I often warn against countries running up excessively large public debts. Some people interpret my worry as a prediction of a future financial crisis, perhaps including default and/or very high inflation. They point out that countries such as Japan have run large deficits for many decades, with interest rates on long-term bonds remaining near zero. So are these worries overblown?

For developed countries with their own currency my actual fear is not outright default, or even hyperinflation. Rather I fear that an excessively large public debt will eventually force painful changes in fiscal policy, such as benefit cuts or more likely large tax increases. The most efficient fiscal policy is one that smooths tax rates over time, as high taxes are a drag on the economy. Furthermore, the effect of tax increases is not linear. A doubling of the tax rate will lead to a roughly fourfold increase in the deadweight loss, without even doubling tax revenue.

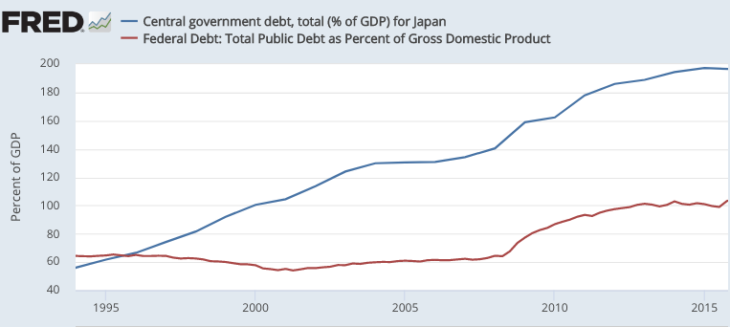

By the mid-1990s, Japan’s budget deficits were on an unsustainable path while the US budget deficits were still on a more sustainable path. At this time, Japan had a 3% national sales tax whereas the US had no national sales tax. Both countries had overall tax burdens that were below average for developed countries.

In 1997, Japan raised its national sales tax to 5%. In 2014 they raised the tax to 8%. In 2019 they raised the tax to 10%. These increases were intended to address the debt problem. Meanwhile the US continued to have no national sales tax. Thus the very thing I was worried about did actually occur in Japan. Furthermore, more tax increases are almost certainly on the way. Unfortunately, the US budget deficit situation also became unsustainable during the late 2010s, due to a highly expansionary fiscal policy. Thus the US is likely to be forced to raise taxes (or cut benefits) in future years.

To summarize, it is true that Japan is likely to be able to avoid default on their public debt. But this does not mean that those who warned the deficits were unsustainable were wrong. Indeed, Japan was forced to repeatedly raise taxes precisely because the path of the public debt was unsustainable without future tax increases.

PS. The FRED data site shows net debt for Japan (blue line) and gross debt for the US (both as shares of GDP.) So the actual gap is even larger than it appears:

READER COMMENTS

David Henderson

Jun 6 2020 at 5:24pm

Actually, not a fourfold increase but a threefold increase.

robc

Jun 6 2020 at 5:55pm

I having flashbacks from the last thread this came up.

🙂

Philo

Jun 6 2020 at 6:32pm

(A quadrupling, that is.)

artifex

Jun 6 2020 at 9:18pm

The Merriam-Webster page for the -fold suffix says “multiplied by (a specified number) : times” and gives “a sixfold increase” as an example. Wiktionary usage note addresses it and says “a twofold increase” means “an increase to 200% of the original amount”.

Let’s abolish ‘fold higher’ and ‘fold increase’ from our lexicon says it’s used inconsistently.

Scott Sumner

Jun 6 2020 at 11:13pm

Good point.

Jason S.

Jun 7 2020 at 7:48am

It’s a little misleading to include only federal debt when comparing the U.S. to other countries, because other countries typically do not have (much) state and local debt. The effective federal tax base is a lot lower than the GDP figure alone would suggest.

Scott Sumner

Jun 7 2020 at 1:03pm

Good point.

D.O.

Jun 9 2020 at 9:37pm

Only a little. Federal debt is about 23 trln. and state and local debt is about 3.5 trln.

