Over the past 90 years, the public has frequently been warned that the US budget deficit would lead to an economic crisis. As in the famous story about the boy who cried wolf, they eventually began to tune out those warnings. And it does no good to cite specific data about the budget deficit rising to hundreds of billions or even trillions of dollars; those figures have no meaning to average people. I suspect that if you polled people on the consequences of a $800 million deficit and a $800 billion dollar deficit, the answers would be similar.

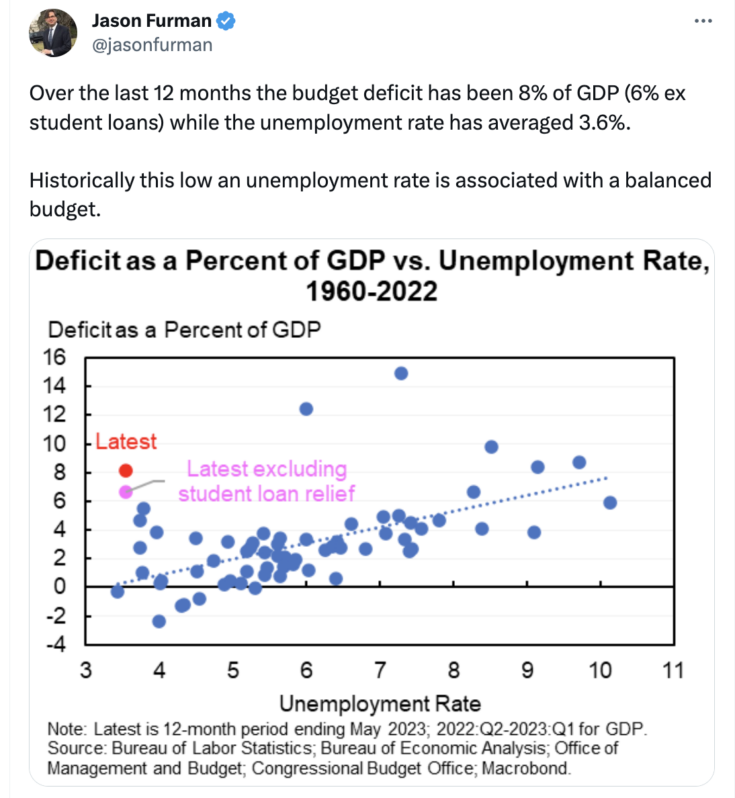

But this time is different, as something important has changed. The wolf is not yet at the door, but it’s getting closer. Over the past 5 years, the US budget deficit has shifted to a more unsustainable path. Matt Yglesias directed me to this tweet by Jason Furman:

The dotted line is upward sloping because deficits are typically worse during periods of high unemployment, which is as it should be. The further above the dotted line, the more out of line the deficit, given the condition of the business cycle.

Back in 2019, I argued that US fiscal policy was the most reckless in US history. It’s not that the budget deficit was all that high (4.6% of GDP), rather it was unusually high given that unemployment was near an all-time low. I knew that things would become far worse in the next recession, although I did not know that the recession would come so soon.

I stand by my claim that (at the time) 2019 fiscal policy was the most reckless in American history, even though each of the next 4 years ended up being even more reckless. In terms of vertical distance above the dotted line, 2020 was the very worst, then 2021, then 2023 (estimated—red dot), then 2022, and then 2019 (roughly tied with 2009.)

The consequence of the reckless fiscal policy will not be a financial crisis. Nor will it be a default. Even the permanent monetization of the debt is unlikely, in my view. The most likely consequence will be higher future taxes and slower economic growth. This will lead to reduced living standards. It might also push politics in a more “populist” direction, with consequences that are difficult to predict (but unlikely to be desirable.)

P.S. The distinction between higher taxes and lower spending is less clear than you might assume. Thus one option is a $1000 tax increase on rich people. Another option is a $1000 cut in Social Security benefits for rich people. The first represents higher taxes while the second is lower spending. But the consequences for implicit marginal tax rates are quite similar.

