It’s easy to end a transitory inflation. It’s hard to end a persistent inflation. That’s why it’s essential that central banks engage in “level targeting”. Level targeting makes all inflation transitory.

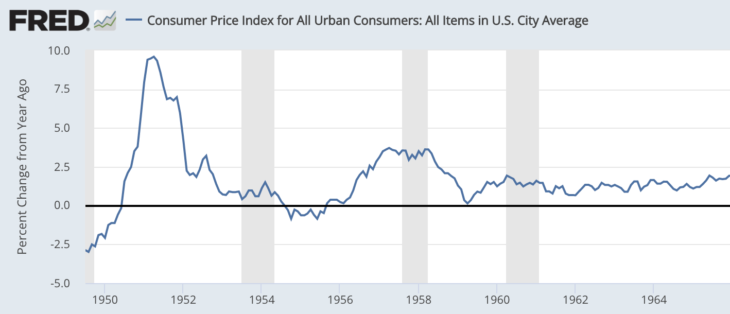

When the Korean War broke out in June 1950, the US economy was experiencing a period of mild deflation. By February 1951, the 12-month CPI inflation rate had reached 9.4%. By February 1952, inflation was back down to 2.2%. How did the Fed achieve success so quickly, without triggering a recession in 1952?

The transitory inflation of 1951 was not a supply shock—NGDP rose at an extremely rapid rate. Inflation would not end just because the supply shock went away. There were price controls, but it wasn’t just inflation that declined in 1952—NGDP growth also fell very sharply. So monetary policy did significantly reduce aggregate demand in 1952. (Contrast this with the 1971-74 price controls.)

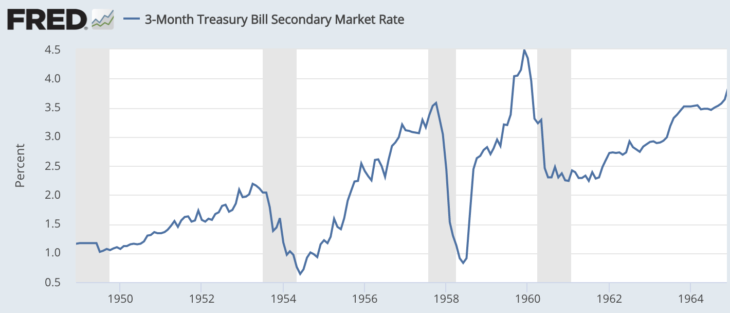

The key to the Fed’s 1952 success was level targeting. Between 1934 and 1968, the US pegged the price of gold at $35/oz. This provided monetary policy with credibility, keeping long-term interest rates at relatively low levels. As a result, the Fed was able to eliminate the high inflation of 1951 with a relatively small increase in short-term interest rates, as 3-month T-bill yields rose by only about 40 basis points between 1950 and 1952:

(A similar small increase in interest rates eliminated the transitory inflation of 1936-37; although that policy was too contractionary, pushing the economy into a deep slump in 1938.)

As recently as last September, the Fed’s FAIT policy still had some credibility. Markets assumed that the Fed would keep inflation around 2%, on average. Ten year T-bond yields remained around 1.3%. At the time, markets (wrongly) assumed that the Fed would engineer a 1952-style soft landing.

As Fed officials began moving away from their promise to keep average inflation near 2%, long-term bond yields rose sharply. Eliminating inflation will now be much more costly. Interest rates will have to rise more sharply and the economy will slow by more than if the FAIT policy had been maintained.

People often ask me how high the Fed needs to raise rates to control inflation. The answer depends on the policy environment. With a credible level targeting regime, only a tiny rate increase is required. But as we saw in 1981, without policy credibility a dramatic rate increase is required.

Right now the Fed is somewhere in between these two extremes. It has less credibility than in 1951 but more than in 1981. The longer they wait, the higher the price that must be paid.

READER COMMENTS

Michael Sandifer

May 7 2022 at 3:00pm

Good post. Inflation expectations haven’t fallen much since the peak after the spike that began after the invasion of Ukraine, but real growth expectations are down considerably this year. Hence, to control longer-run inflation within the FAIT framework will involve more tightening, as you suggest, but I wince because we’d do so much better right now with a level targeting framework.

Of course, you may say monetary policy hasn’t actually tightened, but my sense is that you’re very much in the minority in that view. Even inflation expectations are down a bit, and much more importantly, the expected NGDP growth path is certainly fallen this year, and continues to do so. My model has it at about 4.41% right now, down from just over 5% when the year began.

