I don’t believe that it makes sense to speak of the true rate of inflation. After all, no one seems to know what inflation is supposed to be measuring. Some economists might argue that it represents the increase in pay you’d need so that you are not worse off in terms of utility. But what does that mean?

Suppose I met a Gen Zer who said he rather earn $100,000 today than $100,000 in 1955 (when I was born.) After all, today he can have better medical care, better Asian cuisine, better TVs, the internet, smart phones, etc., etc. Would that imply that there had been no rise in the “cost of living” since 1955, at least for that individual? In my view, that would be a silly way to view inflation. But given textbook definitions, how can I say he’d be wrong?

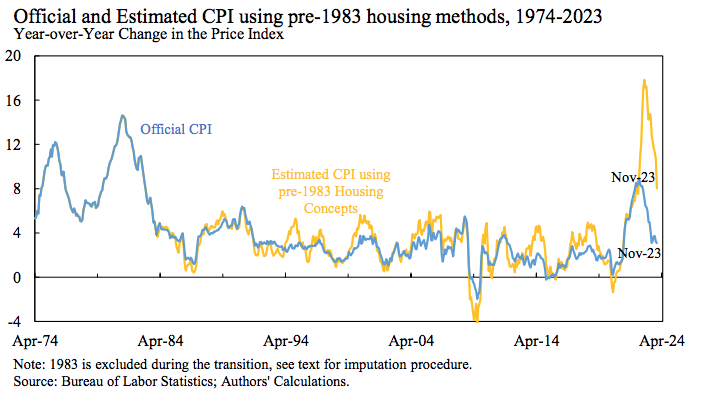

If I’m correct that inflation is somewhat subjective, I’d still insist that some price indices are more useful than others. Josh Hendrickson directed me to a paper by Marijn A. Bolhuis, Judd N. L. Cramer, Karl Oskar Schulz, and Lawrence H. Summers (BCSS), which estimates recent inflation using the techniques that were used prior to 1983. They put more weight on things like financing costs, which have risen sharply during a period of rising interest rates:

In their revised estimates, 12-month CPI inflation peaked at 18% in November 2022, and remained at 9% even in November 2023. (The official figures show CPI inflation peaking at only 9.1%.) Unless I’m mistaken, the revised data implies a 28.6% total increase in the CPI between November 2021 and November 2023. Let’s compare that to some other data points:

Revised CPI: +28.6% between 11/21 and 11/23

Nominal GDP: +13.4% between 2021:Q4 and 2023:Q4

Nominal consumption: +12.9% between 11/21 and 11/23

Nominal average hourly earnings: +9.6% between 11/21 and 11/23

Taken at face value, a 28.6% rise in the price level at a time of much slower nominal growth implies that the US fell into one of the deepest depressions in US history. In fairness, it’s not quite right to compare the CPI with nominal GDP, as the CPI only measures the price of consumer goods. You need the GDP deflator.

But notice that nominal consumption rose even more slowly than nominal GDP (although both are actually growing rapidly by 21st century standards). So if the revised CPI figures are true, then it seems as though real consumption must have plunged at an astounding rate—comparable to a major economic depression such as the 1930s.

I suppose one could argue that the same techniques that BCSS used to adjust the CPI might also impact nominal aggregates such as consumption and NGDP. Even so, it’s hard to believe that any plausible adjustment in aggregate consumption growth could even come close to closing the gap with the revised CPI inflation estimate.

In addition, any problems with nominal consumption would not bias the estimate of nominal average hourly earnings, which rose by only a total of 9.6%. I suppose it is technically possible that nominal wages rose by 9.6% at a time the cost of living rose by 28.6%, but what would that imply about the rest of the economy? Wouldn’t that imply a major economic crisis where workers were unable to afford anything more than the most basis necessities? And yet, everywhere I look I see evidence of a booming economy.

