In recent months, we’ve seen an almost endless series of opinion pieces discussing the supposed “mystery” of why tight money has failed to slow the economy. Yet almost no one seems to question the assumption that a tight money has been adopted in the US and elsewhere. In this post, I’ll show that there is no mystery to be explained; the economy is reacting today as it has always reacted.

Today’s Financial Times provides a good example of the media’s confusion:

Monetary policy always comes with a lag, taking about 18 months for the impact of a single rate increase to fully seep through into spending patterns and prices.

Monetary policymakers began raising rates less than a year and a half ago in the US and UK, and less than a year ago in the eurozone. They went higher than the neutral rate — where they are actively restricting the economy — only a few months ago.

But some central bankers and economists believe lags may be even longer — and the effect of the tightening less potent — this time around.

“Maybe monetary policy is not as powerful as it was several decades ago,” said Nathan Sheets, chief economist at US bank Citi.

There is a much simpler explanation. Interest rates do not show the stance of monetary policy. Policy was not tightened in 2022; indeed it remained quite loose. When policy does get tight, the effects will be almost immediate. Here’s a point I cannot emphasize enough:

Interest rates are a procyclical variable.

A long-term shift away from manufacturing towards services, which require less capital, could also mean slower transmission of a tighter monetary policy.

Just the opposite is true. In an economy that requires less capital, the neutral interest rate is lower. Any given policy rate then implies tighter money. Indeed this may help explain why the neutral rate fell to such low levels in the 2010s.

Structural changes in important parts of the economy — including housing and labour markets — between now and the 1990s may explain why rate rises had a much snappier and sharper impact then.

I’m afraid the FT has misremembered the 1990s. Interest rate increases did not have a “snappier and sharper impact” back then:

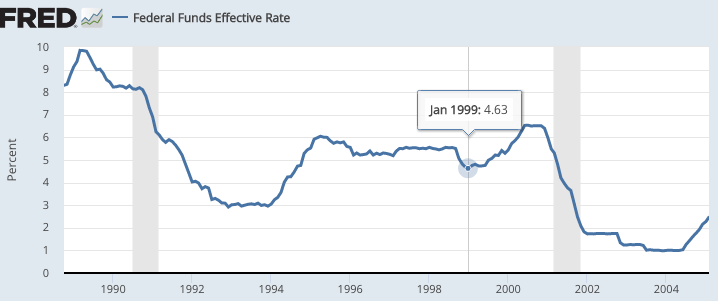

Notice that there were two periods of rising rates during the 1990s. The sharpest occurred in 1994, and not only was its impact not “snappier and sharper”, it had almost no impact on the long 1990s economic boom. Inflation was 2.6% in 1994, 2.8% in 1995, and 2.9% in 1996. (It slowed in 1997 due to the East Asia crisis, not anything the Fed did.)

The second period of rising rates began in January 1999. A full two years later the economy was still not in recession. In contrast, we are less than 18 months into this tightening cycle.

No, there was no Golden Age when rate adjustments explained macroeconomic trends. The Fed enacted many rate increases between 1965 and 1981, and yet inflation rose higher and higher. Sharp rate cuts in 1929-30 failed to arrest the severe deflation of 1929-33.

How can we learn from history if we don’t even know the facts? There’s never been a close correlation between interest rates and the macroeconomy. Interest rates are not monetary policy.

PS. I wrote a whole book on the subject. It’s free.

READER COMMENTS

Casual Observer

Jul 4 2023 at 3:15pm

As far as I understand, the FED has three tools to work with: interest rates (IR), forward guidance, and QE. If I am understanding you correctly, IR has minimal (if any) impact on the macroeconomy, so what about the other two? Is it possible that all three on their own have little to no impact but when taken as a whole the impact is larger? By impact I mean a greater ability to slow/speed up the economy and ultimately be reflected in macro trends.

Note: I have your free book downloaded and on my shelf. Haven’t read it yet though! Either way thanks for making it accesible to the masses!

Don Geddis

Jul 8 2023 at 2:19pm

Monetary policy got more complicated after 2008 (with IOER, Interest on Excess Reserves), and there are always subtle points like the difference between direct purchases of bonds, vs. Overnight Reverse Repurchase Agreements (“repo”). But those are all minor details.

The easiest, clearest, model of monetary policy, is that the Fed has only one single tool: the quantity of money. (And, therefore, the central bank is only capable of targeting one single goal!)

