Back in the early 1980s, the Fed tried to gradually squeeze high inflation out of the economy, so as to avoid a bout of high unemployment. They failed. But it was not a failure to control inflation; it was a failure to bring inflation down gradually. Inflation fell much faster than almost anyone anticipated, and as a side effect the unemployment rate soared to a peak of 10.8% in late 1982. This convinced many that reducing inflation was costly, and that it was best not to allow the inflation genie out of the bottle in the first place.

[To be sure, there is more evidence for this claim that just the 1982 recession. Anti-inflation programs also led to recessions in 1921, 1957, 1970 and 1991, to name just a few examples. But 1982 was a particularly dramatic case.]

So what did we learn from the 1982 experience? Did this show that gradualism doesn’t work? Not exactly, as a necessary precursor for gradualism never occurred. The 1982 recession showed that gradualism is not easy to implement, but it provided no evidence on whether it would work if implemented.

So what is the necessary precondition for gradualism to work? The central bank must engineer a gradual slowdown in the growth rate of NGDP. That’s the only reliable method for achieving a “soft landing”.

A few weeks back, Tyler Cowen wrote a Bloomberg piece criticizing the economics profession for its failure to explain the economy’s surprising strength in 2023. And some of those who correctly saw that we might avoid recession had previously advocated models where inflation could not be brought down without high unemployment.

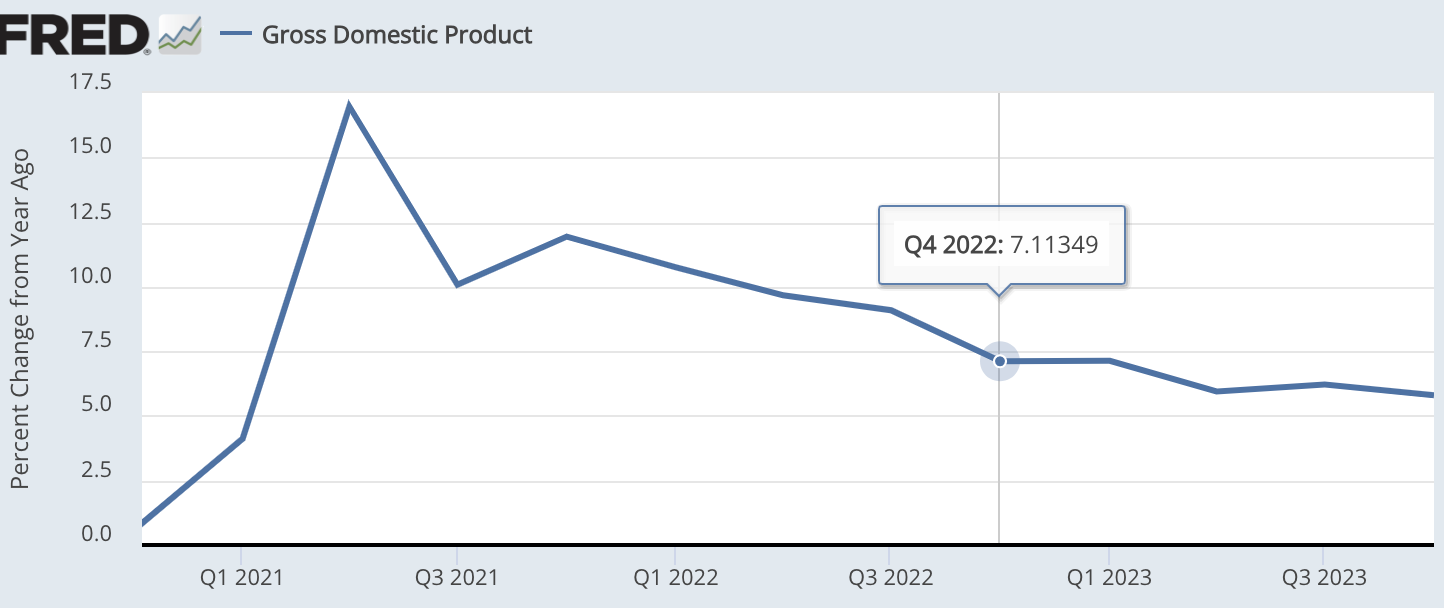

It’s a very good article, but Tyler fails to mention the fact that 2023 is a strong piece of evidence in favor of one particular approach—gradualism. For instance, look at the modest slowdown in 12-month NGDP growth from 7.1%.in late 2022 to 5.8% late 2023:

When presented with this argument, many people complain that I’m engaged in a tautology. “Growth slowed gradually because growth slowed gradually.” Those making that complaint are confusing nominal GDP with real GDP, a completely unrelated concept. The fear has always been that sharply slowing inflation would be costly in terms of falling real GDP and high unemployment. When economists use the term ‘growth’, they are referring to real GDP, not nominal GDP.