Scott Sumner

May 8 2022 at 11:53am

“but my sense is that you’re very much in the minority in that view.”

I seem to ALWAYS be very much in the minority on monetary policy.

Michael Sandifer

May 9 2022 at 10:53am

Yes, and you’re usually correct, despite being in the minority. I think this case is an exception though.

Mark Brophy

May 8 2022 at 11:17am

The Fed has stated that they’re going to raise the rate to 3% but that it’s going to take a long time. Instead, they should raise the rate to 3% immediately rather than pursue a bad policy for a long time. This might restore their credibility. However, I doubt they’ll eliminate inflation unless and until they raise the rate to 10%. That’s unlikely so we’ll suffer stagflation for at least 10 years. The Fed shouldn’t have printed so much money in 2020.

Scott Sumner

May 8 2022 at 11:51am

Fed policy in 2020 was appropriate. The problem is that they abandoned FAIT in 2021.

Spencer Bradley Hall

May 8 2022 at 11:45am

Net changes in Reserve Bank Credit are determined (or should be determined) by Fed policy period – ever since the Treasury-Federal Reserve Accord of 1951.

However, the Fed allows the banks to usurp its “open market power” by not acting – by ignoring the dynamics of money creation.

In 1965 William McChesney Martin Jr. re-established stair-step case functioning (and cascading), interest rate pegs (like during WWII), thereby abandoned the FOMC’s net free, or net borrowed, reserve targeting position approach in favor of the Federal Funds “bracket racket”. All the trading activity was on top of the brackets.

I.e., the Fed once again, began using interest rate manipulation as its monetary transmission mechanism, targeting nominal interest rates and accommodating the banksters and their customers whenever the banks saw an advantage in expanding loans.

Thus, the Fed ignored Bagehot’s dictum where the discount rate is made a penalty rate (beginning in Jan 2003). And the banks flaunt the Central Banking rule that borrowing should not be used for profit (sold back into the interbank or secondary market).

Monetarism has never been tried. Monetarism involves controlling total reserves, not non-borrowed reserves as Paul Volcker found out. Volcker targeted non-borrowed reserves (@$18.174b 4/1/1980) when total reserves were (@$44.88b) (i.e., absolutely no change from what Paul Meek, FRB-NY assistant V.P. of OMOs and Treasury issues, described in his 3rd edition of “Open Market Operations” published in 1974).

Spencer Bradley Hall

May 8 2022 at 11:59am

The economic engine is being run in reverse. Economists don’t know a debit from a credit. Interest is the price of credit. The price of money is the reciprocal of the price level. Powell, a banker’s banker, should force an absolute reduction in the money stock while releasing monetary savings. The solution to the 1966 credit crunch, the first one, is the correct operating model.

Monetary Flows { M*Vt }: `1966 Interest Rate Adjustment Act

Monetary Flows { M*Vt }

Spencer Bradley Hall

May 8 2022 at 12:36pm

It’s perfectly obvious. Short-term money flows are affected first. Raising policy rates disproportionately affects N-gDp, or restricts the velocity of circulation. It impacts R-gDp more so, applying a double whammy, than reducing inflation by reducing the money stock.

Orion

May 8 2022 at 2:41pm

But you aren’t taking the deficit and velocity of money into consideration which aligns where we are much closer to the 1950s than in the 70s. With the velocity of money so low we need the government to signal that the era of the pandemic is officially over and we are in the safe endemic mode. The ideology of the pandemic era must end. People aren’t and rarely ever died in hospital corridors waiting for assistance.

Scott Sumner

May 9 2022 at 10:49am

“But you aren’t taking the deficit and velocity of money into consideration”

Yes I am.

Orion

May 8 2022 at 2:44pm

The FEDs tightening will really spook people and there will continue to be a downturn until an epic upwards momentum like there was in the 50s. when it either stabilizes or drops back to 0. There is too much money laying around being hoarded and the FED needs people to start spending big time.

Spencer Bradley Hall

May 8 2022 at 4:38pm

The importance of Irving Fisher’s Vt in formulating or appraising monetary policy derives from the fact that it is not the volume of money which determines prices and inflation rates, but rather the volume of money flows relative to the volume of goods and services produced (one dollar that turns over 5 times can do the same work as five dollars turning over only once). Thus, to stop inflation, you drain the money stock.

Comments are closed.