READER COMMENTS

spencer

Jun 9 2023 at 2:55pm

Link: Fiscal Dominance and the Return of Zero-Interest Bank Reserve Requirements (stlouisfed.org)

“imposing high reserve requirements for zero-interest paying reserves may seem quite attractive to a policymaker interested in reducing the inflationary consequences of fiscal dominance.”

spencer

Jun 9 2023 at 3:14pm

Our twin deficits have an insidious, if not an incestuous, relationship. Positive interest rate differentials are significantly responsible for the dollar’s exchange rate support. And an “overvalued” dollar in turn is the principal contributor to our burgeoning trade deficits.

Carl

Jun 9 2023 at 8:42pm

I’ve heard a number of theories explaining why we are fiscally profligate. There’s the Triffin Dilemma, Cost Disease Socialism to name two. I’m curious what you think is driving our fiscal profligacy.

Scott Sumner

Jun 10 2023 at 11:16am

The problem only began in the late 2010s. Prior to that, the fiscal policy was sustainable.

What changed? The US became more populist, more like a banana republic. Not a serious country. I’m not sure why.

Thomas Hutcheson

Jun 10 2023 at 12:30pm

My analysis is a , decline in the “feeling” that deficits are bad, leaving both parties “free” to be irresponsible about not taxing enough to cover the expenditures they favor (or don’t dare to cut).

vince

Jun 10 2023 at 1:04pm

Response to the GFC and its bailout? Employment dislocations due to globalism? The Kardashians?

steve

Jun 11 2023 at 4:05pm

Debt has been increasing for a lot longer than the 2010’s. I think it goes back to the 80s. Remember that Cheney said this. “”Reagan proved deficits don’t matter,” Cutting taxes while not cutting spending gains you lots of votes. It looks like you are getting lots of govt services for free. We got lucky and had a brief period in the late 90s where debt was prioritized but now it seems everyone believes that you can cut taxes or increase spending with our consequences.

Steve

Scott Sumner

Jun 11 2023 at 5:21pm

“Debt has been increasing for a lot longer than the 2010’s.”

But until recently, the increases were at a sustainable pace.

Thomas Hutcheson

Jun 9 2023 at 9:22pm

Let’s HOPE the result is higher taxes, that’s a lot better than the alternative. Especially if we we moved personal taxes toward consumption taxes, financed the social safety et with a VAT, and rebated less than total collections of the taxon net CO2 emissions.

spencer

Jun 10 2023 at 10:26am

It was axiomatic and a gaffe. Keynesian economists have achieved their objective: that there is no difference between money and liquid assets.

“A rise in inequality, trims net wage growth and thus economic growth and prosperity.” And “The persistent trade deficit kills domestic industries and real wages”. “Living standards, the take-home production wage, has dropped since 1973.” “Manufacturing employment peaked in 1979.” “Consumer credit accelerated after 1980.”

Importantly, “if demand and supply are to be balanced over time, then either wages rise in sync with productivity, or productivity growth must be matched by the growth of wages plus debt”

“Demand = Consumption + Investment + New Debt” – Ravi Batra in his book “Greenspan’s Fraud”

vince

Jun 10 2023 at 1:01pm

Why not inflation? Stagflation? We might be on that path now.

Michael Sandifer

Jun 10 2023 at 8:25pm

This is not so surprising to me. I’ve long thought that once the baby boomers began retiring, budget deficits and the debt would shoot way up, as we’ve long been a country that has problems making decisions on spending and taxes that would avoid such a situation. We don’t have government that likes to tell people that there are limits. That’s probably because many voters don’t understand much about reality.

This was evident not only in our fiscal policy, but our foreign policy. Many voters who used to be blind hawks, are now blind isolationists, after feeling they were duped about the situations in Iraq and Afghanistan. Ignorant people flow between extremes, as they only know enough to understand that a policy isn’t going well after many years, and extremely high costs.

I also am not surprised we’ve headed more in a banana republican direction, though we’ve gone farther, faster in recent years than I imagined. I didn’t predict the Republican leadership would be so led by its increasingly extremist base. They’re willing to follow their base off a cliff, even politically, as long as they can get some tax cuts for the wealthy and certain other special interests.

They actually want to create fiscal crises that Republican Presidents never address, because they know Democrats are politically stupid enough to try to address them when in office. Republican leaders are Keynesian when in office, and spend to get us closer to a sense of fiscal crisis in what is ultimately a “starve the beast” strategy, 100% in support of plutocrats.

