With Javier Milei’s recent election victory, there is speculation that Argentina might drop the peso and dollarize its economy. I won’t speculate on how likely that is to occur, as I don’t know much about the political situation in Argentina. But I do have a few comments on the economics of dollarization:

1. Dollarization would solve the problem of hyperinflation.

2. If Argentina intends to dollarize, now would be a good time to do so.

3. Dollarization is not a panacea. Argentina still needs Chilean-style economic reforms, and there’s no guarantee that dollarization would lead to those reforms.

4. Dollarization is less risky than a currency board, but not completely free of risk.

There are two reasons why this is an ideal time for dollarization. First, years of hyperinflation have produced a very small monetary base (in real terms, obviously.) Many Argentine citizens have already switched their money holdings from pesos to dollars. Thus the fiscal cost of dollarization would be relatively low. Given Argentina’s severe economic problems, it would still be a heavy lift, but it’s doable if they are determined to make the switch. Fiscal reforms would obviously make the job much easier, and Milei has promised to slash the budget. I certainly don’t think he’ll cut anywhere near as much as promised, but some cuts seem likely.

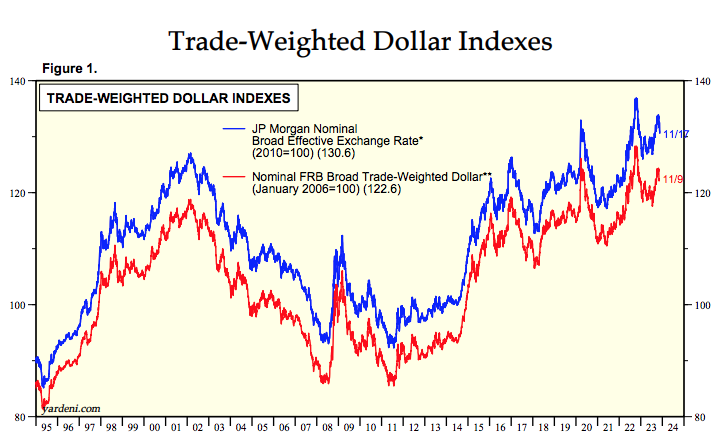

The second factor is more important, and often overlooked. The US dollar is currently quite strong. Thus Argentina would be adopting the dollar at a point in time where large (US dollar) currency depreciation seems more likely than large currency appreciation. Purchasing power parity (PPP) is far from perfect, but it does exert some pressure on currencies in the very long run. Yardeni Research provides the following graph:

It might seem odd that I view a strong dollar as a propitious time to dollarize, as it makes it more likely that Argentina’s inflation rate over the next few decades will slightly exceed the US level. If the dollar were currently weak, then Argentina might be expected to experience slightly lower inflation than the US (as the dollar strengthened.) In fact, Argentina has far more to fear from a few years of negative 1% inflation than from a few years of 5% inflation. Indeed, given their current triple-digit inflation rate, even a 5% inflation rate would seem like price stability to the Argentine public.

This is not just a theoretical point. Argentina did experience a period of mild deflation (and more importantly falling NGDP) during the late 1990s and early 2000s, under their currency board regime. And the primary cause of that deflation was the rapidly strengthening US dollar. Argentina had the misfortune to adopt a dollar peg in 1991, a point in time when the dollar was relatively weak. As it strengthened dramatically in the late 1990s, many developing countries in East Asia sharply devalued their currencies. Soon afterward, Brazil and Russia followed suit. Argentina’s currency became dramatically overvalued. The US tech boom allowed us to get by with a strong dollar. But Argentina was a commodity exporter competing with places like Brazil and Russia.

To be clear, the fact that the US dollar is currently quite strong doesn’t mean that it cannot strengthen even further. But on balance, I consider a significant depreciation to be more likely than significant further appreciation (for PPP reasons.) That should help Argentina to avoid the sort of deflation produced by falling NGDP.

PS. In recent years, I’ve lost all faith in politics. Thus I have no expectation that Milei will be able to achieve any significant improvements in Argentina’s economy. He seems a bit unstable. I will say, however, that my favorite Milei proposal is a market for organ transplants. Such a market in the US could save 40,000 lives/year. Iran is the only country I am aware of that currently has such a market.

READER COMMENTS

Rafael

Nov 20 2023 at 4:01pm

I wonder if Milei will sort of take the Venezuelan approach to dollarization.

More of an implicit dollarization remove all capital controls and just allow both currencies to circulate. Eventually the private sector will just use dollars for everything (or at least set prices in dollar and simply charge the current XR for purchases in pesos) while keeping public sector wages paid in pesos (that get continually devalued).

