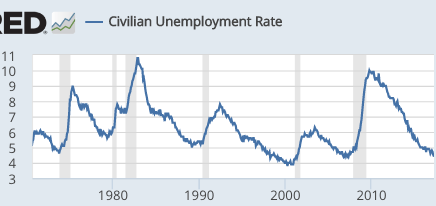

The government reported today that the unemployment rate has fallen to 4.4%. To give you an idea of how low that is, consider that since 1971 the only period of lower unemployment was the tech boom of the late 1990s:

That’s right, the current unemployment rate is well below the lowest rate of the 1980s boom, and equal to the lowest rate achieved during the 2007 housing boom.

The Fed aims for an unemployment rate that is roughly equal to the natural rate of unemployment. The problem with this policy is that the Fed doesn’t have any way to precisely determine the natural rate.

A few years ago, the Fed estimated the natural rate of unemployment to be over 5%. Since that time, the actual rate has fallen to 4.4%. You might assume that the Fed would respond to that by tightening monetary policy with the intention of raising the unemployment rate back up over 5%. In fact, the Fed has not adopted that sort of unemployment target; instead, they’ve steadily reduced their estimate of the natural rate of unemployment, as the actual rate has fallen below their previous estimates.

The Fed’s response to the unexpectedly sharp fall in unemployment is not quite as capricious as it might seem. They’ve looked at other data, and concluded that either they were wrong in the past, or that the natural rate may have fallen in recent years (or both). For instance, inflation, inflation forecasts (TIPS spreads), NGDP growth and nominal wage growth all seem quite subdued, consistent with an economy that is not overheating. (BTW, I prefer NGDP growth and wage growth over inflation, as an indicator of the condition of the economy.)

But if the Fed looked at these other indicators and concluded (correctly in my view) that they had overestimated the natural rate in the recent past, then that suggests those other variables may be better indicators of macroeconomic stability than unemployment itself. Instead of targeting unemployment (or the output gap) and then ignoring what it tells you when the NGDP growth rate conflicts with it, why not just target NGDP growth?

Note that this does not require abandoning the “dual mandate”. The Fed might reasonably conclude that the best way to achieve stable prices and high employment is via NGDP targeting. That’s certainly my view, and it’s what I’d tell them if Congress asked me how their dual mandate could be most effectively achieved.

PS. Last year, commentators pointed to the elevated level of U-6 unemployment, which includes discouraged workers and part-timers that prefer full time work. Since then, however, the U-6 rate has fallen sharply, from 9.7% last September to 8.6% this April. So even the U-6 unemployment rate is now pretty close to normal.

PPS. I predict that RGDP growth, NGDP growth, and payroll employment growth will all slow sharply in 2018. A few years from now, the 2% RGDP growth achieved under President Obama will be seen as unusually high. (Actually, 1.9998%) That’s because even that mediocre growth rate occurred during a period when the unemployment rate was falling sharply, a process that will likely end within a year.

READER COMMENTS

Peter Hurley

May 5 2017 at 1:45pm

I think you undermine your credibility by citing an NGDP growth number with that many significant figures. I don’t think we could ever know with precision whether there was 0.0002% error in the nominal GDP growth rate.

AntiSchiff

May 5 2017 at 4:04pm

Dr. Sumner,

Could low productivity growth mean the unemployment rate is lower than it otherwise would be?

Mr. Econotarian

May 5 2017 at 6:13pm

It doesn’t matter, the Fed doesn’t have a choice.

In 1977, Congress amended the Federal Reserve Act, directing the Board of Governors of the Federal Reserve System and the Federal Open Market Committee to “maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.”

The law states that they must take “account of past and prospective developments in production, employment, and prices.”

https://www.gpo.gov/fdsys/pkg/STATUTE-91/pdf/STATUTE-91-Pg1387.pdf

E. Harding

May 5 2017 at 8:12pm

I agree with Sumner; the U.S. is close to the natural rate. There’s some labor market slack out there, but no more than half a percentage point’s worth of the labor force. Trump will not be the greatest jobs president in history.

Scott Sumner

May 5 2017 at 9:51pm

Peter, I was just amused by how close the number was to 2%, but that’s just me. I realize there is measurement error.

I could say that your credibility was hurt by confusing NGDP and RGDP, but I won’t.

Antischiff, I suppose that’s possible; it depends what counterfactual you assume for monetary policy if productivity had been higher.

Mr, Econotarian. No, they do have a choice. It is true that employment must be a goal of policy, but it need not be a target. It’s easier to stabilize employment by targeting NGDP than by targeting employment.

Morgan

May 5 2017 at 10:13pm

By my estimate, we’re well down the slope of a demographic dip in the rate of growth of the (native born, at least) working age population. I wonder if this is influencing the natural rate of unemployment.

Thomas Hutcheson

May 6 2017 at 7:56am

There is an alternative: use unemployment (some vector or indicators not just U3) to target the “unemployment” portion of the Fed’s mandate and the Price level to target the “price stability” portion.

Under this approach the Fed would goose inflation (with interest rate changes, QE in LT government backed securities, private securities, exchange rate intervention, whatever instrument it chooses) as long as their forecast for the price level remains below target.

The Fed would try to rein in inflation (again, with whatever instruments) when the price level was above target unless the unemployment vector was also above target. What ought to go into the unemployment vector, how to make the price level forecast, and which instruments to use, what level of unemployment to target and what rate of change of the price level to set as the target would remain matters of “Fischerian” discretion.

I’d guess that when both the price level and the unemployment were on target it would appear that the Fed was successfully targeting NGDP. But the behavior of the Fed “out of equilibrium” could be different.

Of course the key to this or the NGDP approach is can the Fed achieve the political independence to commit to allowing inflation to exceed its de facto ceiling.

Scott Sumner

May 6 2017 at 10:11am

Thomas, That sort of asymmetric policy is destabilizing. Your two policies need to be mirror images of each other.

If you don’t rein in inflation when unemployment is high, then you don’t rein in disinflation when unemployment is low.

Max

May 6 2017 at 1:27pm

I don’t think unemployment to be a good judge of effective fed policy. The refining question would be what is the situation of those that are employed and what is the distribution of those? Part time, self-employed vs. Full-time employment and their incomes.

It’s sad that all commentators especially in academic circles seem to ignore those questions.

Ed Fuller

May 6 2017 at 2:44pm

May I suggest that technology is providing a measurable liquidity benefit to the labor market such that the historical effects of tight labor markets won’t be felt till a much lower unemployment rate?

A corollary is the housing market were days on market have dropped dramatically without producing insane price inflation. Technology has dramatically altered the housing market place where new listings are known almost instantly by the entire world.

TravisV

May 6 2017 at 3:09pm

Graphs:

https://fred.stlouisfed.org/graph/fredgraph.png?g=dCVJ

https://fred.stlouisfed.org/graph/fredgraph.png?g=dCVI

It seems to me that money still matters……

Ray D

May 7 2017 at 12:18pm

Labor force participation rate is still quite low and has been since Obama took office.

A bit of this is due to workforce aging, but much of it comes from other factors.

The unemployment rate can’t be discussed independent of the participation rate.

Comments are closed.