Just look at proposals this year to cut spending on social programs by $3 trillion over the next 10 years, coupled with additional tax cuts of $3 trillion over the same horizon. They don’t hide what they’re doing. They know they will always get away with it. They don’t talk about fiscal policy at all, unless Democrats hold the White House.

Democrats have learned some of the wrong lessons. They are now more willing to run deficits to try to run the economy hot to get unemployment down and keep it down, and are also adopting industrial policies which satisfy voters in important electoral college swing states, while trying to appeal to less educated working class voters that have increasingly turned to Republicans. It’s understandable in a way politically, and perhaps even inevitable if we want to keep increasingly dangerous Republicans out of office.

Meanwhile, we have a growing culture war, as Democrats bendover backwards to try to keep its minority/women coalition together, while Republicans attack modern culture and all of its recent changes as part of a broader inability to adapt to an increasingly rapidly changing world. Republicans have no policies to address the economic insecurities of voters, caring only about serving the plutocrats, so they engage in culture wars to win votes from the most primitive people in the electorate.

Hence, increasingly, the Republican Party is a scam organization in which leaders constantly lie to voters to tell them what they want to hear, while only serving their career interests vis-a-vis the plutocrats. Many openly steal money raised from various scare campaigns, and/or sell sham books, and other media, or scam dietary supplements, gold and crypto investment schemes, etc. Republicans are increasingly old and foolish and easy to rob blindly.

Many candidates who run for office these days, especially on the Republican side, have no interest in the office itself, accept as a vehicle to grow their fame and fortunes. These are people who are essentially the professional wrestlers of public policy. It’s all about the show, with no substance whatsoever.

Pedactor

Jun 11 2023 at 10:11am

Debt and deficits don’t matter anymore. There are literally a billion buyers of U.S. debt and Eurozone countries much much older than the U.S. have horrendous debt to GDP ratios. Applying Austrian economics and supply side to what the world has become (it’s not sound money) is an echo-chamber move.

Global maritime security is DOMINATED by the US. The US military is hundreds of times larger and more advanced than the rest of the world combined. Man is an apex predator and the US debt is just a more civilized weapon. It will suck liquidity mercilessly into 5-7% treasuries to finance itself and will still provide savings to the Eurozone and Japan over true re-militarization. China has massive issues that aren’t being reported on. Illiquid debt loads tied to cities built for a population that doesn’t exist. 20+% youth unemployment.

Everything is relative. There is nothing anybody can do about it. Taxes won’t matter enough because only taxes and austerity would even make a dent over DECADES. And the pure truth is that the US is setup to dominate further over the next decade or so because it is the most desired debt. And that is all that matters.

MarkLouis

Jun 14 2023 at 7:15am

You are too sanguine. Neither party is willing to increase taxes, except perhaps to partially fund new spending. Inflation is unpopular with the electorate, but blaming the Fed seems to be the better strategy than reducing the deficit. The Fed is unwilling to offset excess fiscal spending in a timely manner. COVID programs are winding down but new spending was met with little Fed pushback or policy action. With inflation well above target, new fiscal spending should be met with almost immediate disapproval and rate hikes

A majority of our obligations are directly or indirectly linked to inflation (social security, healthcare, TIPS, military, etc). Nominal debt not already owned by the Fed isn’t huge therefore we can’t “inflate away our liabilities.”

A doom loop is possible: spending creates inflation which creates more spending; the Fed is perpetually behind the curve and willing to tolerate overshoots which results in more inflation, and thus more spending. This can become self reinforcing.

Scott H.

Jun 14 2023 at 12:59pm

The reasons we have these deficits are pretty simple:

1.) We have a moral panic about inequality and people believe gov’t spending reduces it.

2.) Too many people believe that they, ultimately, won’t be the ones paying for it.

3.) Many people believe they don’t care that much about economic growth anyway.

MarkLouis

Jun 14 2023 at 2:48pm

This isn’t surprising when you study history. It’s one reason we desire a strong and independent central bank. The surprise is that our central bank refuses to do what’s required to neutralize reckless fiscal policy. Inflation will probably get back to 2% eventually, but not before we experience a large and permanent jump in the price level.