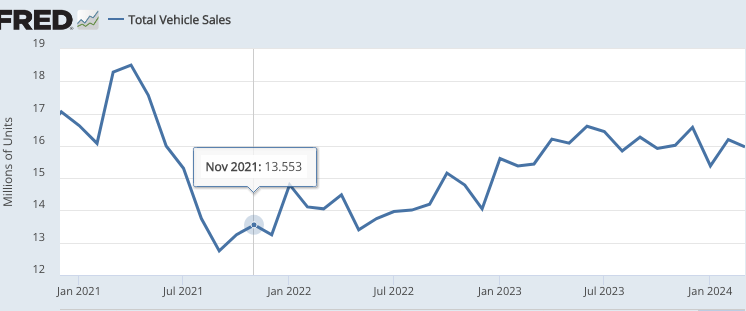

To take one example, car sales tend to fall sharply during “hard times”. And yet car sales have increased sharply during this period of rising interest rates:

And car sales are generally far more cyclical than other types of consumption like health care, education and haircuts. Why have they risen sharply since November 2021?

All our economic data points suggest strong output growth. The job market is extremely strong, with low unemployment and very robust growth in total employment. If you adjust for demographics (the aging population), then the employment-population ratio is back near the peak levels of 1999-2000.

If you ask people why we need inflation estimates, they’ll typically say something to the effect that inflation adjustments allow us to figure out how the economy is actually performing, without the distortions created by a declining purchasing power of money. In other words, we use inflation to convert nominal variables into real variables. But when I try to apply the BCSS inflation estimates to any sort of plausible nominal variable in the US economy, I come up with real variables that literally make no sense.

To be clear, this is not a criticism of the BCSS paper, which focuses on one very narrow question—why is consumer sentiment so poor, despite a strong labor market? They may be correct in claiming that rising financing costs largely explain the public’s surprisingly sour mood.

Rather, my argument here is that these inflation estimates are not useful in a conventional sense. If we try to use them to convert nominal variables into real variables, we end up with nonsense. What am I missing?

READER COMMENTS

Andre

Apr 6 2024 at 6:25pm

“why is consumer sentiment so poor, despite a strong labor market?”

1. Prices outpaced nominal wages for most of the last three years, with wages only exceeding prices over the past year. But the net area between the curves is negative: consumers lost purchasing power: only now are median real wages reaching the level they were at when Biden took office. It seems unlikely the average person will be made whole this year, so this presidency period will be a net negative for real wages.

2. It’s a tale of two different types of households. Lots of people are better off than four years ago: asset owners and the laptop class come to mind, as well as those who are employed near the bottom, at the now de facto higher minimum wages – earning, say, $15-$20 instead of $10 pre-Covid. However, since the average person is between worse off and no better off, that means that there are tens of millions (well, more than half the country) out there who have taken a real hit to their purchasing power – I suspect that these are folks who for many reasons can’t or won’t change jobs. Here I’m thinking of folks in income quintiles 3 and 4. Inflation favors job changers, and many of these folks, because of where they are or because of loyalty to an employer, or other reasons, are less willing to or unable to switch jobs

3. Food and shelter are up about 20% each, higher than the increase in the CPI (18% since Feb 2021). The laptop class is hit less by food and shelter than the average person.

Craig

Apr 6 2024 at 10:38pm

“Food and shelter are up about 20% each, higher than the increase in the CPI (18% since Feb 2021).”

Once paid if interest rate is fixed, you’ve paid the price and now have a stable finance agreement for the next 30 years. South FL does have the hurricane threat, but I locked in at 2.25% — good deal for me, my payment went down, then the inflation hit and the home owners insurance went up so from the post refi rate and so the housing payment which is mortgage/property taxes/homeowners that payment went up 32% and when things like that happen, it gets people worried because it went up 32% and they’re talking about it going up even more. Is it going to go up another 32%? I don’t think so, but many are worried about it.

Things don’t seem very stable.

Thomas L Hutcheson

Apr 7 2024 at 8:03am

Aren’t insurancertes more related to the growing awareness of hurricane risks?

Jon Murphy

Apr 8 2024 at 7:17am

Unlikely. Why would insurers have been unaware of their job until recently? Besides, that would only affect insurance in Gulf states.

