In order to have a successful monetary policy, it is necessary to understand what success looks like. I fear that many pundits have the wrong view of success. They envision heroic central bankers valiantly fighting against cycles of too much spending and too little spending.

In fact, that’s what failure looks like. To see why, it will be helpful to first review the famous Newcomb’s Paradox:

Imagine that an omniscient entity puts $1000 into Box A and either $0 or $1,000,000 into Box B. You can choose to take either Box B alone, or both Box A and Box B. It seems like it’s better to take both boxes. But there’s a twist. The omniscient entity (OE) tells you that it can predict your future actions, and if it thinks you will greedily take both boxes, then it will only put $0 into Box B.

There are many ways to think about this paradox, depending on your views of free will, determinism, and omniscience. For our purposes, however, I’d like to explore one particular train of thought.

At first glance, I might decide to take both boxes, because at the point I make the decision, the OE has already put the money into the two boxes. Taking both boxes gives me a higher expected value than taking just one box.

Alternatively, I might fear the OE’s omniscience, and decide that one box is the safer bet. But how do I avoid changing my mind at the point when I make the choice, after the OE has already decided? I do so by changing the sort of person I am at the point where the game is explained to me. I change my personality from a cynical profit maximizer to a sincere and honest person, the sort of person that will always do what he or she commits to do (even if the commitment is introspective, not verbalized.)

According to this interpretation, because the OE is omniscient the only path to success is a sincere change in your personality—a sort of “Road to Damascus” moment in your life. Anything less will be perceived as insincere, and will lead the OE to put $0 into Box B.

Central banks also face a commitment problem. They need to commit to a policy that is something close to NGDP level targeting, and promise to return to the target path if their are deviations. If the commitment is credible, then NGDP will rarely deviate far from the target path. In other words, the economy will magically seem to become almost free of “shocks”.

If the central bank policy is not credible, then NGDP will often wander far from the trend line, and central bankers will be frequently required to fix problems by boosting or restraining growth in spending. If successful in eventually fixing these problems, they become lauded as heroes by a public that doesn’t understand that the so-called “shocks” were caused by previous errors in monetary policy. Even worse, it’s not just that there were previous errors, there was a policy regime in place that made errors much more likely.

In Newcomb’s Paradox, the prospect of taking both boxes becomes frightening, due to the OE’s omniscience. At the point in time when you actually choose, it may be tempting to see the game as one where “bygones are bygones”, as the OE’s decision has already been made. And then grab both boxes. But a wiser participant in the game will fear the omniscience to the OE and stick with their previous internal commitment to take one box.

When inflation overshoots its 2% target, a central bank that previously committed to average inflation targeting will be tempted to abandon the commitment and refrain from bringing the average back down to 2%. After all, the commitment had already done its job and spurred a strong recovery. But if the financial market understands that the central bank is not sincere, then it will fail to move interest rates in the sort of anticipatory way that would prevent the inflation overshoot. The central bank’s lack of sincerity will cause the very problem they are later praised for resolving.

Successful central bank policies don’t look exciting, full of adept and timely actions by central bankers. They look boring, as if the central bank is presiding over a “lucky country” that is almost free of destabilizing shocks. (What did Napoleon say about lucky generals?)

Market forecasts are nowhere near as accurate as my imaginary OE, but they are still the best that we have. Thus I become very frightened when people ask what the central bank should do when things go way off course. The fact that the economy is far off course means that the market has already determined that the central bank lacks commitment to fix the problem. How likely is future success when the world’s best forecaster believes that you will fail? So what should the Fed do when it’s far off course? I’m reminded of what the laconic farmer said to the lost motorist: “First of all, I wouldn’t start from here.”

Australia is often referred to as the lucky country. Apart from a brief Covid slump, Australia has gone more than 30 years without a recession. When I speak to people about this case, they instinctively assume that Australia must be lucky—its economy has somehow avoided being hit by shocks. After all, if you don’t believe that central banks cause our recessions (and most people don’t), then how else can one explain Australia’s success?

In fact, Australia is an unlucky country. It’s a small economy that is highly dependent on the export of a few commodities, which is a highly unstable sector. A lucky country would be focused on a stable sector, such as services. Australia is buffeted by much stronger non-monetary shocks than is the US economy. It doesn’t look that way because we have many more recessions. But that’s because we have had a much less stable monetary policy. Unlucky Australia has outperformed the lucky USA.

PS. Students of history might see an analogy to how we rate presidents. Boring presidents that preside over peace and prosperity (say, Coolidge) are placed near the bottom of the rankings by historians. Like economic pundits, historians place active presidents that screw up (say Wilson or LBJ) far ahead of boring presidents that don’t create problems in the first place.

