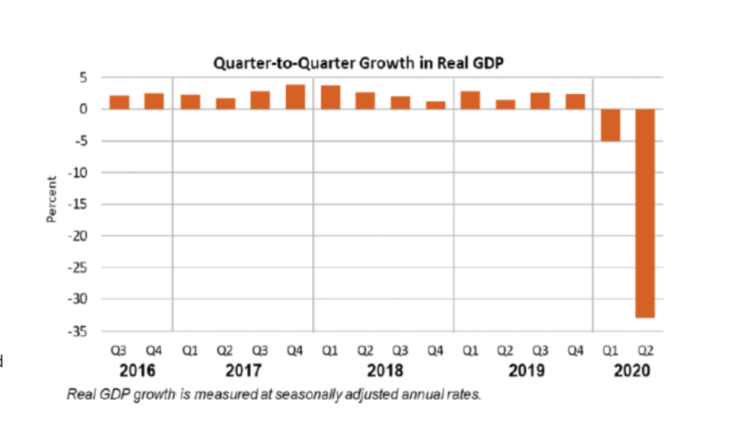

The second quarter of this year saw what is probably the biggest fiscal stimulus in American history, in terms of increase in the budget deficit. And today we see the results: nominal GDP fell by 34.3% at an annual rate. That means the fiscal stimulus prevented a much bigger fall in GDP—right?

Well, that might be true, but how would we know? We have models, but these models certainly don’t predict that NGDP would fall at a 34.3% rate in a quarter where disposable income is actually rising. And not just rising, but (according to the BEA) rising at an almost insane annual rate of 42.1%. In real terms it was even higher, due to deflation:

Real disposable personal income (DPI)—personal income adjusted for taxes and inflation—increased 44.9 percent in the second quarter after increasing 2.6 percent in the first quarter.

Why do I mention disposable income? Because the models that predict fiscal stimulus will boost the economy are based on a transmission mechanism that runs from more fiscal stimulus to more disposable income to more spending. Thus our (Keynesian) models don’t really explain why NGDP fell so sharply in Q2. Indeed, if anything these models predict an extraordinary boom.

You might respond that our common sense does provide an answer—people were afraid to go out shopping due to the virus. I accept that theory. But as far as I know there are no models that predict fiscal stimulus will be effective when people are afraid to go out shopping. And with the new Q2 GDP data there is also no empirical evidence that fiscal stimulus boosted GDP.

Before discussing the policy implications of all this, a few caveats:

1. Yes, I understand “ceteris paribus”. It’s plausible that the fiscal stimulus had some positive effect. After all, even during periods where the virus is the dominant factor, disposable income does matter at the margin.

2. A very large budget deficit in Q2 was appropriate, as standard public finance theory says you should take in less tax revenue during a severe slump, and spend more on unemployment compensation. Then there’s spending on the virus itself. I accept all of that. A big deficit was inevitable and appropriate.

What I question is the part of the deficit that was motivated solely by the desire to boost disposable income. For instance, why give $1200 to middle class people with stable jobs who were actually benefiting from a decline in the cost of living? That seems like wasted ammunition. What were they expected to do with the money? Why not just do enough stimulus to keep disposable income stable, if the problem is that people are afraid of spending? Why a 44% (annualized) real increase?

In fairness to the other side, the fiscal stimulus this time around was larger and timelier than I expected. I would have expected gridlock in DC to slow the process. Nonetheless, it seems plausible to me that the massive fiscal stimulus was mostly wasted, due to the reluctance of people to spend. Ironically, this might be the one recession where it would have been better to delay the fiscal stimulus until 2021. If we get a vaccine this winter (which experts seem to think increasingly likely) then perhaps people will become more willing to shop in 2021. That’s when the fiscal stimulus might have been effective, at least if you buy the underlying Keynesian model.

For myself, I believe monetary stimulus would be more effective in boosting the economy in 2021, at a much lower cost. Monetary and fiscal policy are very different. Monetary stimulus does not exhaust ammunition; rather it actually creates ammunition by raising the natural rate of interest. Fiscal stimulus really does exhaust ammunition.

Despite the preceding comments, I actually believe the economy received too little stimulus in Q2 of this year. I would have preferred to see monetary policy be expansionary enough to prevent disinflation. It wasn’t. So I’m not one of those conservatives who argue that “stimulus” doesn’t help in a slump. Rather, I favor monetary stimulus (which is basically costless) over fiscal stimulus that imposes a heavy burden on future taxpayers. If there’s a vaccine this winter, then I believe that monetary stimulus alone (done properly) could give us a V-shaped recovery.

In the past, I argued that fiscal stimulus did boost GDP in Q2 of 2008, but did not boost GDP for 2008 as a whole. That’s because the Fed responded to Bush’s spring of 2008 tax rebate by tightening money to slow inflation (CPI inflation peaked at 5.5% in mid-2008.) The rest is history.