If I may draw on my expertise given I recently testified on this matter before the NC House Committee on Oversight and Reform:

Insurance rates are being heavily driven by several factors:

-Tariffs increasing the costs of repairs

-Legislative restrictions on who can do what work

-inflation

-The legal framework of an insurance market (specifically how easy it is to sue someone and the structure of the state’s residual market)

Scott Sumner

Apr 6 2024 at 11:01pm

It’s misleading to compare median wages to early 2021, when the figures were distorted by Covid. The main reason why the public is so negative on the economy is that Republican respondents are extremely negative. But when you ask people about their personal financial situation, they give much more positive responses.

I don’t take these poll figures at all seriously.

https://www.themoneyillusion.com/theres-no-such-thing-as-public-opinion-example-2178/

Tristan

Apr 6 2024 at 9:23pm

Speaking of Josh, have you had a chance to read his recent paper, “The Treasury Standard: Causes and Consequences” ?

Scott Sumner

Apr 6 2024 at 11:02pm

No, I have not.

Craig

Apr 6 2024 at 10:31pm

“why is consumer sentiment so poor, despite a strong labor market? They may be correct in claiming that rising financing costs largely explain the public’s surprisingly sour mood.”

I agree and add in housing costs which, in many, not all, the price increases have greatly outpaced inflation. South FL is one such market, my home which I bought for $X in 2018 is now 1.74X and so somebody would have to pay that and the financing. Not saying this is every market but it is a large one and there are millions of people here and same with NY metro etc. Many may be employed and may even see their wages outpacing inflation, but many are not seeing their wages outpace the growth in their housing payment. I locked in 2.25% so I have the bank right where I want them, but inflation means the premiums for home insurance went up and that’s baked into the housing payment.

While I am in team disinflation for right now I also think there are more than a few price increases which really shock people. South FL you get a haircut, its $25 pre tip now, car wash in/out is not $37.50 pre tip. Even McDonalds, I took my son and his friend to McD’s and it was $40 and I was just flabbergasted at that, other eateries are similar. Throw on ‘tip creep.’ Quite a few things people are thinking, “Whoa, whoa, whoa, what’s going on here?”

Scott Sumner

Apr 6 2024 at 11:07pm

Interesting, I pay $16 for a haircut in Orange County (pre-tip). But I have also seen large price rises for meals, etc. Gas is $5.50 around here.

On the other hand, I don’t actually believe the claims that consumer sentiment is poor. I don’t trust polls, and people seem to be enjoying fairly high levels of consumption. The economy is booming.

Dylan

Apr 7 2024 at 9:27am

I just spent a few weeks in southern California, inland from the coasts a bit, and I was shocked at how cheap prices were. It literally felt like stepping back in time 20 years. A movie theater ticket was $7. I bought lunch for two in a sit down restaurant with drinks and it was $25. That’s close to what I pay for one person for a fast casual meal in NYC. A haircut at my barber went from $35 to $45 this year before tip.

Craig

Apr 7 2024 at 9:33am

Suppose polls could be wrong, but I’d suggest the simplest explanation is angst about the future on the backdrop of a miserable Zeitgeist.

Scott Sumner

Apr 7 2024 at 12:27pm

I do accept the polls that suggest that people are generally satisfied with their personal situation. For the overall economy, people are reacting to a drumbeat of negative news. And again, it’s largely driven by extremely negative ratings by GOP voters who may be personally doing fine, but don’t like Biden.

Thomas L Hutcheson

Apr 7 2024 at 8:08am

It may not affect the ch of “prices” and “wages” that much, but beat in mind that we do not actually have data on movement in _wages_. BLS produces only unit values of wage payments, not indices of job to job wage comparisons. https://thomaslhutcheson.substack.com/p/improvements-in-macroeconomic-data

Dylan

Apr 7 2024 at 11:08am

Another comment on the “public’s surprisingly sour mood.” I know that it is dangerous to try to extrapolate from anecdote, but I’m human and it is a hard habit to break. And the sentiment in my little corner of the world has been horrible for about two years now. Mid to Senior level people getting laid off from good jobs, and it taking months before they can even land an interview. I know multiple people, including myself, that have been out of work for a year or more. And, when they do get a job, it’s come with large cuts in salary. That’s been true for the folks that I know that are lucky enough to have a job, but are unhappy with it and have been looking for a new one, the salaries are just across the board lower.