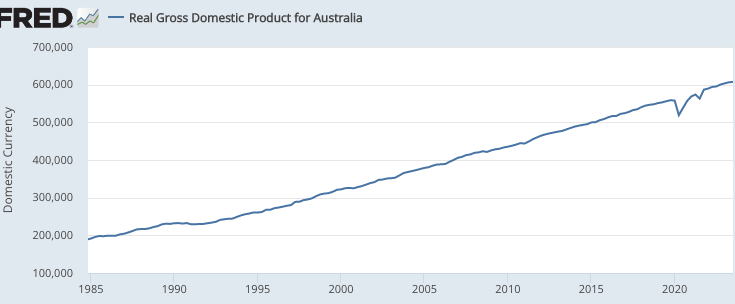

PS. During Australia’s only recent recession, unemployment rose from 5.2% in March 2020 to a peak of 7.5% in July 2020. It was back down to 5.1% by May 2021. That’s far better than the US. Here is Australia’s boring real GDP graph:

PPPS. Others have also argued that success is banal. Here’s what Orson Welles’ character says in The Third Man:

In Italy for 30 years under the Borgias they had warfare, terror, murder, and bloodshed, but they produced Michelangelo, Leonardo da Vinci, and the Renaissance. In Switzerland they had brotherly love – they had 500 years of democracy and peace, and what did that produce? The cuckoo clock.

READER COMMENTS

David Henderson

Jan 3 2024 at 10:55am

I remember that line well, from when I first saw The Third Man. I was only a teenager and not even a libertarian, but I remember thinking “I’ll take the cuckoo clock.”

Scott Sumner

Jan 3 2024 at 2:00pm

And Switzerland has produced some great artists.

MarkW

Jan 4 2024 at 8:25am

But apparently not cuckoo clocks (thought that’s beside the point).

Tsergo Ri

Jan 3 2024 at 1:30pm

Can you again explain why NGDPLT is better than SNB’s policy of bringing inflation below 2% ASAP?

Scott Sumner

Jan 4 2024 at 1:38am

If we had NGDPLT, then inflation would already be below 2%.

Henri Hein

Jan 3 2024 at 2:34pm

That leads to the question what kind of regime the Australian central bank follows? Wouldn’t that be something to emulate?

Scott Sumner

Jan 4 2024 at 1:39am

I’m not sure what their regime is.

Junio

Jan 3 2024 at 3:56pm

Interesting post, Scott. I always do appreciate your analogies.

steve

Jan 3 2024 at 5:12pm

Have to think about this one, especially in light of supply shocks. If you have a supply shock that is truly a surprise, it seems like it might take a while to respond.

Query- It seems to me that our fiscal policy has also been pretty hit and miss and not particularly stable, other than the relentless pursuit of expenses exceeding revenues. Anyway, from my POV it certainly looks like the Fed could often be playing catch up for poor fiscal policy.

Steve

Lizard Man

Jan 3 2024 at 7:16pm

How has Australia’s central bank responded to supply shocks? It looks to me like the US Fed had a large COVID supply shock to deal with, and decided to deal with that by letting inflation/NGDP growth go above target instead of trying to cool off the labor market. They were too accommodative for too long, leading to AD/NGDP growing too fast. But how should central banks deal with negative supply shocks? Should they let inflation rise to try to maintain higher employment, and then once the economy seems to be on its way to adjusting to the supply shock commit to a path of slower NGDP to get back to the level implied by the previous trend? Should they treat deflation as something that they should avoid, or should they set NGDP growth low enough that the economy will experience deflation in order to get back to the level trend?

The policy of the Fed appears to be to deal with supply shocks through higher inflation and then get inflation/NDGP growth back to trend. Would it even be credible for the Fed to commit to below trend NGDP growth for a long time horizon?

Scott Sumner

Jan 4 2024 at 1:37am

They should not react to supply shocks at all—just keep NGDP growing at about 4%, with level targeting.

Todd Ramsey

Jan 4 2024 at 10:33am

Would a one-year-out +4% NGDP level target have worked in March 2020, given the uncertainties of the moment, without benefit of hindsight? Would a two-year-out target have been more appropriate?

Should the Fed always be targeting two years out, as opposed to one year?

Scott Sumner

Jan 4 2024 at 11:49am

In March 2020, it might have been better to target 2 years out. In general, I don’t think it makes much difference.

Lizard Man

Jan 4 2024 at 11:53am

Wouldn’t keeping NGDP growth level in the face of a large supply shock (especially one that is driven by a ubiquitous input like an energy price shock) lead to much larger spikes in unemployment than a regime that allowed for spikes in NGDP growth that then brought it back to trend? Like take the oil price shocks of the 1970’s. Let’s say that NGDP growth stays the same, and the price of everything requiring oil goes up, and the price of everything else falls as people cut back on spending. Given the role of debt, a lot of businesses go bankrupt, when many of them would be able to remain as going concerns in a more inflationary environment (not all of them). With the lower number of businesses, employment and wages fall. What benefit is there to idling a lot of workers, instead of having them do useful things?

