In recent years, the Fed has increasingly adopted the rhetoric of 1960s Keynesianism. Go for growth. Don’t worry about a bit more inflation. Jobs are much more important. Given that 1960s Keynesianism gave us the Great Inflation, should we be worried about today’s rhetoric?

Oddly, at roughly the same time that they adopted all this expansionary rhetoric, the Fed switched to average inflation targeting, which makes 1960s-style expansionary monetary policy totally impossible to implement.

So what will the Fed do in the 2020s? Will inflation average 2%, or will it average 4%, 6%, or 8%? I don’t know, but my hunch is that a portion of this Keynesian rhetoric is just the Fed trying to be PC, trying to keep up with a generally leftward shift in public opinion on stimulus. Another part might be the Fed’s perceived need to create “credibility” for its 2% inflation target, given that inflation ran below 2% over the previous decade, and given that (until recently) market indicators have been skeptical that we’d reach 2% inflation, on average.

One way or another, we’ll soon find out.

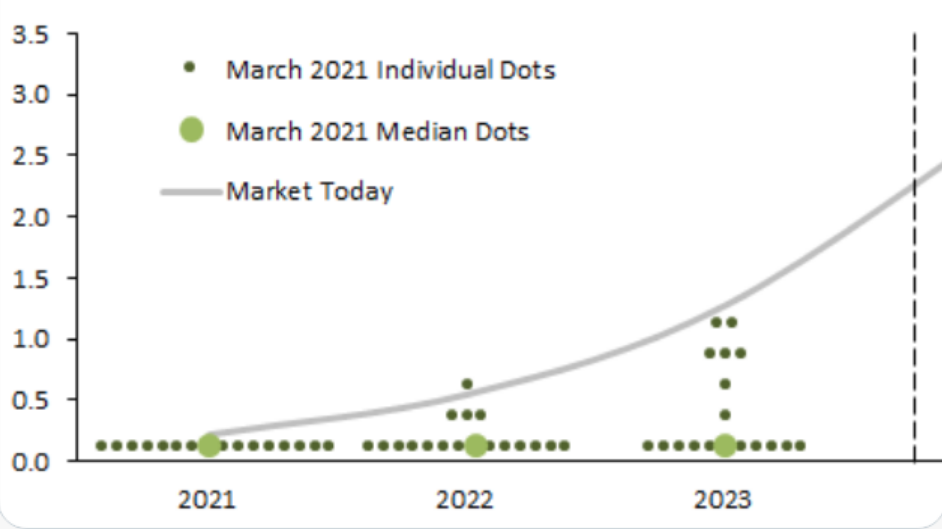

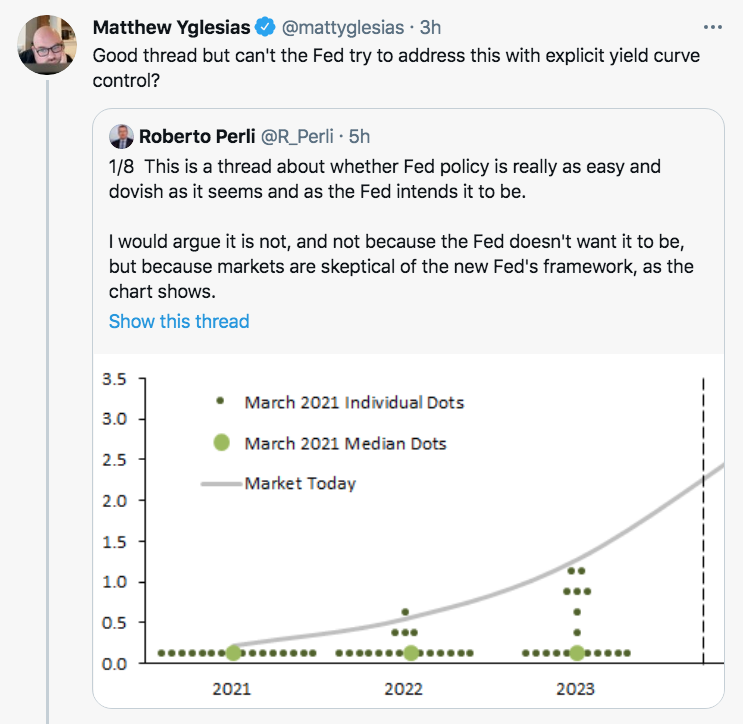

Some people seem concerned by the fact that the markets expect interest rates to rise faster than the Fed itself current predicts.

But this isn’t actually a problem at all, at least if you take the Fed’s 2% average inflation target seriously. At the moment, markets expect a modest overshoot of inflation over the next 5 years, to make up for the undershoot during 2020. Then roughly 2% inflation for as far as the eye can see. But that’s exactly what the Fed says it wants! If the markets think that this good outcome will require higher interest rates than the Fed currently expects, that’s not a lack of policy credibility, it’s just a difference of opinion on the future path of the natural rate of interest. A lack of policy credibility would occur if the markets didn’t expect inflation to average 2% during the 2020s. More likely, rising rates reflect increased confidence that the Fed will achieve its goals.