Jim Glass

Jun 15 2023 at 1:11am

The reasons we have these deficits are pretty simple:

People everywhere want plush retirements without saving any money out of their incomes to pay for them. So governments that must needs please their populations promise such to them. (So the USA gets a real accrual-basis annual deficit of $4.2 trillion that is 3x larger than the “official” cash basis one.) That’s 80% of everything. Yeah, people want other free stuff too, but relatively small potatoes.

The fundamental, constitutional political-economic problem is that nobody owns a modern nation. The owners of a corporation will not allow it to assume massive unsustainable debts, as they must preserve its fiscal soundness or lose their own shirts. But nobody serves this role in government. Maybe we should revive a form of kingship?

Note, this is universal, not just the USA, and relatively speaking the USA is better off than most. The USA collects less tax than most advanced nations (allowing more room to increase tax without destroying the economy) and has a larger percentage of private saving in retirement plans than do many nations (relatively less need to slash benefits).

Back during the peak era of American civilization, the 1990s and early 2000s (when name-calling political arguments were over sane issues like privatizing Social Security and funding the deficit, instead of over masks and men being women) many economists, including conservatives like Mankiw, argued for the USA to enact energy taxes and consumption taxes like a VAT that would be offset by income tax cuts, as these would provide efficiency gains. Like the Europeans claimed to be doing. I argued, contra, that politicians don’t care a rat’s tail about efficiency, only maximizing revenue, so once enacted the energy and consumption taxes would be run up far above promised levels and income taxes wouldn’t be cut. And with the huge entitlement wave hitting in the 2030s, we needed to keep that tax capacity in reserve. Looking back now, I proclaim “I told you so!” on all counts. Most of Europe is significantly worse off than the USA.

Also note this is not a “democracy” issue. One of Putin’s biggest problems has been and still is pension politics. China may be the worst off of all.

Jim Glass

Jun 14 2023 at 10:49pm

For the record…

Since federal tax receipts last year were 19.3% of GDP, this requires a 22% increase in taxes, or a cut of spending by the equivalent (seniors say “Hi!”) or a combo of both in that total.

And it gets worse every year the issue gets punted down the road, of course, just as it has ever since 1983 when Social Security went bust, then was made solvent again (in a manner that requires then-younger participants to take a lifetime loss on it, as a class), for a while.

Jim Glass

Jun 14 2023 at 11:44pm

I blame Krugman. Back in the days of Bush the Lesser he wrote…

That was when when CBO had projected 10-year deficits of $1.8 trillion. Today the one-year deficit is $1.3 trillion and the 10-year projection is, IIRC, $18 trillion.

And that was the one thing PK said during all the Bush years that he was right about, as I told all my Krugman-bashing Repub friends of the time. But then Obama came in wuth the Democrats, and PK promptly executed a 180-degree flip turn to make Mark Spitz envious. (“Gosh, lots of countries have had more debt than the USA has. And entitlements? What’s an entitlement??”) As James Hamilton promptly pointed out.

When Paul abandoned defending the fiscal bridge, we all were doomed.

And for the record, it’s not the current deficit & debt course that’s the problem. It’s the $100+ trillion at present value (last time I looked, a few years ago) of unfunded, off-the-books liabilities for Medicare, Social Security and federal pensions, which will start coming on the books in a big way in the 2030s. Those are cash obligations, inflation-adjusted. No way to inflate out of them. It’s going to be tax increases and spending cuts, period. As a certainty. No third option. Well, other than selling off assets like the Grand Canyon.

For decades now wits have been saying the US government is a health & retirement plan for seniors with nuclear weapons. The day may be coming when it can’t afford the nukes.

MarkLouis

Jun 15 2023 at 9:46am

Very good point on the size of our inflation-linked liabilities. Rarely discussed – especially by the “we have no choice but to inflate away our debt” crowd. Any attempt to do so will make our long-term problems worse.

If leadership changes in 2024, inflation will become Krugman’s #1 concern overnight. Guaranteed. More economists should speak out against blatant politicization of the subject.