Everything that you mention (interest rates, forward guidance, QE) is merely an expression or consequence of this one tool. It is all, only, about the money supply. There is nothing else. (Please note, for example, that the Fed does not set interest rates — at least, not the all-important Federal Funds Rate — it only targets interest rates. And it achieves these targets by … adjusting the money supply.)

spencer

Jul 4 2023 at 4:31pm

re: “When policy does get tight, the effects will be almost immediate.”

Spot on. Powell, like Volcker, is just letting the economy burn itself out. Powell more concerned with a soft landing, than tackling inflation. Powell didn’t tentatively start QT until June 1, 2022, @47.5b after inflation had already peaked. It didn’t increase that figure until September @95.b three months later. And it reversed course in 2023 before getting back on track.

Assets: Total Assets: Total Assets (Less Eliminations from Consolidation): Wednesday Level (WALCL) | FRED | St. Louis Fed (stlouisfed.org)

The FED should let the markets set interests rates. Interest is the price of credit. The price of money is the reciprocal of the price level.

The proper way to combat stagflation, business stagnation accompanied by inflation, is the 1966 Interest Rate Adjustment Act.

It is not the way history unfolded:

Bigger, Fewer, Riskier: The Evolution of U.S. Banking Since 1950 – The American Interest (the-american-interest.com)

Scott Sumner

Jul 4 2023 at 5:13pm

Casual observer, You said:

“If I am understanding you correctly, IR has minimal (if any) impact on the macroeconomy,”

No, I’m saying something slightly different. All three tools that you mention can have an impact. A given change in rates may or may not have an impact on the economy, it depends on other factors such as the neutral interest rate, which also changes over time. If the Fed raises rates by 100 basis points at a time when the neutral interest rate has risen by 100 basis points, then the stance of policy has not effectively changed.

The Fed clearly has the ability to impact aggregate demand (NGDP). It’s just that interest rates don’t tell us much about the current stance of policy.

Thomas L Hutcheson

Jul 5 2023 at 4:52pm

So what? Just don’t talk about “stance,” just talk about what in your opinion the settings of any or all policy instruments should be.

Scott Sumner

Jul 6 2023 at 1:04am

I’d like to see a NGDP level target, at roughly 3.5% or 4.0% growth. Commit to return to the trend line.

I don’t know what the Fed is trying to do now, so I can’t tell them what interest rate setting to have.

Francis Quinn

Jul 6 2023 at 4:54am

Scott is saying that what matters is the objective being targeted by the Fed.

Their tools help them achieve an objective.

They can achieve any (nominal) objective they want.

It’s unclear what objective they’re targeting.

They should make the objective they’re targeting explicit, and take it extremely seriously, and try their hardest to use their tools to achieve that objective.

Michael Sandifer

Jul 4 2023 at 10:04pm

Is it safe to say the following is a misstatement? “Policy was not tightened in 2022; indeed it remained quite loose.”

Did you mean to say that policy did not become tight in 2022? By any measure, policy tightened in 2022, as NGDP growth began to fall, as did inflation and inflation expectations.

Scott Sumner

Jul 5 2023 at 1:42am

But NGDP moved further and further above the trend line in 2022. The fast NGDP growth of 2021 was partly an appropriate return to trend. In 2022 it was an inappropriate overshoot of trend.

You can debate the degree of looseness, but certainly policy was loose in 2022. The media told us it was tight.

Michael Sandifer

Jul 5 2023 at 2:49pm

Yes, if one accepts NGDP level targeting as an appropriate framework, which I do, and if one agrees with your trend baseline, which I don’t. That said, I agree that policy was probably too loose for a time in 2022. I base that on breakevens having been considerably above 2%, in core PCE terms.

I still think you’re underestimating the persistence of supply-side factors driving inflation. The Ukraine war and new US industrial policy haven’t ended, China’s economy still isn’t fully back-on -track, US supply chains are still being repaired and re-routed, and we still have some weakness in the US commercial banking sector.

Thomas L Hutcheson

Jul 5 2023 at 4:57pm

“The media told us it was tight.”Again. The error is in trying to give the right name to the “stance” of the Fed. The question ought to be what to do at the next meeting of the FOMC

Scott Sumner

Jul 6 2023 at 1:05am

No, the question is what target should they shoot for?

Thomas L Hutcheson

Jul 5 2023 at 7:15am

There is not much of a mystery because Fed policy HAS reduced inflation. Now, it is true that some folks are disappointed that inflation has come down without a recession, that Democrats (but not Republicans) may not be punished for large deficits, but sorry. But look at the TIPS rates and tell me Fed policy did not change in March 2022!

vince

Jul 5 2023 at 4:11pm

Inflation is reduced but it’s still too high.