Don’t confuse the rhetoric with the policy rule. The rule is the actual Fed policy—the rhetoric is just a bunch of pretty words.

PS. Of course the other problem with the tweet that Yglesias links to is that Perli is reasoning from a price change, assuming that rising longer-term yields reflect predictions of a tighter monetary policy stance.

PPS. People often ask me about “yield curve control”. That would be like a ship captain announcing “steering wheel control”, a commitment to hold the ship’s steering wheel at a fixed position for days on end, regardless of changes in wind and currents. What do you think? Does that sound like a good idea?

READER COMMENTS

marcus nunes

Mar 21 2021 at 8:22pm

My worry is that many at the Fed, at least Powell & Brainard still reason based on Phillips Curve ideas. The AIT itself is founded on the NKPC. The assumption is that the Phillips Curve is very flat until a very low level of unemployment and will only rise slowly beyond that point.

In my latest post I argue that what leads to a falling rate of unemployment is monetary policy keeping NGDP growing at a stable rate. The “quality” of the overall labor market (something that the Fed now wants to take into consideration in addition to the headline u3) depends closely on the LEVEL path along which NGDP grows.

https://marcusnunes.substack.com/p/kernels-of-truth

Scott Sumner

Mar 21 2021 at 11:49pm

I agree. They need to focus more on NGDP and less on the unemployment rate.

Thomas Hutcheson

Mar 21 2021 at 11:34pm

Maybe the Fed DOES have in mind both of its Congressionally mandated goals the inflation target is the price stability hold but it also sees an obligation to maximize employment, but (presumably) thinks that average 2% PCE will maximize employment.

Rajat

Mar 22 2021 at 6:50am

A few random comments:

I don’t follow the Fed closely enough to know about its current rhetoric, but the dot point projections seem to me to be pure signalling – as they were during the last decade. The dots offer no commitment; they only indicate intent, or ‘mood affiliation’ if you like (as in, a strong desire given past errors to refute any prospect of rises in the Fed Funds rate regardless of inflation expectations). In the last decade, the Fed was concerned that people might think it would stay low too long, giving rise to inflation or ‘distortions’ or whatever. Now the Fed is concerned that people think it will raise too quickly, hence it is trying to signal the opposite – “look, market, we really mean it”. Pure ‘cheap talk’.

Yglesias’s tweet indicates that he, too, reasons from a price to a stance – low rates equals easy money. I notice this framing even from those familiar with your work who should know better.

I agree and have always agreed with your PPS on YCC, but how is the 2010s’ ‘forward guidance’ any better (or YCC any worse)? Once one adopts the NK framework, YCC sounds like a great idea because it appears to represent a stronger commitment to low rates than forward guidance and – if applied for a short enough future period – may avoid the need to make as large asset purchases as a ‘do whatever it takes’ QE policy may require (at least initially).

Scott Sumner

Mar 22 2021 at 10:55am

I agree. And the problem here is that adopting the NK framework tends to lead people in the wrong direction.

bill

Mar 22 2021 at 8:09am

The dots are a distraction.

Scott Sumner

Mar 22 2021 at 10:55am

Yes.

eg

Mar 22 2021 at 4:49pm

Maybe the Fed is signalling that they’re basically getting out of the way and will allow Fiscal Policy to do the heavy lifting.

robc

Mar 23 2021 at 6:59am

I was about to ask a question and decided to google it myself…and now I am totally confused (actually, not surprised at all, and yet still confused).

I was wondering how much of the CPI basket was housing costs. It turns out none at all. No wonder the official inflation numbers have seemed like complete BS for the last few decades (if not forever).

I would accept it if they split out land from housing. If they want to treat the land as an investment asset and count the building as a consumable (which it is), then okay. And since the land is where most of the increase has occurred, maybe it isn’t totally off. But housing costs should be a significant percentage of the basket still.

robc

Mar 23 2021 at 7:04am

Reading deeper into the government description, “shelter” is included. So, the house is partially included. They are still considering the house as an investment asset, not a slowly decaying consumable, but at least part of the value is included. It is still under accounted for.

Scott Sumner

Mar 23 2021 at 10:18am

Housing is nearly 30% of the CPI.

David Seltzer

Mar 23 2021 at 6:54pm

Scott said, “People often ask me about “yield curve control”. That would be like a ship captain announcing “steering wheel control”, a commitment to hold the ship’s steering wheel at a fixed position for days on end, regardless of changes in wind and currents. What do you think? Does that sound like a good idea?” I suspect it’s not a good idea. The Fed’s hinting at operation twist; sell the two year treasury and buy the 10 year with the proceeds to control target inflation is similar to the ship’s intrepid captain. What happens when the Fed wants to unwind the trade, “Operation Untwist?” But in this climate of r < G, MMT who knows?

Comments are closed.