In late July, there were increasingly frantic claims in the media that failure to enact another massive fiscal package would hurt the economy. I’ve pointed out that disposable income growth in 2020 has been astounding, and argued that a lack of fiscal stimulus is not the problem. So what will people say if the economy does not tank in August?

One prediction I can make with near 100% certainty is that a continued recovery in August would not be viewed as evidence against the (old) Keynesian view of fiscal stimulus and in favor on the New Keynesian/monetarist view. The efficacy of fiscal stimulus is now accepted almost as a matter of faith, despite the 2013 debacle. Instead, other explanations will be sought.

Here’s the headline and subhead to a new Bloomberg piece by Conor Sen:

The Stealth Sunbelt Virus Turnaround Will Boost the Economy

Even without a new stimulus package, there are reasons for optimism.

It’s worth noting that those reasons for optimism were typically not cited in late July, before the recent data on falling unemployment claims and rising stock prices. So we need to figure out whether the “reasons for optimism” reflect new economic data, or actual external shocks that would justify an increased level of optimism. I suspect it’s the recent economic data.

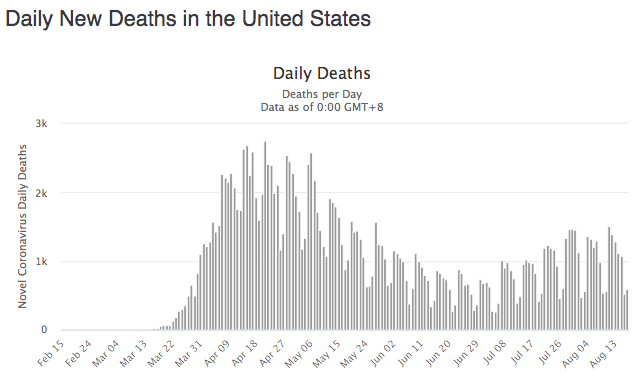

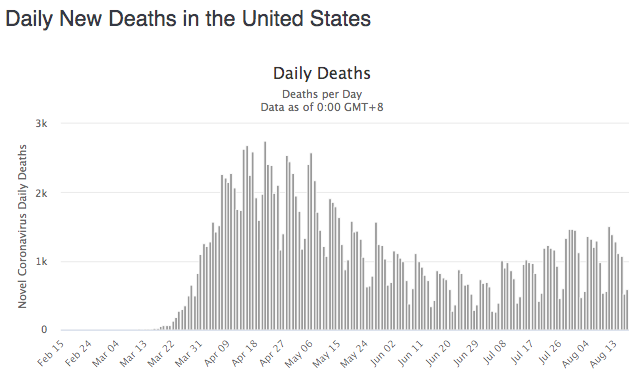

Sen cites the recent Covid-19 data from Arizona, which has indeed improved sharply in recent weeks, after a very bad July. But Arizona is only a tiny fraction of the overall economy. Here is daily Covid-19 fatality data for the US:

Deaths peaked at just over 2000/day in April, fell to just over 500/day in late June, and then doubled again by late July. Ignoring day of the week fluctuations in Covid reporting, the first half of August is still near the July peaks. So one does not see the Arizona improvement in the national fatality data.

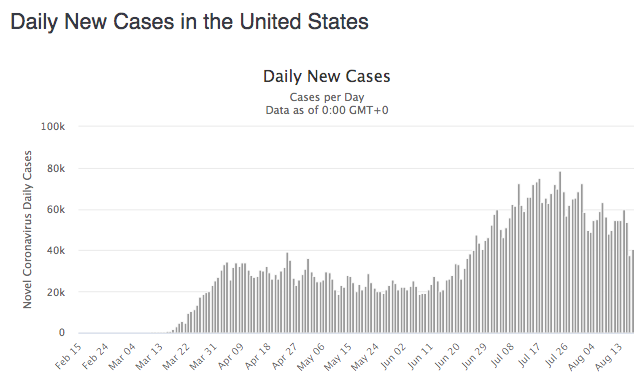

On the other hand, reported new cases are trending downward nationwide, although they are still several times higher than in June. (The recent decline is a bit smaller than it might appear to the naked eye, as the most recent two days are weekend data (reported Sunday and Monday), and today will probably see a jump upward).