Who is disappointed that we don’t have a recession? Those who want a recession in order to break inflation?

Good point.

vince

Jul 5 2023 at 4:12pm

Formatting on this blog is horrible. My post had three bullet points before I submitted. They disappeared.

David S

Jul 5 2023 at 7:33am

I concur with Spencer’s observation about Powell letting things run their course. The inflation spike of ’21 and ’22 was annoying but not a calamity. The Fed’s abandonment of FAIT does hurt their credibility, but most people have short memories. If we end this year with NGDP at 5.5% then we’ll be in a good place, and if 2024 resembles 1995 then the good times will be rolling—although a bit slower.

Do we want Powell to be Greenspan during the 90’s or Bernanke during 2005-2010?

Scott Sumner

Jul 5 2023 at 12:25pm

Keep in mind that when Greenspan brought inflation down from 4.5% to 2%, there was a recession (in 1991.)

Volcker faced much higher inflation/NGDP growth.

spencer

Jul 5 2023 at 8:02am

Financial Times – As Sheila Bair said: “It should replace the shock and awe of major interest rate hikes with new targets based on money supply, and aggressively shrink its portfolio, selling securities at a loss to do so, if necessary.”

Thornton: “the interest rate is the price of credit, not the price of money”

“Today “monetary policy” should be more aptly named “interest rate policy” because policymakers pay virtually no attention to money.”

link Daniel L. Thornton, Vice President and Economic Adviser: Research Division, Federal Reserve Bank of St. Louis, Working Paper Series

“Monetary Policy: Why Money Matters and Interest Rates Don’t”

The distributed lag effect of money flows, the volume and velocity of our “means-of-payment” money supply, are mathematical constants. Powell’s policy has nothing to do with the peak in the inflation indices (“Year-over-year CPI peaked at 9.1% in June”).

spencer

Jul 5 2023 at 8:46am

“The figure shows that market rates have nearly always led changes in the Fed’s federal funds rate target over the period. To me and others this suggests the Fed has been following interest rates up and down”

The Effect of the Feds Target on Interest Rates A Clarificatioin.pdf (dlthornton.com)

John Hall

Jul 5 2023 at 9:05am

I agree with you on interest rates as a stance for monetary policy, but have you been paying attention to forward-looking nominal GDP growth forecasts?

The one-year ahead nominal GDP growth forecast from the Survey of Professional forecasters is 3.6%. It had a recent high of 7.1% in Q2 2021 and has been trending lower since then.

In other words, experts are expecting a roughly trend (or maybe a tad below trend) pace of nominal GDP growth over the next year.

If you were in charge of the Fed, would you declare victory and just follow through with already signaled rate hikes for this year, or would you recommend they keep hiking so as to bring the level of nominal GDP back to pre-COVID trend*? I think I know the answer for what you would prefer (level targeting, though probably over a longer period).

I think this becomes a very big issue for your NGDP level targeting. I suppose it was why others invented hybrid systems that were similar but let bygones be bygones for past inflation.

* By my calculation, we are 8.75% above the pre-COVID log trend in nominal GDP. If we have one year of 3.6% nominal GDP growth, we will be above the trend by 8.3% in a year.

Scott Sumner

Jul 5 2023 at 12:35pm

“I think this becomes a very big issue for your NGDP level targeting.”

The point that people keep missing is that if we’d had a credible NGDP level targeting regime in place in 2021 then we never would have arrived in this predicament in the first place. If we have a recession (and they are hard to predict), it will likely be a completely unnecessary recession.

I don’t like to recommend specific levels for interest rates, because it depends on the monetary policy regime. I’m not sure what the Fed is trying to do.

I will say that a 3.6% NGDP growth rate would be an acceptable outcome to me, so I hope the forecasters are right. Last year they were wrong.

Thomas L Hutcheson

Jul 5 2023 at 5:05pm

Let’s suppose the Fed has a FAIT with the F being to get expectations back to 2% PCE as fast as possible w/o causing a recession. What should it do?Or suppose that the Fed targets what you think it should target. What should it do? Or should have done when?

Scott Sumner

Jul 6 2023 at 1:07am

It should have been tighter in the past. Today, a rate of 3.5% or 4.0% NGDP growth would be acceptable going forward.

John Hall

Jul 6 2023 at 9:20am

I actually meant to add a reply to my comment before I saw yours that addressed this point, but it got eaten by my corporate firewall.