Put this against a backdrop of where, for the first time for many, it seems that the soft and hard skills that have been so lucrative for them in the past are really under technological threat. How valuable is the ability to crank out really good PowerPoint slide decks these days? How valuable will it be in two years? I know lots of people that are supposed to be just hitting their prime earning years, and instead have been taking pay cuts of 30-50% just so they can have some kind of job. And the ones that haven’t done that, have certainly heard the stories from their former colleagues and are scared that’s going to be them next. Also, for the record, these are decidedly not Trump voters in my circle, but they are nevertheless quite apprehensive about the economy.

Scott Sumner

Apr 7 2024 at 12:24pm

You need to keep in mind that in any large economy, there will be lots of variation. The data suggests that in recent years the wages of low paid workers has grown fastest, while the pay of high paid workers has grown at the slowest rate.

But with 3.8% unemployment and rapid overall job growth, it doesn’t seem like your local situation is representative of the entire economy. However, I don’t doubt that it is representative of a certain segment of the economy. Are you in the tech sector?

Craig

Apr 7 2024 at 1:11pm

Aside from the Biden comment you made above which I do believe is correct –>

“But with 3.8% unemployment and rapid overall job growth”

One consequence of inflation is that it puts the fear of future inflation into people’s minds. (rightly or wrongly) the angst is whether the job will be able to cover the price increases they MAY face.

Jon Murphy

Apr 7 2024 at 2:41pm

While that’s certainly a major aspect of inflation, as Scott points out people’s behavior does not reflect this anxiety.

Craig

Apr 7 2024 at 2:59pm

I disagree, YOLO, inflation means spend it before the money loses its buying power.

Jon Murphy

Apr 7 2024 at 5:42pm

Hm. I see where you are coming from. But, alternatively, if you’re afraid of being able to afford things in the future, people would start saving now.

So, we might expect people to buy durable goods to avoid future price increases. But that cannot explain spending on luxuries.

Dylan

Apr 7 2024 at 1:50pm

I’d say I’m tech adjacent. Corporate strategy is the field, but since corporate strategy for the last decade has primarily been how companies can use technology to scale, no matter what industry they’re in, tech as a distinct sector has kind of lost relevance.

But, it also feels broad in other ways. I work with lots of startups. Startups have high failure rates, but as of a couple of years ago, being the failed founder of a venture backed startup was the entry point into a wide variety of career choices. Last year I know a bunch of founders that failed, stellar resumes as early employees at name brand institutions, the kind of people that you have trouble imagining could ever have trouble getting a job. One friend, after 8-months of no income and nothing left in savings was finally applying to coffee shops, and still not able to even get an interview. Another was previously CEO of an internet company you’ve heard of that got acquired by a bigger company, there she was a senior level executive of a division of a few hundred people. Was let go when they closed the division and after a year of looking, finally accepted a job at a much lower level, leading a team of 3 people.Totally understand and agree with you that there’s lots of variation, and that in any economy you will find stories like these and also stories of people doing great. One thing though, while I work in startups, which are a small part of the economy, I do work with startups in every sector and, outside of AI, there hasn’t been any sectors where people think things are going super well (and venture stats mostly back that up)

Lizard Man

Apr 7 2024 at 10:02pm

I have been reading recently the opinion that a lot of venture capital and startups were a zero interest rate phenomenon. How much do the skills that people have in startups translate to the old economy, whether it be in non IT SMEs or large and well established companies, or companies that do consulting or outsourced work for those types of organization?

Dylan

Apr 7 2024 at 10:34pm

That’s the thing, I don’t even know what old economy means anymore? In my last job, I did a bunch of work with old school manufacturing and industrial companies, the kind of names that probably pop into your head when you think of the Rust Belt, yet those were already either on the cutting edge of technology or working really hard to get there. Using Computer Vision, Robotics, AI in supply chains, location beacons that allowed 10cm accuracy tracking inside warehouses, real time digital twins. And all of those companies seemed desperate to get their hands on people with startup experience, partially for the technical skills, but also just for the fact that they knew how to get things done without needing a huge budget and team.