Thus there is nothing tautological in a claim that a recession might be often be associated with slow growth NGDP. For instance, in 2008, Zimbabwe’s real GDP fell even as its NGDP rose more than a million-fold. The two are radically different concepts, which do not always move in the same direction.

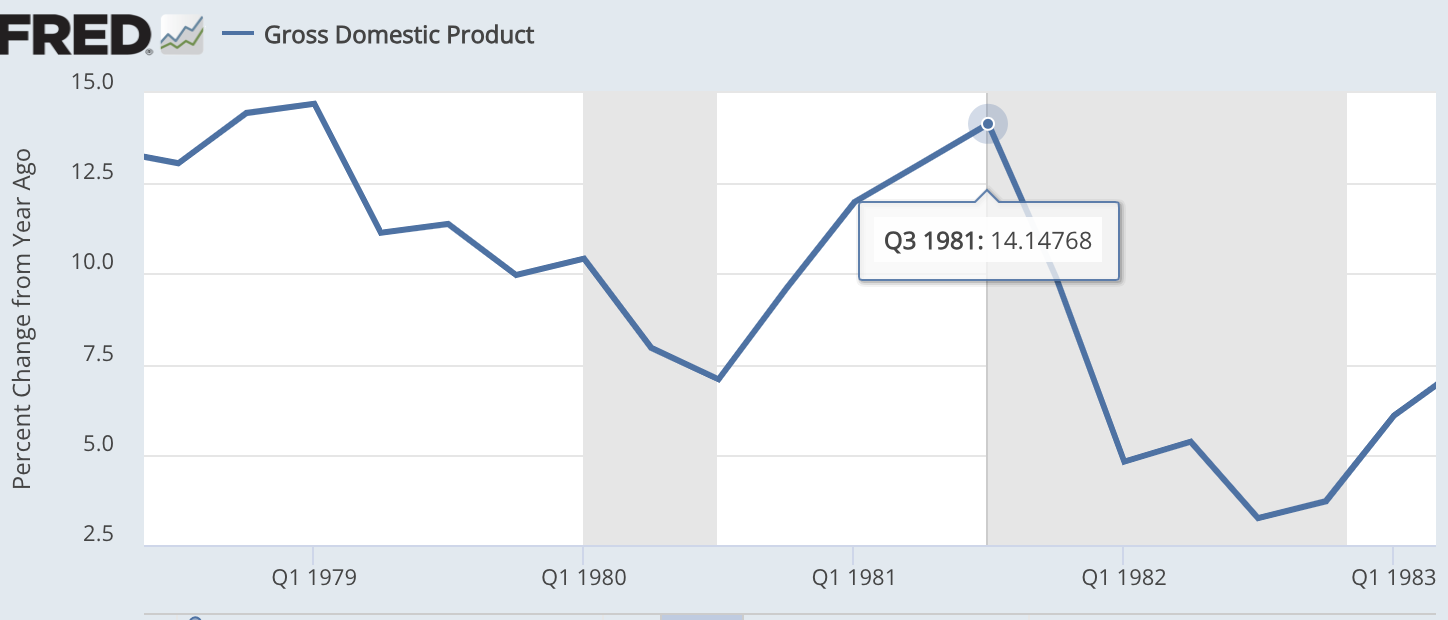

On the other hand, because of wage/price stickiness, short run movements in NGDP and RGDP are often highly correlated in the US. Thus in late 1982, NGDP growth plunged from a peak of 14% to less than 4%, triggering a significant fall in RGDP and high unemployment. While it’s much too soon to declare victory, there’s a real possibility that Jay Powell’s Fed will successfully implement the gradualism program that Volcker’s Fed tried and failed to implement.

