Most fiscal policy consists of adjustments in taxes and transfers. However, the effects of this type of fiscal policy are largely offset by changes in monetary policy, at least when the Fed is doing its job. Defenders of fiscal policy respond that changes in real government spending can directly boost output even when there is complete monetary offset of the effects of budget deficits on nominal spending. In practice, however, even this sort of “real” fiscal stimulus is unlikely to be effective at stabilizing the economy, as Congressional decisions to spend money on new projects is driven by political factors, not the state of the economy. Here’s the National Review:

As New Hampshire GOP governor Chris Sununu observed, Congress allocated $1.2 trillion for new infrastructure projects, but none of it has been spent yet, which means yet another inflationary pressure is looming. What’s more, 50 states and an untold number of localities are about to try to launch hundreds of large-scale infrastructure projects simultaneously during a period of runaway inflation, lingering supply-chain problems, price spikes in raw materials, a construction-labor shortage, and an unprecedented spike in the cost of diesel fuel. This is just about the worst possible time to try to start a massive number of construction projects from coast to coast.

Of course it is possible that these projects will get built during the next recession. But it’s also possible that they won’t get rolled out until the next recession is over. We just don’t know.

Intuitively, one might assume that a series of random fiscal shocks would make the business cycle neither more nor less unstable. After all, random fiscal stimulus would be just as likely to occur when economic output is above average as when it is below average. In fact, macro models suggest that adding random shocks to an unstable economy makes the business cycle even worse than otherwise.

The Covid fiscal stimulus was mostly taxes and transfers, and hence was subject to monetary offset. But even if you don’t believe that monetary offset occurred, the fiscal stimulus appears to have been a mixed bag. The early portions of the stimulus would have made the Covid recession less severe than otherwise, whereas the fiscal stimulus in 2021 would have contributed to economic overheating.

At the time, I argued that fiscal policy should focus on relief for the unemployed, not stimulus. Subsequent events have made me even more confident of that view.

At the time, I argued that monetary policy should focus on getting NGDP back up to trend, but not above trend. Subsequent events have made me even more confident of that view.

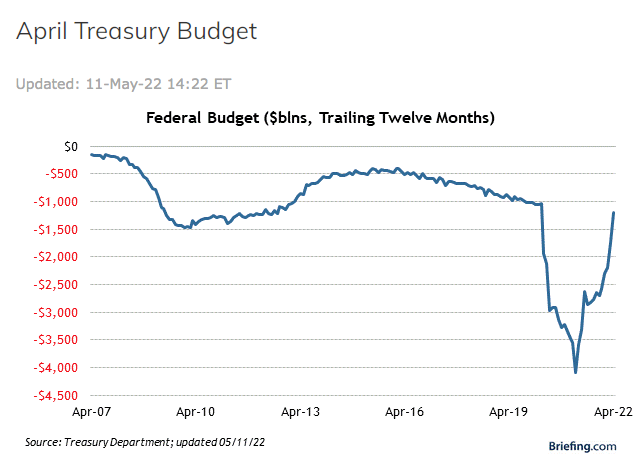

PS. Commenter Cameron directed me to a graph showing fiscal policy tightening over the past year. (Note: The graph shows the deficit, despite being labeled “budget”). This may be why many economists underestimated the recent inflation surge. If you (wrongly) assume that fiscal policy determines aggregate demand, then you might have assumed that the shrinking budget deficit would relieve inflationary pressures. But it’s monetary policy that drives AD, not fiscal policy.

READER COMMENTS

David Henderson

May 14 2022 at 6:07pm

That graph can’t be right. The budget was never negative.

dlr

May 14 2022 at 6:21pm

it’s the deficit

Scott Sumner

May 14 2022 at 7:20pm

Thanks David, I missed that. I added an explanation that it’s actually the deficit, not the budget.

David Henderson

May 14 2022 at 10:00pm

Oh, Ok. Thanks, Scott.

Richard A.

May 14 2022 at 7:32pm

One can make the argument that fiscal stimulus works by incrementally increasing the velocity of money, but if you look at the equation of exchange:

M x V = P x GDPr = GDPn,

if the Fed is controlling M based on what either GDPn is doing or what P and GDPr are doing, it will offset any fiscal stimulus.

Matthias

May 14 2022 at 10:33pm

I am mostly sympathetic to the claims here. Just one small niggle:

> As New Hampshire GOP governor Chris Sununu observed, Congress allocated $1.2 trillion for new infrastructure projects, but none of it has been spent yet, which means yet another inflationary pressure is looming.