In my view the recent fiscal stimulus did slightly boost NGDP in Q2, but the gains are likely to be taken away in 2021. We’ll do a bit less monetary stimulus in 2021 because of all of the fiscal stimulus done in 2020, money that was basically wasted.

PS. Yes, the unannualized drop in NGDP was much smaller than 34.3%, but still pretty horrific by historical standards.

READER COMMENTS

Max

Jul 30 2020 at 2:00pm

I did find this strange. Why not send money only to those who need it? Also, why one-time $1200? That doesn’t help anyone except those right at the bottom get through anything. Canada’s plan made a lot more sense.

Michael Pettengill

Aug 3 2020 at 6:03am

Its reflex. Since the 80s, tax cuts are given mostly to the high income people who can’t come close to spending all their wages. This has been dogma for getting the economy out of recession, increase growth, prevent a recession.

Never is the automatic tax cut given to low income people who get laid off who spend every dime, including what they pay in taxes, and thus end up using SS benefits to pay debts from years earllier.

I think this is due to wage income defining consumer spending thus defining business revenue which thus determines wage income.

Today, cutting consumer spending by cutting income is supposed to drive GDP growth higher.

Alan Goldhammer

Jul 30 2020 at 3:41pm

Scott – obviously disposable income is still substantial. I look at the spreadsheet I maintain for our finances and it is a big positive number. There is no place to spend money! We cannot go out to restaurants, movies, theater, concert, or on a vacation. All we have spent money on is food, utilities and that’s it. We bring in food once a week from a favorite restaurant. Most every one in my neighborhood is doing the same thing.

Even if a vaccine is available in six months, we are going to still be on the sidelines for another 3-6 months waiting to see if it works as promised. Personally, I’m skeptical of some of the vaccine candidates and won’t feel comfortable until we have 3-4 different types of vaccines. I am looking at the economy from a public health perspective as I’m not an economist. I just don’t see things getting back to more than 90% of where we were in January and only then if everything goes right.

Scott Sumner

Jul 30 2020 at 3:46pm

Actually, several companies hope to have vaccines approved this fall. My winter prediction was for widespread availability to the public. I’ll take it day one.

Philo

Jul 31 2020 at 10:33am

“I’ll take it day one.” But how will it be distributed? The government will probably take charge of the process, and you won’t be at the top of their priority list.

Mark Z

Aug 1 2020 at 12:23am

You’ll have to go to the DMV to get it, only open 11AM-2PM, Tuesday through Thursday.

Jose Pablo

Aug 2 2020 at 6:05pm

And they will take turns for having lunch from 12:00 to 1:00 pm

You will need and appoitment … the first available date will be in 3 months time

Olof

Jul 30 2020 at 5:17pm

If my calculator is not fooling me, the unannualized quarterly drop (also known as the normal way of calculating it) in NGDP was almost exactly 10%.

That should be helpful. It will probably be revised, but can be enjoyed while it lasts.

Shyam Vasudevan

Jul 30 2020 at 5:26pm

I think the design of the checks back in March was less from the standpoint of stimulus than from a “fill in the gaps” approach to prevent a massive rise in evictions during the middle of a pandemic. I agree that the focus of the upcoming act should not be on checks but on sustaining incomes for people such as restaurant workers who will simply not have a job for the foreseeable future.

Sven

Jul 30 2020 at 5:27pm

In europe, there seems to be some relation between amount of fiscal stimulus and GDP loss (at least that is my impression till now given the current data).

Also, it is important to note that the Q2 US GDP loss was smaller than the Q2 loss in germany reported today… And germany is one of the least worse hit countries in europe.

Sven

Jul 30 2020 at 5:32pm

And just in case you are not aware: Fiscal stimulus in US has been much larger than in germany when comparing in a meaningful way (i.e. comparing in relation to GDP size and not include loan to businesses measures, which only partially qualify as fiscal stimulus).

Scott Sumner

Jul 30 2020 at 7:38pm

Interesting. But keep in mind that the German economy is far more export dependent, and hence more cyclical.

TMC

Jul 31 2020 at 3:47pm

The larger Eurozone’s numbers are out at 12% vs Germany’s 10% vs the US’ 9% (all rounded). The stimulus bought something, but likely not a lot of bang for the buck.

Thomas Hutcheson

Jul 31 2020 at 7:22am

What’s to explain? to maintain aggregate demand –NGDP — on track the Fed needed to sharply raise inflation to offset the fall in supply due to workers getting sick or staying home to take care of sick people and children, supply disruptions, and mandatory closing of firms. Instead it let inflation expectations FALL even though they were already below its supposed target.

