Irving Fisher proposed a price level target in the early 1900s, and numerous other reformers had already been advocating the policy over the previous 100 years. Sweden dabbled with the idea in the 1930s, but it wasn’t until the 1980s that inflation targeting caught on with central bankers.

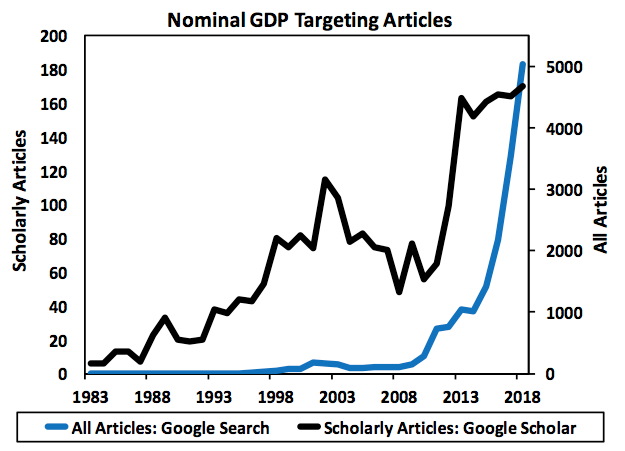

Nominal GDP targeting is another idea that’s been discussed over a long period of time, going back at least to the interwar period. It wasn’t until 2010, however, that the idea achieved broad mainstream recognition. David Beckworth put together an interesting graph showing the number of times that nominal GDP targeting is mentioned in the popular press (blue line) and also in scholarly articles (black line):

Notice that the uptick in the number of popular article mentions began about 2010, and a surge in scholarly articles began two years later. (Note that different scales are used, so there are actually more mentions in the popular press.)

Policymakers have not yet accepted NGDP targeting, which partly reflects the conservative nature of central banking. Nonetheless, NGDP targeting has achieved an important milestone. Support for this policy has risen to the point where if this regime were already in place, central bankers would not be recommending that it be replaced with inflation targeting. And if we were starting from square one, with no regime in place, NGDP targeting would be at least as plausible a candidate as inflation targeting. The persistence of inflation targeting reflects the perceived costs of shifting to a new monetary regime.

PS. This Ross Douthat column caught my eye:

At the same time, though, he has relied on personnel who are associated with 2010-era G.O.P. orthodoxy, rather than elevating the kind of conservatives who have actively theorized for a more populist right. Trump’s choice of Steve Moore to the Federal Reserve is a recent case study: Instead of elevating a principled inflation dove (National Review editor and Bloomberg columnist Ramesh Ponnuru would have been my outside-the-box choice), Trump picked a hack who was obsessed with imaginary inflation under Obama, and only flipped to back a looser monetary policy because, well, it was the Trumpy thing to do.

This has to be a first, a NYT essay that advocates putting a market monetarist on the Fed. (I hope Ramesh doesn’t mind me calling him that—his views are so close to David Beckworth’s and mine that I believe the label fits. Indeed he’s coauthored with David on several occasions.)

PPS. Otherwise, I have a lot of reservations with Douthat’s piece, which has a sort of “let Trump be Trump” feel. Douthat has decided that among all the contradictory things Trump promised during the campaign, including paying off the national debt, the populist conservative stuff was the real Trump. Maybe so, but in office he’s deregulated big banks and cut corporate tax rates. Although Douthat is right that Trump has refrained from cutting popular entitlements, he has not built infrastructure, cut illegal immigration, reduced the trade deficit, or any of the other populist items on his agenda. Indeed he hasn’t even taken any meaningful steps to do any of those things. I’m not sure whether looking for the “real Trump” is a useful endeavor. Is he a hawk (Iran) or a dove (North Korea)?

READER COMMENTS

Michael Sandifer

Mar 31 2019 at 8:04pm

Ponnuru is actually a thoughtful, intelligent person. Another one on the right, if that even makes sense anymore, is James Pethokoukis. Matt Yglesias or Ezra Klien might be his equivalent on the left.

Michael Sandifer

Mar 31 2019 at 8:08pm

How great would the country be, by the way, if the debates were between conservatives and liberals like them?

Mark Z

Mar 31 2019 at 9:45pm

Mildly tangential question: what is the consensus among market monetarists on the optimal value for an NGDP target? Why not 0% NGDP growth?

Matthias Görgens

Mar 31 2019 at 10:13pm

George Selgin has come out in favour of a stable nominal GDP (ie 0% growth) in his recently republished Less Than Zero. Scott Sumner wrote a foreword for the new release.

The title refers to Less Than Zero [inflation] that you’d get if you pair a stable nominal GDP with secularly rising real GDP.