Scott Sumner

Jan 5 2024 at 1:04pm

There is a theoretical argument for targeting aggregate nominal wage income instead of NGDP, but in the case of the US I don’t think it makes much difference, especially if you are targeting one year forward NGDP.

Thomas L Hutcheson

Jan 5 2024 at 7:47am

Given a shock that was outside the range of shocks for which the target NGDP ws optimized , to keep NGDP growing at some particular rate would require some change in the settings of its policy instruments based on its model of how instrument settings affect NGDP, right?

vince

Jan 3 2024 at 9:13pm

Maybe a little off topic, but I like your choice of overrated Presidents, Wilson and Johnson. IMO they destroy the credibility of the rankings.

As for Newcomb’s Paradox, I would flip a coin between box A and both boxes.

Matthias

Jan 6 2024 at 5:11am

If you want to play those games, then you should go further:

Assume you have one day to make your choice.

So you commit to take one box if tomorrow’s S&P500 goes up, and two boxes if it goes down.

Then you construct a portfolio that hedges the whole thing, so that either your stock market bet pay off handsomely or you get a nice reward from the box.

(If it’s somehow possible for a friend to check the boxes, without you learning anything about them, that would work even better. Use some relativistic speeds, to reorder events in the relevant frames of reference.)

MarkW

Jan 4 2024 at 8:41am

Successful central bank policies don’t look exciting, full of adept and timely actions by central bankers. They look boring, as if the central bank is presiding over a “lucky country” that is almost free of destabilizing shocks.

That’s how things should look. But unfortunately, that seems not to be the common perception of the general public, economists, or central bankers. I’m reminded of HL Mencken:

“The whole aim of practical politics is to keep the populace alarmed (and hence clamorous to be led to safety) by an endless series of hobgoblins, most of them imaginary.”

To which we might add, “…and the genuine hobgoblins often created by ‘practical’ politics”

I’m also reminded of a wonderful book of fairy tales by Terry Gilliam (of Monty Python) we read to our kids called, The Beast with a Thousand Teeth. One of the storied involves a kingdom where a dragon lands on a rooftop. The king calls the chief dragon slayer who advises that this particular dragon is old and tired. It won’t bother anybody and will leave on its own after it has rested. Unhappy with this answer, the king calls in the assistant dragon slayer, who says that, no, the dragon must be destroyed. The king takes his advice and the dragon is killed (along with a number of the King’s subjects) during the battle. Naturally, the king basks in great public acclaim and pins a medal on the assistant and promotes him to chief dragon slayer.

Scott Sumner

Jan 4 2024 at 11:50am

Good analogies.

Market Fiscalist

Jan 5 2024 at 4:26pm

Suppose the CB had day-by-day accurate information on NGDP (or perhaps tracked a NGDP futures market). Every time it dropped below target it increased the money supply and every time it exceeded it it reduced the money supply.

Would it matter in this case whether the CB had credibility or not ?

Jose Pablo

Jan 5 2024 at 5:31pm

When inflation overshoots its 2% target, a central bank that previously committed to average inflation targeting will be tempted to abandon the commitment and refrain from bringing the average back down to 2%

“bringing the average back down to 2%”, would mean bringing the inflation well below 2%.

Afterall the inflation (cpi) has averaged 2.8% for the last 10 years (from Nov-2013 to Nov 2023) and 2.58% for the last 20 years.

I don’t think that’s what markets think the FED is going to do: bringing the inflation well below 2% for a period of time long enough to bring the average back to 2%, since this would mean keeping the inflation below 1.25% for the next 10 years.

Why, in your opinion, should the FED do that?, it is far from clear that doing this “guarantees” a “shockless future”

Alex S.

Jan 5 2024 at 11:22pm

Successful central bank policies don’t look exciting, full of adept and timely actions by central bankers. They look boring, as if the central bank is presiding over a “lucky country” that is almost free of destabilizing shocks.

Reminds me of my favorite line from Futurama:

“When you do things right, people won’t be sure you’ve done anything at all.”

PS: According to ChatGPT, an unofficial motto of Australia is “The Lucky Country”.

Matthias

Jan 6 2024 at 5:14am

Keep in mind that it’s not just a central bank that’s important here. Absence of destabilising regulation of the financial sector also helps the economy.

George Selgin wrote a lot about that.

Eg absence of minimum reserve ratios. Absence of bans on private bank notes, etc.

Comments are closed.