The Fed has a legal mandate for price stability and high employment. Their mandate does not instruct them to stop trying if things get a bit difficult. It does not instruct them to pass the job on to the fiscal authorities. And yet that’s exactly what we are seeing. Here’s Greg Ip:

Research by John Williams, president of the Federal Reserve Bank of San Francisco, and Fed economist Thomas Laubach suggests the equilibrium rate could be as low as 2%, or zero when adjusted for inflation. This means the Fed may have only two percentage points of interest-rate cuts available to fight the next recession (compared with 5.25 points in 2007).

“I am worried that a very low equilibrium rate makes it harder for monetary policy to do the full job of counter-cyclical stabilization policy in downturns,” Mr. Williams said in an interview. That, he said, means fiscal policy will need to play a bigger role.

This is discouraging for many reasons. As recently as 2007, belief in liquidity traps was the sign of economist not being well informed about monetary theory. Leading macroconomists were dismissive of the idea that Japan was stuck in a liquidity trap, and blamed passive policymakers for the deflation. (Since 2013, Japan has averaged about 2% inflation, coincidently this began at the moment they adopted a 2% inflation target. So we now know that this 2007 skepticism was justified.)

But now we find Fed officials starting to claim monetary policy is ineffective at the zero bound, and needs to be augmented with fiscal stimulus. Keep in mind that:

1. Fed officials are not elected

2. Fiscal policy has enormous implications for the Federal budget.

If John Williams is correct, then the Fed plans to hold a gun to the head of Congress next time the US falls into recession. Williams is saying that the Fed will refuse to take any of the many possible steps that are well understood to solve the zero bound issue (such as level targeting) and instead plans to threaten Congress with a recession if they don’t step up and implement fiscal stimulus, which will once again cause the national debt to balloon upwards (as it did during 2008-12.)

I don’t expect anyone in the GOP to complain about this, as they seem to lack an even rudimentary knowledge of monetary economics. But they ought to be especially outraged, as they opposed the previous fiscal stimulus. On the other hand, it wouldn’t surprise me if most Republican officials also opposed monetary stimulus, and preferred a deep recession (except in the very unlikely event that they occupy the White House.)

But the Dems should also be outraged by this comment, as it makes another recession more likely, and since they occupy the White House (and are likely to continue doing so) they will be blamed for the next recession. That’s not fair, but it’s how politics works. And of course the GOP will still control the House, making it very unlikely that there will be another round of fiscal stimulus the next time we fall into recession.

I suppose we should not be surprised that the Fed has not learned much from its recent failures; the economics profession is equally behind the curve. I’ve consistently argued that the Fed follows the zeitgeist—to change the Fed we first need to educate the economics profession.

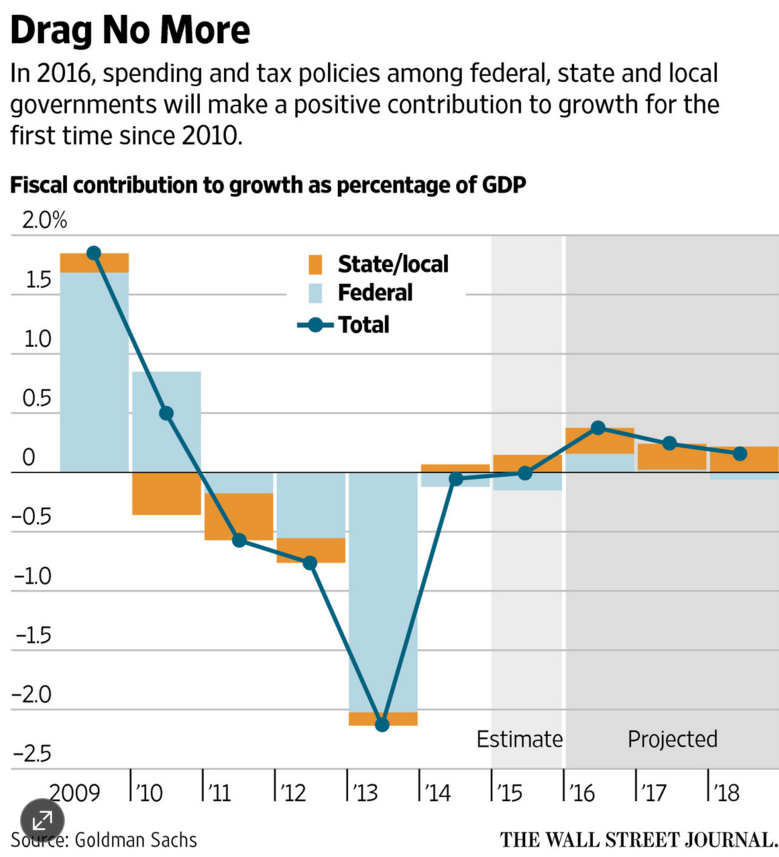

By the way, Greg Ip’s article has a nice graph showing the extent of fiscal stimulus or austerity, in terms of changes in the budget deficit. Of course 2013 was the year of Krugman’s famous “test” of market monetarism, which we passed with flying colors. Keynesians later explained away the acceleration of growth in 2013 by denying that there had been austerity in 2013. I’m glad to see that Ip does not agree with them.