[In fairness, Powell was dealt a far easier hand, as by the early 1980s inflation expectations were stuck at double-digit levels and the Fed had lost credibility with the public. This time around, long-term inflation expectations remained fairly low.]

In his Bloomberg piece, Tyler made the following observation:

Krugman has lately further explained his position — complete with unironic headline — suggesting that the untangling of broken supply chains had helped lower the rate of inflation. That point, too, is correct. He didn’t mention that there also has been a massive negative shock to aggregate demand: High rates of M2 growth became slightly negative rates of M2 growth. Fiscal policy peaked and then retreated. The Fed raised interest rates from near-zero levels to the range of 5%, and fairly rapidly. It also sent every possible signal that it was going to be tight with monetary conditions.

I did an Econlog post criticizing his claim that there was a massive negative shock to aggregate demand:

[I]f you’d told economists in late 2022 that we’d have 6% to 7% NGDP growth in 2023, I doubt that very many would have predicted a recession. So the events of 2023 in no way refute the assumption that a sharp slowdown in AD will generally trigger a recession—we failed to have a sharp slowdown in AD.

Notice that I’m equating “aggregate demand” and NGDP growth. Not everyone defines AD in that way, indeed some people derisively call it a “tautological” definition. Well, definitions are tautological, but that doesn’t mean they are not useful.

A few days after I did this post, Tyler posted the following:

Any “very heavy” reliance on real shocks to explain the macro of the last two years has to account for why 2021 had high growth rates, in spite of supply chains then being quite tangled. And why prices haven’t gone back down to their original levels? And what happened to aggregate demand, once the Fed turned its attention to the problem? There simply was a huge, negative AD shock in recent times, at least under any non-tautological definition of aggregate demand. Why didn’t that crush us? Any account needs to address these issues.

Tyler doesn’t mention my name, but given that a few days earlier I had argued that he was wrong about the existence of a “massive negative shock to aggregate demand”, and used the assumption that AD equals NGDP to back up my claim, I felt like his remark might have been directed at my post. After all, “non-tautological definition of aggregate demand” isn’t a phrase you hear every day.

(BTW, I’m inclined to equate “non-tautological definition” with “so vague as to be useless”.)

Over at Marginal Revolution University, Alex Tabarrok summarizes the definition of aggregate demand used in Cowen and Tabarrok’s superb textbook:

You can think about spending growth another way, too. It’s actually the equivalent of nominal GDP growth. If nominal GDP growth is 5%, an AD curve shows all of the possible combinations of inflation and real GDP growth that add up to 5% nominal GDP growth. Likewise, if nominal GDP growth is 7%, the AD curve will show all of the possible combinations of inflation and real GDP growth that add up to 7%, and so on. Increases in the growth rate of nominal GDP shift the aggregate demand curve outwards, whereas decreases shift it inwards.

That sounds pretty tautological to me. And just to be clear, I don’t believe that 2023 saw a massive negative demand shock even using a non-tautological definition of AD.

More than a decade ago, Tyler started a blog post as follows:

Without meaning to take sides in the controversy, I got a kick out of this sentence, which describes the attitudes of contemporary macroeconomists:

Even something anodyne like “demand might also play a role” would come across like the guy in that comic who asks the engineers if they’ve “considered logarithms” to help with cooling.

The blog post, by JW Mason, is interesting throughout.

If you follow the link, JW Mason has a long post, which begins as follows:

People often talk about aggregate demand as if it were a quantity. But this is not exactly right. There’s no number or set of numbers in the national accounts labeled “aggregate demand”

Actually, there is—NGDP.

Mason continues:

Rather, aggregate demand is a way of interpreting the numbers in the national accounts. (Admittedly, it’s the way of interpreting them that guided their creation in the first place). It’s a statement about a relationship between economic quantities. Specifically, it’s a statement that we should think about current income and current expenditure as mutually determining each other.

Now we are back in the world of tautologies:

Gross domestic Income = Gross domestic Expenditure = Gross domestic product

Seriously, when people tell me something is inexpressible, a sort of way of thinking about the world, I’m likely to assume they are referring to some sort of eastern mystical religion, not a branch of economics that is supposed to explain prices, output and employment. Aggregate demand is either total nominal spending, or it’s nothing at all, at least nothing of any use to economists. Given that Mason thinks AD is not NGDP, I can’t criticize him for treating AD like a big joke.