This decline may partly reflect reduced testing, but a portion of the decline is almost certainly real. The question is whether that’s enough to explain a modest improvement in the economy in August, despite the end of fiscal stimulus. I doubt whether consumers are that sensitive to a drop in reported cases that is not showing up (yet) in the fatality data, but I can’t rule it out.

Even so, you have to wonder how important fiscal policy actually is if a fairly modest improvement in Covid-19 can explain why dire economic predictions don’t seem to be coming true. If anything, I believe this supports my claim that it’s the virus, not a lack of disposable income, which is driving the economy right now.

PS. I always need to point out that a major increase in the budget deficit was appropriate this year. I am merely questioning stimulus for stimulus sake, such as giving $1200 to middle class people with jobs and giving unemployed people more than they earned on their previous jobs. I favored the provisions that expanded unemployment compensation to a wider range of people during recent months. So I’m not suggesting that doing nothing right now is appropriate; rather this post is aimed at the macroeconomic effects of using fiscal stimulus as a tool to boost disposable income.

Update: This David Beckworth tweet provides additional evidence that a lack of disposable income is not what’s holding back spending.

READER COMMENTS

Variant

Aug 18 2020 at 3:57pm

Most of the KPI’s have significant flaws:

Dashboard deaths mostly come from days past, and the ability to look at actual date of death means waiting 2-3 weeks for processing. The former is sometimes an ok proxy, but subject lately to death certificate matching and other activities that gum things up. And of course died with vs. died of.

Cases, or case positivity more specifically can be affected by who is being tested (in March we only tested sick people, then we went crazy and tested everyone, now that seems to be backing off some — all variances in the test group), lag (Texas, California), inclusion of antibody tests, inclusion of non-electronic tests (positives only with negatives not reported), and significant irregularities in how the data is reported by media outlets

Likely the best indicator is a combination of hospital census and deaths by true date of death. The former are trending in the right direction and the latter is already likely trending down with peaks in late July/early August, though you won’t see the trend for a couple of weeks.

Scott Sumner

Aug 19 2020 at 1:33pm

Thanks for that info. I’d still say the declines are too small to explain recent economic trends. A state by state analysis would probably confirm my view.

Thomas Hutcheson

Aug 18 2020 at 5:59pm

The argument for Congressional action is to provide relief for people who need it, not to provide “economic stimulus. Keeping up aggregate demand is the Fed’s job and even when they are doing it poorly, it’s well beyond the power of Congress to force their hand by incurring deficits not justified by NPV considerations.

How the economy performs in August as it did in July and will in September depends on the Fed.

Scott Sumner

Aug 19 2020 at 1:32pm

You said:

“The argument for Congressional action is to provide relief for people who need it, not to provide “economic stimulus.”

Yes, but that’s obviously not what they did in the earlier rounds of stimulus.

Alan Goldhammer

Aug 18 2020 at 7:18pm

Scott – I think it is important to define the economy. Some parts of it were hardly effected at all, principally big tech which has driven the stock market to highs. You are correct about the virus driving things as opposed to disposable income. This is a point I’ve been making here and other places for several months. For those over 60 who have money to spend, there is no place to spend it. I don’t know about you, but we are not going out to restaurants and there is no performing arts (including movies) going on at all in our area. Performing arts are shut down for the rest of the year and we routinely go out to plays/concerts/dance once a week.

The travel industry is in the can and I don’t see any major meetings being booked right now. Every organization that I belong to is doing meetings on line. Remote work is still the only game in town for many people and they are all scrambling for help with their children. I’m keeping a running total of those in our neighborhood who have posted on our list-serve (600 families) and there have been 30 requests for home help with kids because of closures in day care and our local schools doing only remote teaching. Clearly there is an opportunity here for gap year students to work in this area.

The carnage in local retail and hospitality is very high in a lot of places and those jobs will not mysteriously come back despite what the S&P 500 says. Companies in those areas have lost 30% or more of their value providing they are still solvent. Retail can have an online presence but not all have adapted. Food service is only a limited option on line but doesn’t bring back all the wait staff and others to work.