I’m not sure what’s more depressing, their failure to admit they were wrong, or the fact that they now admit that while fiscal policy is their preferred policy tool, they do not even know how to ascertain the stance of fiscal policy in real time, and must wait for the results to come in before figuring out whether it was expansionary or not. (The same thing occurred in Britain.)

HT: Marcus Nunes

READER COMMENTS

o. nate

Jan 8 2016 at 2:06pm

I think you’re right to point out that there is disagreement even among avowed supporters of fiscal stimulus about how exactly the degree of stimulus should be measured. We saw this in the recent back and forth between Tim Taylor, Krugman, and Stephen Williamson. Taylor pointed to federal deficits in ’09 and ’10 to say the stimulus had been large, while Krugman pointed to government employment and Williamson pointed to spending to say it had been small. I wish Krugman would explain exactly what he thinks the right measure is and why, but he seems to beat around the bush.

Aaron S.

Jan 8 2016 at 2:37pm

Doesn’t this inadvertently make the case for electing a Republican in 2016? If the GOP controlled congress and the White House they could do stimulus through tax cuts. Even if they don’t quite know what they’re doing Republicans won’t pass up a chance to cut taxes.

ThaomasH

Jan 8 2016 at 5:05pm

Here is the same sentiment from our old friend Krugman (specifically about the possibility of a China-genic world recession, but the same for any recession):

Of course Krugman has it exactly backwards: with inflation below target, the Fed has even more room to fight an “economic downdraft” if it did not take the inflation rate target as an inflation rate ceiling. I suppose (I try to be charitable) that Krugman means that the Fed would have limited ability to do anything without going back to QE which is politically unpopular with “Macro Media” in the same way that ECB is presumably not doing more because of political constraints.

Brian Donohue

Jan 8 2016 at 5:16pm

Great post, Scott. 2013 is a perfect smoking gun that should be flogged without mercy.

maynardGkeynes

Jan 8 2016 at 5:36pm

Not that he is the voice of god on this blog, but I think Larry Summers, to whom more than a few powerful Democrats listen, seems to be in the Ip camp. I don’t see this view of fiscal policy changing Dem or Republican in the WH. Plan B?

Scott Sumner

Jan 8 2016 at 5:39pm

O. nate, Taylor is clearly right and Krugman and Williamson are wrong. I don’t even see how it’s debatable. Now if Krugman and Williamson want to create brand new theories of fiscal policy, they are free to do so, but they shouldn’t suggest that this is Keynesian economics.

Aaron, You said:

“Doesn’t this inadvertently make the case for electing a Republican in 2016?”

Maybe if I believed in fiscal policy. But since I do not, then no, it doesn’t suggest a reason to elect Republicans.

Thomas, Good point.

Thanks Brian.

ThaomasH

Jan 8 2016 at 5:58pm

One interpretation of Fed action is that they know any kind of stimulus, fiscal or monetary is deeply unpopular (an understatement) with the financial elite and “Macro Media.” Naturally the Fed wants someone else to get in hot water.

Steve J

Jan 8 2016 at 6:48pm

Is Krugman that hard to understand? Calling any deficit “fiscal stimulus” is a simple way of defining it but do we think maintaining constant government spending is boosting the economy? The government could cut spending significantly and still be running a deficit. Krugman does shift the goalposts (especially regarding 2013) but from my perspective it is clear he is trying to find a better measure of stimulus than looking at just what the deficit provides.

Scott Sumner

Jan 8 2016 at 9:53pm

Steve, Keynesians generally prefer the cyclically adjusted deficit. But Krugman seems to ignore taxes entirely.

ThomasH

Jan 10 2016 at 9:54am

@Steve J

Unfortunately, the “proper” measure of “stimulus”/”austerity” would be quite unobservable: departures up and down from expenditures with current costs and future benefits whose NPV are positive. [I think there is a counterpart of this rule for taxation, but it’s harder to state.] A recession lowers the marginal costs of many inputs into government expenditures and lowers the borrowing rate used to discount future benefits. A government that does not increase expenditures in the new positive-NPV projects is engaged in “austerity.” Conversely, making expenditures with negative NPVs is “stimulus.”

It’s clear that the US and European governments have been engaged in massive “austerity” since 2007 and it looks like China was engaged in “stimulus” but the magnitudes are not easily quantifiable.

This is parallel to Scott’s criticism of the Fed when it does not buy assets when the NGDP is below the pre crisis trend as “tight” money.

Comments are closed.