I don’t know whether that’s a valid critique: the market anticipates monetary policy with long and variable foreshadowing.

Why would fiscal policy be any different?

Scott Sumner

May 15 2022 at 2:00am

I’m not sure how much impact it will have on inflation (perhaps not that much due to monetary offset.) The main point here is that to the extent that fiscal policy has an impact, it’s often poorly timed.

Matthias

May 15 2022 at 2:42am

I can believe that fiscal policy is poorly timed.

I just think a rigorous critique probably has to talk about when fiscal policy spending announcements (or announcements of austerity) first become credible or can be guessed with sufficient certainty.

As an alternative, you can also argue to what extent actually spending is more important in timing than the anticipation.

When I grew up in Germany, I remember hearing a lot of talk in the media about automatic stabilisers. The idea that welfare spending automatically goes up in a recession while tax take goes down. That’s also an example of something that can be anticipated by the market very well.

Thomas Lee Hutcheson

May 15 2022 at 7:31am

“Fiscal” policy should not be about macroeconomics at all. Investment and relief should proceed according to NPV analysis which is affected by temporary downward departures of market prices from marginal costs (unemployment) and lower borrowing costs, making some greater spending during recessions a good idea, but this is not of much importance for infrastructure.

Njnnja

May 15 2022 at 7:42pm

Maybe it’s in another post, but how much do you think of the fiscal policy decisions relied on the MMT framework, and might not have been done without those theoretical underpinnings?

Scott Sumner

May 15 2022 at 8:57pm

I doubt that MMT had much influence. Do you know a single influential economist that takes it seriously? And the policy began under Trump, which makes MMT influence seem even less likely.

vince

May 16 2022 at 12:07am

MMT policy began under Trump? Nice try.

Jon Murphy

May 16 2022 at 7:14am

He said MMT hasn’t been the guiding policy, neither under Trump or Biden.

vince

May 16 2022 at 12:04am

“monetary policy should focus on getting NGDP back up to trend”

What is NGDP trend, and how do you get it there?

Scott Sumner

May 16 2022 at 1:17pm

The trend has been roughly 4%/year, although you can argue it’s slowing now with the drop in population growth.

vince

May 16 2022 at 7:33pm

If it’s 4 percent, wouldn’t that suggest no change in policy, and wouldn’t that leave the inflation path as is.

Michael Sandifer

May 16 2022 at 11:53pm

Right now, the expected NGDP growth path is at about 4.29%, with roughly 1.6% being real, given expected core PCE inflation. The end of the Ukraine war would lower inflation and raise RGDP somewhat, as would the end of pandemic related supply problems.

Population growth that’s trending close to zero and below will be a headwind for real growth, but we’re also in the early stages of an AI revolution that could eventually have an effect on productivity greater than that of electric power. That time frame for the productivity boom is very uncertain, of course.

The electricity boom even helped spur relatively high productivity growth during the Great Depression.

vince

May 17 2022 at 12:27am

What’s your point–leave the inflation path as is?

Scott Sumner

May 17 2022 at 12:47pm

NGDP growth has recently been running at 10%; that’s way too high. Even compared to 2019 the rate is too high, despite the huge Covid slump.

Brian

May 17 2022 at 7:47am

You wrote… “At the time, I argued that fiscal policy should focus on relief for the unemployed, not stimulus.”

To what extent was the CARES Act of 2020 which sent $1200 to tax filers that earned less than $75k per year motivated by the fact it was an election year? Who’s idea was it? Was Kevin Hassett for or against the $1200 cheques and did members of the Council of Economic Advisors say anything against it publicly?

Capt. J Parker

May 17 2022 at 11:01am

The Fed’s performance over the past year suggests:

Monetary policy is quite happy to work in concert with Fiscal policy

Monetary offset does not exist (Or exists only at full employment)

The Fed is still guided by a Phillips approach to managing the employment level

Larry Summers correctly predicted the current inflation problem. In his model, fiscal policy seems to reign supreme, even to the point of his suggesting fiscal policy is an effective way to control the current inflation.

Scott Sumner

May 17 2022 at 12:50pm

“Monetary offset does not exist (Or exists only at full employment)”

Monetary offset occurred in 2013, despite being nowhere near full employment.

The correct answer is that monetary offset occurs on some occasions, and not on others.

Comments are closed.