Eventually you don’t have to fire public sector employees but they leave voluntarily as Peso wages become a fraction of what dollar wages are paying in the private sector.

Brett

Nov 20 2023 at 5:29pm

I think he’ll have to do that stealth approach – he only has the Presidency, not party control of the Argentinian legislature as well.

Eliminate all controls on the exchange and use of dollars, order a cessation in the issuing of new pesos, and any old pesos used to pay taxes or bank deposits get removed from circulation. Have existing pesos still be legal tender as long as they’re out there.

Matthias

Nov 20 2023 at 6:11pm

Why would you remove old pesos from circulation, if you want to get rid of that currency?

That would be an expensive way to stabilise the value of the old peso, only to then abandon them?

And it would cost more political capital than just leaving the old peso machinery in place.

robc

Nov 20 2023 at 5:09pm

I think he would more likely go the Ecuador approach and just flat out switch to the dollar.

Matthias

Nov 20 2023 at 6:17pm

I hope they would allow privately owned companies to issue USD denominated bank notes.

That would help stabilise nominal GDP and make dollarisation cheaper for the Argentinian economy.

Scott Sumner

Nov 21 2023 at 12:39pm

I have no problem with that, but I’m not sure it would stabilize NGDP.

Louis Woodhill

Nov 22 2023 at 11:06pm

At the black market exchange rate (1040 pesos/USD), Argentina could buy up the entire peso monetary base for about $5.5 billion. In contrast, I read that Argentines are holding $265 billion worth of USD in various forms.

John S

Nov 21 2023 at 8:28am

Given all the wild and improbable things that have happened this century, what do you think of the idea that we’re living in a simulation?

robc

Nov 21 2023 at 9:55am

Does wild and improbably things make it more or less likely we are in a simulation?

If more, are you saying someone is cooking the simulation books? Or is there a poor implementation of a random number generator installed?

John S

Nov 21 2023 at 11:07am

Haha, it’s mostly a joke. (mostly…)But the trajectory has unfolded so differently from what I expected in the 90s that it does feel at times like an HBO showrunner is throwing in some crazy curveballs just to screw with audience expectations. Maybe it’s all a big Truman show.

Scott Sumner

Nov 21 2023 at 12:37pm

It suggests to me that much of the way things play out is almost completely unpredictable. No one in 1900 could have foreseen the next 50 years–so it’s nothing new.

Todd Ramsey

Nov 21 2023 at 9:30am

If Greece uses the same currency as Germany, and over time Greece’s labor rules and regulatory policies result in a lowering in the ratio of (Greece’s output per worker) / (Germany’s output per worker), do wages in Greece need to fall to maintain the balance of trade between Greece and Germany?

Would that analysis apply to the United States and a dollarized Argentina?

Scott Sumner

Nov 21 2023 at 12:38pm

Wages would be lower in Greece (and Argentina), but for reasons unrelated to the currency. That would also be true if they kept their own currency.

Todd Ramsey

Nov 21 2023 at 4:46pm

If Greece had its own currency, could wages fall relative to German wages through a change in the exchange rate, without any change in “Drachma” wages?

But if Greece uses the Euro, Greek Euro wages would either have to fall (or German wages rise) in Euro terms to maintain the balance of trade. If the former, since wages are sticky downward, wouldn’t that result in increased Greek unemployment?

That could be avoided through flexible exchange rates?

Scott Sumner

Nov 24 2023 at 12:22pm

Yes, that’s accurate.

Garrett

Nov 28 2023 at 10:14am

The anti-euro argument in a nutshell

C Riboldi

Nov 21 2023 at 10:48pm

What people don’t understand is that Argentina has already been dollarized. Every argentine is hyper aware of the value of the dollar with respect of their peso. You cannot make major purchases like real estate without physical dollars. Most people purchase dollars as a form of a savings account. The only difference now is they won’t have to use the pesky pesos that are essentially monopoly money at this point.

David S

Nov 23 2023 at 5:54am

Thanks for this post, even if I did have to schlep over from the Bad Blog to read it.

You make a good point about how Argentina is effectively already dollarized because people have been relying on American cash as a store of value for decades. Javier has a good bully pulpit in that regard and I bet it got him votes. He would simply be bringing the monetary system in line with reality.

Alex

Nov 28 2023 at 8:14pm

The task at hand is monumental since his approach needs to somewhat mirror what El Salvador president is doing, the main goal would be to eliminate corruption, which is the largest virus. Time is also against him as the level of overall education in the country is so low that people expect Eutopia overnight and realistically four years aren’t sufficient to correct almost 100 years of corruption. Hope he succeeds but odds are against him

Comments are closed.