I still think unemployment hovers at or close to 10%. 1/3 of the public is still to concerned about COVID-19 to change their habits right now. Until that changes, things are not going to get any better.

Ike Coffman

Aug 18 2020 at 9:24pm

Bear with me because I am going to make some assumptions here, and I am not an expert. David Beckworth provides graphical evidence that there is a two tier economic recovery going on right now, and when you talk about the economy not tanking, it is not tanking for those in the higher income groups. For those in the lower income groups, particularly those in the service industries, there is no economic recovery and I think you can say they are still in a recession, if not a depression.

The bad news for the lower income group is that there are (at least) two significant signs of recovery that both economists and politicians can point to, which is the recovery in GDP and the exploding stock market. Both of these indicators are saying we don’t need any more stimulus, ignoring the fact that those in lower income brackets are still hurting badly.

I also want to credit Alan G, I agree with him the lower income group has both had their income reduced and they spend whatever money they get pretty much as soon as they can get it, while the higher income groups have not had their incomes affected much but don’t find much to spend on.

Here is where I am going to attempt to explain what I think, if I am wrong please correct me.

Scott has introduced me to his favorite GDP formula, and after some thought it turns out I like it a lot myself.

GDP = M * V

I believe that the Fed has powerful and effective tools that effect M, but they don’t have much to influence V. Congress, on the other hand, can significantly affect V through stimulus payments and the extra $600 dollar a month unemployment. I don’t see how they have much direct influence on M. So the Fed controls M and congress controls V. I contend that one of the reasons the economy recovered so quickly is because both types of tools were used, and both were effective.

However, congress is deadlocked, those direct cash stimulus programs have ended, and there are no plans on the horizon to break the deadlock. Because the Fed is doing doing their stimulus part while demand remains low I see the stock market continuing its run, which means I do not see the economy tanking. However, the increase in M is not making its way down to the lower income groups, so they will stay in their recession. I don’t know any better way to say it than the lower income group is screwed. The rich get richer, the poor get poorer.

Scott Sumner

Aug 19 2020 at 1:35pm

You said:

“David Beckworth provides graphical evidence that there is a two tier economic recovery going on right now, and when you talk about the economy not tanking, it is not tanking for those in the higher income groups.”

But his data also shows that spending for the rich has declined more than for the poor, which is what’s relevant to this post.

Ike Coffman

Aug 19 2020 at 2:37pm

I thought David Beckworth himself explained it pretty well in his own comments section (“if I had to guess I’d say cash transfers and extra UI covered larger % of lower income budgets and therefore easier for them to resume spending.”) and I didn’t want to just repeat what he said.

Todd Kreider

Aug 19 2020 at 10:26am

I wouldn’t say several times higher than in June.

U.S. Covid-19 cases have been at 44,000 a day over the past four days and will average about that for the week since predictable. In early June, there were 20,000 cases a day, in mid June there were 30,000 cases a day and in late June there were 42,000 cases a day.

Scott Sumner

Aug 19 2020 at 1:42pm

Maybe, but the graph I provided shows well over 50,000/day in the first half of August vs. around 23,000/day in the first half of June. Obviously, any recent employment data cannot be explained by the past three day’s Covid data.

Jose Pablo

Aug 21 2020 at 10:48am

In Florida the situation has improved significantly with new daily cases half the end of July numbers and daily deaths below one third.

https://experience.arcgis.com/experience/96dd742462124fa0b38ddedb9b25e429

In Miami-Dade county the “Covid Patiens Admitted” (one of the most reliable metrics) have gone from 1,785 to 1,136 (a 32% reduction) in the last 14 days, with the “Number of Covid Patients in ICU Beds” going from 463 to 296 (close to a 40% reduction) in the same period of time.

http://www.miamidade.gov/information/library/2020-08-20-new-normal-dashboard.pdf

Michael Pettengill

Aug 19 2020 at 11:46am

Walmart has certainly profited from the pandemic in terms of growth in revenue, market share, and Federal spending to prop up consumer spending even as wage incomes fell significantly.

How will the end of Federal spending to prop up consumer spending and wage income cuts becoming permanent not slow or stop Walmart’s growth?

Comments are closed.