Economics is already full of hard to measure entities, such as the natural rate of interest or the natural rate of unemployment. Let’s not make things needlessly obscure by acting as if AD is not a specific number that can be easily measured.

In the long run, aggregate demand (NGDP) does not matter at all. In the short run, it’s the most important macro variable—explaining almost everything we care about. Why have we had a soft landing so far? Because NGDP growth has slowed gradually. Why has NGDP growth slowed gradually? Because the Fed raised its interest rate target up close the the economy’s natural rate, without overshooting (as it had done so often in the past.). How were they able to do that? I wish I knew. Probably a mix of luck (30 years of Fed credibility plus some positive AS shocks such as a surge in immigration) and skill (more sophisticated reliance of financial market signals and a deeper understanding of the process based on learning from past mistakes.).

But that’s just a guess, and we are not even sure there won’t be a recession in 2024. But there is one thing I can predict with confidence—the performance of the economy in 2024 will be largely determined by the NGDP growth rate. If it’s around 4% by yearend, then we’ll have a soft landing. If it’s around 2%, we’ll have a recession. If it’s around 6%, we’ll have resurgence in inflation.

Looking out over the next few decades, NGDP won’t matter much at all—the performance of the economy will depend on real factors such as the impact of AI.

HT: Commenter JP reminded me of the Cowen and Tabarrok textbook.

READER COMMENTS

Kevin Erdmann

Jan 27 2024 at 5:15pm

I wrote about this in my most recent substack post.

I argue a few things. Among them:

1) there is a sustainable 5% NGDP growth path. There hasn’t been a decline in trend. There was a one-time GDP shock of about 11% after 2008. That was actually unsustainable because residential investment can’t stay that low. Real per capital housing expenditures were declining. We’ve been back to a roughly 5% NGDP trend since residential investment got back up to what would have previously been considered recessionary levels. Using that trend from 2016, post-covid NGDP hasn’t significantly overshot.

2) we still haven’t even started to recover from the covid-related residential investment supply shock. Real residential investment is still at pre-Covid levels and the input price spike hasn’t reversed at all. There is still a lot of room for a correction of above average real growth and below target inflation. The housing supply shock still has to unwind. Eventually if it is allowed to, it will feed into rent disinflation which will also help boost the long term sustainable NGDP trend.

3) also, I note that the Fed target rate was still at zero several quarters into the glide path of declining NGDP growth. So arguing for tighter policy in 2021 and 2022 is an argument for pushing harder (a la Volcker) on the path correction. I had complained in late 2022 that the Fed was hiking too much, and I have conceded that Powell probably had it right, in hindsight. You have argued that they were too loose, and I wonder if you, like me, have come around to being more favorable of Powell’s choices.

https://open.substack.com/pub/kevinerdmann/p/december-2023-new-home-sales-and?r=2pxsw&utm_campaign=post&utm_medium=web&showWelcome=true

Scott Sumner

Jan 27 2024 at 11:51pm

No, I still think money was too loose in 2021 and 2022. The economy overheated and there was a severe shortage of workers. Somewhat slower NGDP growth would have meant lower inflation without much effect on the unemployment rate.

I hope you are correct about 3% trend growth in RGDP, but I’m skeptical. The trend rate has been well below that figure in recent decades. Perhaps AI will help. Time will tell.

Kevin Erdmann

Jan 28 2024 at 4:29pm

Well, one of my points is that 3% RGDP growth may not take anything special. In June 2022, the unemployment rate was 3.6%. We now have 6 quarters of 3% RGDP growth since then.

The question I ask in the link is, if this continues, how many more quarters or years will it take to consider 3% the neutral target?

Scott Sumner

Jan 29 2024 at 10:43am

You need at least one complete business cycle to estimate trend RGDP–preferably several.

Kevin Erdmann

Jan 29 2024 at 12:25pm

Isn’t that another reason to stick with the 5% NGDP trend that goes back 30 years, except for the anomalous 2008-2012 period?