Jim Glass

Jun 15 2023 at 12:15am

Aw, let’s not be spooked by that mere 8% of GDP, $1.4 trillion, deficit number. The federal government uses a cash-basis accounting system that’s so unreliable that the federal government makes it is illegal for any business larger than a small candy store to use. Those numbers are so bogus they shouldn’t scare anybody.

Happily, the Treasury also publishes decent accrual-basis accounting results, like real candy stores are required to use.

According to those, the one-year deficit for 2022 was $4.2 trillion, 3x more. And while the “official” deficit for 2022 was that $1.4 trillion, the one-year increase in the accrual basis deficit was $1.2 trillion.

https://www.fiscal.treasury.gov/reports-statements/financial-report/government-financial-position-and-condition.html#chart1

I hope all you reading this who are under age 50 are fully self-funding your future retirement years. If not, better start now. When Social Security went bust in 1983 benefits were cut and taxes on benefits were sharply increased. And that bust was *nothing* like the one that is coming.

Michael Rulle

Jun 15 2023 at 6:55am

It is very interesting that we believe increased deficits can be a positive thing. We never should have had SS or Medicare. What about our military? We built that pretty fast when needed. When government controls it makes things deranged, controlling, or sloppy, or whatever language Hayek would have used.

Isn’t it generally more efficient for private markets to do the spending? I cannot help but believe that deficits are a way for government to increasingly gain control and increased power. What did that stat guy (Keynes :-))believe? He believed we could refine deficits and then refine them back. except we could not.

Bastiat and the newsman (Hazle1t) eliminated the craziness of the so called “broken window theory” ——which is really a form of deficit spending.

I think Covid (I hope at least) was an another broken window concept. Why did we need taxes? Leverage? No. Taxes/spending is for power. We need it from time to time. Truman got rid of it fast however.

Imagine if Robert Moses types existed in every state? Nightmare.

Jim Glass

Jun 15 2023 at 1:10pm

We never should have had SS or Medicare.

There’s nothing fiscally wrong with the likes of them as long as they are funded. FDR’s original SS Act of 1936 was fully funded and “out of the Treasury forever”, running huge initial revenue surpluses to pay for future decades of benefits. He was so serious about that, that when he read the Act and discovered his minions had slipped in some Treasury borrowings in the 1960s (!) he had a famous tantrum, pulled the bill from Congress and had it re-written. Don’t we wish we had politicians like that today?

I cannot help but believe that deficits are a way for government to increasingly gain control and increased power.

Never assume deep, long-term conspiracy when immediate myopic greed will do. “Who wants free stuff?” “We do! We do!” “Great, we all agree!” FDR’s version of SS lasted until its tax revenue started coming in. Then Congress immediately slashed the tax rate (taxpayers: “Yea!), greatly boosted future benefits (workers: “Yea!”) and they all cheered the politicians who did it (politicians: “Yea! We all agree!”) FDR vetoed the changes and Congress over-rode his veto — the only time in his four terms. Because everyone agreed! Democracy in action! You support democracy, right?

FDR’s head of SS complained bitterly to Congress’s leaders that this would bankrupt SS in the future. Just as it did in 1983. Demographics is easy. He said they told him: We’ll be gone, it will be somebody else’s problem. It was *free* to them. Do you turn down free lunches? No deeper plan than that.

Isn’t it generally more efficient for private markets to do the spending?

Singapore has by far the most efficient health care in the world. Results are equal to or better than OECD best, at a cost of only 4% of GDP, half the OECD average cost (1/3rd of the USA’s). Medical tourism, foreigners coming for treatment, is a major industry.

It’s plan is ~80% government paid, taxes. But this government spending is through rigorously constructed markets. Everybody has a forced medical savings account. No insurance (almost). Doctors and hospitals must post transparent, competitive prices. No cost shifting. Everything is paid for out of pocket. This produces world-best market efficiency that the government benefits from when it pays its share.

How is all this efficient suppression of everybody’s individual freedom possible in a democracy? It isn’t. Singapore is a one-party state, our world’s closest thing to a “benevolent dictatorship”. Plato proved long ago that benevolent dictatorship is a far better form of government than stinkin’ democracy. The only problem is securing, you know, the “benevolent” part.

Comments are closed.