The especially perverse nature of Fed policy is that TIPS expectations (as of 7/30/2020) are for CPI inflation in years 6-10 of 1.68% pa whereas years 0-5 are LOWER at 1.36% p.a, both far below the equivalent of 2% PCG inflation, ~2.5%. If the Fed were offsetting the supply shock, expectations should be for higher inflation in the short term and target inflation in the longer term. Even if it were taking the supply shock as given and only trying to offset the demand shock, it should be keeping expectations for both shorter and longer run at CPI 2% What kind of policy objectives can explain this puzzling behavior?

I think it is a mistake to think of the recent Congressional action as “stimulus.” It all seems to be just a collection of more or less misguided measures to provide relief to different groups who have lost income. It would have a “stimulatory” effect only if it led the Fed to purchase X trillion more of something that it would, ceteris paribus.

Matthew Opitz

Jul 31 2020 at 8:57am

How exactly would the Federal Reserve have achieved stable 4-5% NGDP growth in Q2 of 2020 with monetary policy alone? Would an NGDP futures market really be enough to help them fine tune “buying the world” just enough to balance out the COVID shock? It seems like kind of a fine needle to try to thread with a great risk of overshooting and ending up with far too much NGDP growth, with the exact amount of NGDP disruption from COVID having been exceedingly difficult to estimate in real time.

And in a situation where real GDP was constrained with physical limitations on production for much of April due to the lockdown, wouldn’t a continuance of 5% annualized NGDP growth have entailed 30+% inflation during Q2? Are you prepared to bite that bullet?

Thomas Hutcheson

Aug 1 2020 at 10:59am

Well, they could create a NGDP futures market, but pending that they could make an estimate of the real shock and then target the TIPS inflation rate at 2.5% + shock%. Of course just letting it be know that they were not going to let the PL fall below 2.5% pa increase since some date, say Jan 1 2019 would help a lot.

Scott Sumner

Aug 1 2020 at 8:39pm

I favor targeting NGDP about 12-months forward, so I would have allowed NGDP to fall sharply in Q2.

Mark Z

Aug 1 2020 at 12:20am

Inasmuch as the reason the $1200 checks failed to stimulate spending (for obvious reasons), and people just saved money, then once they can spend it, they will, and the stimulus will happen. So is there really any problem with doing the stimulus “too early?” Giving someone $1200 in April that they only spend in January has the same effect as giving someone a $1200 check in January that they spend immediately? As long as you give the money out by the time people can spend it, it’ll get spent just the same, right?

Scott Sumner

Aug 1 2020 at 8:43pm

Yes, but you could argue that by waiting we’d have a better idea of how much monetary policy could and world do, and how much fiscal stimulus was actually needed.

Nathan

Aug 1 2020 at 10:21am

Scott, remember your post on “empressions” – employment recessions. You suggested that there is only one kind, the kind associated with falls in nominal gdp. But there is another kind of empression. If you are still interested, read on.

https://seekingalpha.com/article/4361570-skill-stalagmites-technology-stalactites

Hans Viirlaid

Aug 2 2020 at 6:45pm

I am confused.

Sure, the GDP contracted about 8.6% (or 34.3% annual rate) in the second quarter but the contraction was all in the first half of that second quarter.

And the government checks didn’t go out until the end of April.

The GDP stopped contracting about the middle of May.

Is that really a ‘failure’?

To me it looks like the distributed money had the intended effect.

Philippe Bélanger

Aug 3 2020 at 1:04am

Why is monetary stimulus “costless”, whereas fiscal stimulus isn’t? The Fed can, in the future, monetize the debt that was issued to finance the deficit. Yes, this could eventually create inflation, but so would monetary stimulus. So it doesn’t matter, when assessing the cost, if the stimulus is fiscal or monetary; what matters is what the Fed does in the long run.

derek

Aug 3 2020 at 9:34am

I’m not nearly as convinced as you that the $1200 checks did not stimulate spending – just look at the surging home improvement sector (either retail stores or the incredibly tight contractor market). People have money to spend on home improvements and are spending it. The high frequency graphs of consumer spending show a very clear jump in activity when the checks came out. Granted, people who own homes may be more likely to have money even without the stimulus than people who don’t own their homes, so maybe people are just spending money that they cannot spend on travel, dining, daycare, etc., on home improvements and consumer goods. And it goes without saying that the rise in spending may be more due to lockdowns expiring than to any stimulus.

As far as WHY the checks exist, I think they are mostly intended as a spoonful of sugar for any still-employed middle-class who resent the massive income boost for low-wage unemployed people or companies who figured out how to game the unemployment system (furlough one day per week to unlock access to fed benefits and then give employee the equivalent of a $30k annual raise while saving company money). I am not saying that the stimulus was all good policy compared to your preferences, but given the USA’s apparent inability to target unemployment benefits or to design a system that does not introduce huge and obvious work disincentives/inequalities, I am not sure that the needed unemployment benefits were really possible without the stimulus checks.

Comments are closed.