Michael Sandifer

Jan 27 2024 at 5:45pm

I want to add to Kevin’s points. Real GDP has trended up over the past two years, even as NGDP has declined, as you noted. This is due, in part, to healing on the supply side of the economy. This healing continues, and still has room to run. Here’s a look at commodity prices, which are still more than 50% their pre-pandemic levels, for example:

https://tradingeconomics.com/commodity/crb

Of course, monetary policy did get too loose for a while, and the Fed has brought aggregate demand down, which has helped lower inflation rates. But, many “transitory” factors were and continue to be at work also. I continue to argue that it seems you’ve underestimated the role of supply-side factors in contributing to and reducing inflation.

As important as looking at NGDP versus it’s long-run trend is, it is not determinative. I see it as a big red arning light on a dashboard, but even it cannot be taken to be definitive in isolation.

Scott Sumner

Jan 27 2024 at 11:54pm

I’ve always agreed that supply factors have contributed to moves in headline inflation. But when people say it’s painful to bring inflation down, they are referring to the demand side part of inflation, which has fallen by much less than the headline figure. That’s the part of the change in inflation that is affected by NGDP.

Michael Sandifer

Jan 27 2024 at 5:46pm

I meant to type that commodity prices are still more than 50% above pre-pandemic levels. That is also not definitive, but it is potentially a clue.

Jim Glass

Jan 28 2024 at 12:09am

No disagreement as to today’s world. But as to gradualism in 1981, I was studying Econ at NYU/Stern then with Profs from across the street at the NY Fed, and recall the Fed’s breaking of inflation then not as failed gradualism but much more an overt exercise in “shock and awe” knowing the pain was coming. I recall then as the high water mark of Friedman’s monetarism, the Profs being serious Friedman-Volckerites, and the whole atmosphere being “whip inflation now“, not gradually — which they had been trying and failing for years (most recently with the 1980 Volcker backoff under Carter). But my memory is failing, so…

Checking the data, from June ’80 to May ’81 the 3-month T-bill rate went from 7.1% to 16.3% as the PCE fell from 9% to 8.2% — so that real interest rate went from -1.9% to +8.1% in less than a year. That’s up 10 full points. The prime rate went from 11.5% to 20.5%. I don’t remember anyone thinking that was gradual, or heading for a soft landing.

My memory is that Volcker in his book said they knew things would get tough and Reagan’s advisors tried to stop him but Ron said: do what needs to be done. But my copy is in storage so I looked for quotations online. On your blog, here is you quoting me citing Volcker’s book Better than that, I just found a much earlier discussion here at Econlog that links to Volcker being interviewed by PBS…

Read the whole thing.

Scott Sumner

Jan 29 2024 at 10:46am

Part of the problem is that the Fed flipped from tight money in early 1980 to easy money in late 1980 to tight money in the spring of 1981. That made it harder to implement gradualism

Arqiduka

Jan 28 2024 at 4:14am

Unproven but I’d still like to throw it out there: the way to curb inflation without causing a recession is to *lower* interest rates whilst at the same time buying back as much base currency as the market wants to sell at the new rates. Requires huge reserves, thus in practice you fall back to gradualism.

Matthias

Jan 28 2024 at 10:20pm

How do you lower interest rates?

Typically that’s done by the central bank buying lots of government debt with newly created money.

So you are suggesting to inject money into the economy, but then also to take it out somehow?

At least that’s interpreting your suggestion as short run measures.

As Scott likes to argue, you can also bring interest rates down in the longer run with tight money. So first the central bank sells lots of government debt, which removes money from the economy and raises the interest rates. Then in the longer run inflation drops and interest rates drop, too. But the central bank selling government bonds to fight inflation is as close to old-time orthodox policy as one can imagine.

Arqiduka

Jan 29 2024 at 4:09am

Why, exactly.

You buy back debt, and sterilize the emissions by buying it back against reserves.

Basically, you buy back local debt with foreign currency.

spencer

Jan 28 2024 at 1:56pm

The 1982 recession was precipitated from the DIDMCA of March 31st 1980 and the imposition of reserve requirements against NOW accounts in April 1981.

2023’s growth was driven by a change in the composition of the money supply.

Matthias

Jan 28 2024 at 10:23pm

Scott, I would have expected a lot more talk about expectations from you on this subject?

If the central bank credible announces that they are going to bring inflation (or ngdp growth) down from eg 10% to 2% over three years, wouldn’t expectations make that announcement effective right away, even if the planned path of policy was gradual? (Or even more extreme, even if actual policy only changed at the end of the three years?)