Similar stories can be told about healthcare, education, construction, and the list goes on. Software really is eating the world, and it is hard to find a sector of the economy that isn’t impacted.

spencer

Apr 7 2024 at 11:55am

If you don’t include asset prices, you miss a good proportion of inflation.

Bernanke, pg. 287 in his book “The Courage to Act”, “Lower long-term rates also tend to raise asset prices, including house and stock prices, which, by making people feel wealthier, tends to stimulate consumer spending” (aka the “wealth effect”).

“Housing is considered unaffordable if it costs more than 30% of an individual’s income”.

Jose Pablo

Apr 7 2024 at 7:39pm

the true rate of inflation

That’s a very interesting question. Particularly taking into account how dependent it is on your own “personal” basket of goods and services. Which sure don’t mimic the “average” basket resulting from the Consumers Expenditure Survey.

Individual preferences can make a huge difference.

https://www.weforum.org/agenda/2023/02/charted-heres-how-us-goods-and-services-have-changed-in-price-since-2000/

If you are, mostly, into toys and televisions …

Lizard Man

Apr 7 2024 at 9:55pm

I suspect that the Democrats have also changed in the past 10 years. There is a pretty big gap between older and younger Democrats on how they feel about the economy, with younger Democrats being more pessimistic. This also lines up with older Democrats being more moderate, and younger Democrats being more ideological. I suspect that the divide is between people who view the world through some kind of ideological lens, and people who are more normal. Republicans as a whole are more ideological, which in part explains why they watch Fox News in the first place. But Democrats, especially young ones, are becoming more ideological as well. And both are angry that the world doesn’t conform to how they think it ought to be, and to admit that the economy was doing well would be inconsistent with their sense of grievance.

Cove77

Apr 7 2024 at 11:31pm

FOX News viewers don’t tune in for just 30 min a nite and go about their day. It’s an incessant drumbeat. (Maria Bartaromo just claimed that employment data and SPX are so strong cause employers and mkt are expecting a Trump win in 7 months)

David S

Apr 8 2024 at 7:11am

Share of income spent on shelter is the only price index that matters. I’m mostly just repeating Kevin Erdmann on this point—he has a good Substack post on this.

Also, the neighborhood kids jacked up the price of lemonade at their sidewalk stand to $3–but I reported them for violating zoning regulations.

robc

Apr 8 2024 at 12:56pm

My preferred inflation measure: Change in M2 per capita.

robc

Apr 8 2024 at 1:01pm

From 2000 to the pandemic, M2 growth generally trended between 5 and 10% per year, while population growth was about .8%.

M2 growth shot up to over 25% during covid but has been negative since the end of 2022.

If I am thinking correctly (maybe not), the difference between M2 growth per capita and price level growth would be due to productivity growth?

D F Linton

Apr 8 2024 at 4:22pm

If using a cpi based on 1984 methods today gives unreasonable values for real variables doesn’t that mean that using pre 1984 cpi series is equally bad?

Ramesh Iyer

Apr 16 2024 at 3:31am

Regarding “They put more weight on things like financing costs, which have risen sharply during a period of rising interest rates”

IMO The financing cost / interest rates have a very dynamic relationship to CPI. Once can see this if you plot change in CPI along side interest rates. The close association until 2008 starts to diverge completely starting 2009 as a intervention to recoup from the financial crises.

Another aspect we should consider when reasoning “why is consumer sentiment so poor, despite a strong labor market?” is the Cares Act ($2.2 trillion economic stimulus bill) this is an absolute anomaly in Fiscal & Monetary policy ($300 billion in one-time cash payments to individual, $260 billion in increased unemployment benefits, $669 billion Paycheck protection & forgive loans programs, $500 billion in loans for corporations).

This created a boom business cycle for many sectors most notably in fashion & lifestyle brands.

With this spending tapering down we will see some of its effects on spending disappear.

How do you see these two aspects?

Comments are closed.