Phil H

Jun 7 2020 at 11:07am

This is a really interesting question. The most interesting take on debt that I have heard came from a Chinese economist who described debt as a technology: it is the technological capacity to bring future earnings forward to the present day, in order to smooth out problems like the need for upfront investment.

So the question of what is a sustainable versus unsustainable level of debt is ultimately a technology question: how good are the debtor and the creditor at balancing the debt against other potential uses of their resources?

I like looking at debt this way, as it sidesteps the moral baggage that people love to load onto the notion of debt/credit.

Thomas Hutcheson

Jun 7 2020 at 11:18am

Indeed, another way of saying that expenditures should pass an NPV test (with inputs valued at marginal cost).

Mark Z

Jun 7 2020 at 3:24pm

I think this is basically what the issue of crowding out is: what is the opportunity cost of credit diverted to the federal government. Though one reason why I think the ‘moral baggage’ is largely justified is that much – maybe most – federal spending is not investment but consumption, and on the question of how much we should pull consumption forward from the future, present-day consumers and future-consumers probably have very different perspectives on the matter, but only the former can vote in the present (mostly). Of course if markets are efficient and forward looking then pulling forward future consumption should affect expectations of future GDP growth immediately, and if voters are rational they should take that into account in deciding how much their government should borrow today, but I expect most people regard at least one of those conditions is challengeable if not both.

Phil H

Jun 8 2020 at 8:46pm

I see what you mean, but I think our destruction of the physical environment is a much more serious moral failure to give future generations what they’re due.

Mark Z

Jun 9 2020 at 2:48pm

Why would the remediation of one require the other?

Thomas Hutcheson

Jun 7 2020 at 11:13am

So the only problem with deficits is the timing of the revenue and expenditure adjustments? This seems far too limited. If an expenditures has a negative NPV, then resources are being wasted in every period until it is adjusted. Likewise, if taxes are eventually going to rise (hopefully more on consumption rather than on income), the delay reduces savings and investment in the interim.

Of course a projection of deficits rising to infinity indicates that something is wrong, but “sustainability” is a poor criteria for deficits because the “deficits” is the wrong variable to try to optimize. It seems to me better to optimize the taxes and expenditure year by year instead.

[Sorry to have to keep mentioning this, but the TMI spam filter is still not letting my comments be posted there.]

Scott Sumner

Jun 7 2020 at 1:06pm

I recently released three of your comments from the span filter. They should be there now.

Thomas Hutcheson

Jun 7 2020 at 10:34pm

Thanks!!!!

[Thomas: In the future, if you have a problem on another blog, please do not keep posting comments about your experiences or frustrations here on EconLog. That should go without saying. It is annoying for our other commenters and readership, irrelevant to the main threads under discussion, and distracting for our bloggers. If you have a personal question for one of our bloggers about, say, your comment status on a different blog, please email the blogger privately or email us here at webmaster@econlib.org or econlib@libertyfund.org so we can relay it to the blogger without troubling the entire rest of the EconLog comment community and comment threads. Your repeated complaints in many threads in your comments about this entirely irrelevant matter have, unfortunately, now moved your comments into the spam filter processing on EconLog. So, out of the frying pan, into the fire.–Econlib Ed.]

dlr

Jun 7 2020 at 2:54pm

the fred data does not show net debt for japan, it shows gross debt. net debt can be a bit of a term of art but fred seems to be clearly using world bank gross debt. this link includes some gross/net differentials from a few years ago:

https://www.mof.go.jp/english/budget/budget/fy2017/04.pdf

Scott Sumner

Jun 8 2020 at 4:38pm

Thanks dlr. I had seen estimates of 250% of GDP, and assumed those were the gross debt figures.

Tsergo Ri

Jun 7 2020 at 8:24pm

Would not Japan have avoided raising the sales tax if it had printed more money to pay for the public debt? It’s pretty strange why they do not go for a decade or so of 3-4 percent inflation instead of forever 10% sales tax.

Scott Sumner

Jun 8 2020 at 4:40pm

Printing money would not have been enough, but you are right that they should have printed enough to hit their 2% inflation target.

Comments are closed.