Scott Sumner

Jan 29 2024 at 10:48am

The problem is that these sorts of announcements are often not very credible. But yes, I agree that expectations matter, and the Fed’s credibility this time helped Powell do better than Volcker.

Michael Sandifer

Jan 28 2024 at 10:32pm

The Fed Funds futures curve has rates dropping down to near 3% until 2026, and then rising thereafter. This could mean that growth is expected to be back down to around pre-pandemic rates until 2026, and then will rise. This may reflect the expectation of an AI-related J-curve, with the boom beginning in 2026.

This strongly suggests that mean RGDP growth will be higher than the pre-pandemic rate for the foreseeable future.

Philippe Bélanger

Jan 29 2024 at 3:57am

There is something very circular about assuming a value for NGDP growth when drawing an aggregate demand curve. In microeconomics, the point of a supply and demand analysis is to show that both curves, which are independent of what happens in equilibrium, determine price and quantity (and therefore nominal spending). The way Cowen and Tabarrok go about it, we begin by assuming the equilibrium value of NGDP growth, then use that value to draw the AD curve (the AS curve is presumably a behavioural relationship) and the intersection of both curves gives us the equilibrium state of the economy. But this model can’t explain why NGDP growth has the specific value it has in equilibrium; it just assumes it.

Such a model is useful if the central bank successfully targets NGDP growth. In that case, we have a good reason to assume that NGDP growth is constant along the AD curve and we can use the NGDP target to draw out the AD curve. But under a different regime, especially one where NGDP growth varies considerably over time and we want to explain this variation, this approach isn’t useful because it can’t explain in a non-circular way why NGDP growth takes on a specific value. In order to explain NGDP growth in a non-circular way, you need a model where both curves are behavioural relationships that are independent of the equilibrium of the model.

Scott Sumner

Jan 29 2024 at 10:53am

I agree that when the central bank is not targeting NGDP then you want to model the way NGDP is determined. For instance, I did a book on the role of gold market shocks during the 1930s—entitled The Midas Paradox.

But even in that case, movements in NGDP can be viewed as demand shocks, albeit ones that were not caused by the central bank.

Philippe Bélanger

Jan 29 2024 at 5:09pm

I agree you can always draw a hyperbolic AD curve and view changes in NGDP as demand shocks, however I think it’s important to realize that if you do this, your model (or rather the model that is implied by the AS-AD diagram you draw) doesn’t explain changes in NGDP. The value for NGDP must come from somewhere else (say, an analysis of the gold market). But I have to admit that I don’t really see the point of drawing such a diagram. The only case where I would do this if I thought that NGDP was determined independently of the AS curve. Then the AS curve only determines the decomposition of NGDP into the price level and real output. The only situation I can think of in which this is true is an economy where the Fed always hits a NGDP target.

Gregory A Pakela

Jan 29 2024 at 9:50am

Scott, as someone who like myself was a young adult from the time that Paul Volcker was appointed by President Carter in the waning days of his administration, you should be well aware that the Volcker Fed was anything but gradual in raising the Fed funds rate to 20%. At the time the Fed had ostensibly bought into the monetarist policy framework and attempted to control the rate of growth in the money supply. This caused a massive increase in interest rates at the very short end with an inverted yield curve that led to a very steep recession, actually a compound recession in my view. Volcker eventually abandoned strict monetarism, but even as he dramatically reduced the Fed funds rate, it was still extremely high in real terms. The Volcker Fed did succeed in a gradualist approach in the mid 1980s by once more raising the Fed funds rate, and this did not result in a recession, but merely a pause in economic growth. The 1991 recession was also characterized by a Fed tightening cycle, but may have been triggered by the first Gulf war and the attendant increase in the price of oil. The gradualist approach was perfected by the Volcker and Greenspan Feds, unlike the Martin Fed of the 1950s where tightening cycles led to frequent recessions. Perhaps the Fed is more successful now because the modern economic is more market oriented than it was in the early post-war era.

John Hawkins

Feb 1 2024 at 2:14pm

To perhaps disentangle you and Tyler’s disagreement: Do we have any idea why money Velocity seems to have increased so much? Do we really understand anything about Velocity?

Comments are closed.