannot simply extrapolate.

Grand Rapids Mike

Jan 3 2023 at 9:58am

Lot of factors involved, besides excessive government spending there was excessive M2 growth 2020 and 2021. In 2022, government spending continues, M2 growth stopped by no real contraction and real interest rates still negative, On supply side prices spiked because of the Ukraine War and no growth in energy production. The spike was only abated by release of oil from SPR. While unemployment is technically low, lost of men just not seeking work, when benefits exceed to need to work, resulting in higher labor cost.

Now the prime negative going into 2023 is stock decline and bond price surge that really hurt using investments for retirement & spending. That puts a negative on growth, but government spending is charging along and M2 from 2020 and 2021 still high. Anyone willing to forecast 2023, does M2 the way Friedman said. So what model is the right one for getting all these factors in play.

Comments are closed.