The book is available for free online.

Scott Sumner prefers something around 4%, mostly that’s because it’s the historic average for the US I think. But one percent more or less doesn’t seem to make too much of a difference, as long as the target is announced well enough in advance.

Eg level targeting (vs growth rate targeting) is more important than 3% vs 5% target.

Mark Z

Apr 1 2019 at 12:51am

Selgin’s Less Than Zero was actually precisely the book that really convinced me of the merits of a productivity norm/NGDP targeting. His primer on monetary policy is also great. I just wasn’t sure what the basis was for Scott’s preference for 4%.

Trevor Adcock

Apr 1 2019 at 3:56am

There is some evidence of long run non-neutrality at mild levels of NGDP growth vs no NGDP growth. Bryan Caplan, David Hume, and others have argued this. Also increased variance in GDP seems to decrease long run GDP growth, at least, mildly.

Mark Z

Apr 2 2019 at 9:23am

Thanks for the reply. Would an implication of this be that, as real GDP growth rate declines (assuming it does), we should gradually or periodically adjust the NGDP target downward?

Scott Sumner

Apr 1 2019 at 11:45am

I believe George Selgin favors something closer to zero percent growth per capita, or per worker, not zero percent overall.

A 4% growth rate reduces the zero bound issue and makes labor markets more flexible (maybe.) A higher number raises the tax rate on capital income. So there are tradeoffs.

Mark Z

Apr 2 2019 at 9:29am

Isn’t level targeting itself supposed to resolve (or at least mitigate) the problem of the zero lower bound?

Scott Sumner

Apr 2 2019 at 12:10pm

Yes.

Benjamin Cole

Mar 31 2019 at 11:57pm

As a practical matter, I favor “3+3” or nominal GDP LT at 6% every year. I think this level brings moderate inflation and solid growth, and was the average from 1982 to 2008.

The US labor force appears to be expanding with tighter labor markets and very modest real wage growth. We could have a long good run at 6% NGDPLT.

I prefer prosperity and moderate inflation to slow growth-low inflation. I think you get “2+2” at 4% NGDPLT, and maybe edge towards recession.

There is another even bigger and uglier snarl: How to get to 4%-6% NGDPLT?

We hit lower bound, and if QE doesn’t work, then what?

Scott Sumner advocates negative interest rates and more QE, the Japan model. So far, very limited results in Japan. Maybe we have to wipe out cash to make negative interest rates work. We may end up wiping out our banks too, btw.

Just try harder? Maybe. Sumner says so.

Larry Summers says bigger federal budgets are the answer, but not MMT. Okay, not too hot, not too cold. This has the feel of playing for a tie in the NFL.

I say money-financed fiscal programs are inevitable. Ben Bernanke advocated same for Japan in 2003. Adair Turner has written persuasively on this topic.

As a practical matter, maybe QE+federal deficits=money-financed fiscal programs. There seems to be a variety of opinions on this, from experts. The Temple of Macroeconomics has many a smoky circular room, with mirrors, surrounding hallowed and hoary totems towering in the haze.

Genuflect accordingly, to your tastes.

I say, “Send in the choppers. Fleets of ’em.”

Thaomas

Apr 1 2019 at 8:33am

Maybe I’m just being conservative, but I’d rather see the Fed do price level targeting as the “price” half of it’s dual mandate. The only disadvantage I se would be that it could not use as a single instrument buying and selling NGDP futures. Is there some other disadvantage?

Mark Z

Apr 2 2019 at 9:35am

I’m just going to try to parrot George Selgin here, but stabilizing price level suppresses salutary price changes, such as those caused by changes in productivity, and we only want to counteract overall price changes due to changes in demand for money balances. This, at least as I understand it, is the main issue with price level targeting.

Thaomas

Apr 5 2019 at 4:18pm

I was not advocating a target of a 0% pa increase in the price level. Given (?) the Fed’s reluctance to go below 0% nominal interest rate, it’s probably better to be on a 3% pa price level target than a 2% trajectory. What the optimal rate of increase in the price level is depends on how downwardly sticky nominal prices are and how much relative prices need to change typically.

George Selgin

Apr 3 2019 at 9:13am

Thanks to Scott and others for the references to Less Than Zero. Pleae note that only the original 1997 IEA edition is available online. The much prettier Cato ed., with Scott’s foreword as well as a new preface by me, is available only through Amazon, at https://www.amazon.com/Less-Than-Zero-Falling-Growing/dp/1948647109

Lorenzo from Oz

Apr 5 2019 at 9:33pm

Good news on the increasing scholarly interest.

Comments are closed.