There are basically two parts to this:

1) Should an optimal Fed policy ignore past inflation when it is above the target? (i.e. let bygones be bygones)

2) Given that the Fed’s monetary policy regime previously allowed inflation to go above its target, should the Fed adopt a new monetary policy regime that incorporates the past inflation spike?

I think 1 is a difficult question that many people would disagree about.

On number 2, I think anytime a central bank adopts a new regime, they are going to have some transition period that they will need to think carefully about. If economy went into a tailspin, then the Fed wants to adopt nominal GDP level targeting, then it makes sense to include the past real shock, rather than starting the level calculation on Day 1 (and excluding the past). For inflation, I think it’s a bit trickier, but I think it would probably be a mistake for the Fed right now to tighten policy sufficiently to restore NGDP to its pre-COVID trend. It reminds me of the aftermath of WW1 and countries trying to go back on the pre-War gold standard at the same price as before the war.

Bobster

Jul 7 2023 at 12:30am

The survey of professional forecasts has underestimated inflation the past couple years.

Data doesn’t seem to indicate slowing

Grand Rapids Mike

Jul 5 2023 at 10:53am

It seems what is forgotten is that the Fed increased M2 by about 40% from March 2020 to December 2022. Since then there has been only a minor decrease in M2,. Consequently still of lot of excess M2 out there seeding inflation etc.

vince

Jul 5 2023 at 4:07pm

Thanks for the book, Scott. It helps to explain your view on interest rates. If I read it correctly, you’re not necessarily saying that interest don’t reflect monetary policy. You’re saying it depends on interest rates relative to an unknown equilibrium rate, and the distance from the equilibrium rate is inferred from observed outcomes such as prices. But isn’t that exactly what the Fed is doing–raising short term rates and observing the effect on outcomes such as inflation, unemployment, and NGDP?

Scott Sumner

Jul 6 2023 at 1:08am

The problem is that the Fed lacks a clear policy target. They promised an average inflation rate of 2%, then reneged on the promise.

marcus nunes

Jul 7 2023 at 6:12am

Interest rates and the economy over the past three decades:

https://marcusnunes.substack.com/p/when-monetary-policy-tightening-is

marcus nunes

Jul 7 2023 at 6:41am

Since early 2022, also for the first time in 30 years, an increase in the Fed Funds rate has been “consistent” with monetary policy tightening! My “cynic side” will conjecture that, since the steep increase in the FF rate took place in an environment of “true” monetary tightening , its effect was mostly to produce a banking crisis! (In 2008, the financial crisis happened in an environment where the FF rate was dropping BUT monetary policy was EXTREMELY tight. At the present time, monetary policy is “only” being gradually tightening).

When monetary policy “tightening” is not what you think (substack.com)

spencer

Jul 7 2023 at 8:48am

QE was made possible in 1965 when reserve requirements were removed from interbank demand deposits at the FED for member banks.

That’s what propelled the “Great Inflation”.

You can blame Paul Volcker for QE:

Paul Volcker was quoted in the WSJ in 1983 that the Fed: “as a matter of principle favors payment of interest on all reserve balances” … “on rounds of equity”. [sic]

Interest is the price of credit (bank credit, plus nonbank savings). The price of money is the reciprocal of the price level (based on specialized price indices).

Waller, Williams, and Logan seem to agree. They “believe the Fed can keep unloading bonds even when officials cut interest rates at some future date.”

The FED should cut interest rates now, and continue with QT. The 1966 Interest Rate Adjustment Act is prima facie evidence.

The only interest rate inversion that didn’t produce a recession was back in 1966. Then, the 1966 Interest Rate Adjustment Act lowered commercial bank deposit rates. This activated monetary savings, increasing velocity while decreasing money growth.Whereas time deposits were 105 percent of demand deposits in July, by the end of the year, the proportion had fallen to 98 percent. These were all desirable developments.

”M1 peaked @137.2 on 1/1/1966 and didn’t exceed that # until 9/1/1967. Deposit rates of banks, Reg. Q ceilings, decreased from a high range of 5 1/2 to a low range of 4 % (albeit not enough). A .75% interest rate differential was given to the nonbanks. And during this period, the unemployment rate and inflation rates fell. And real interest rates rose.

Today we have the inverse situation, the remuneration rate on IBDDs is higher than long-term interest rates.

The FED’s Ph.Ds. have learned their catechisms.

spencer

Jul 7 2023 at 8:58am

The short-term rate-of-change in American Yale Professor Irving Fisher’s “equation of exchange”, the proxy for the real-output of goods and services (the distributed lag effect), bottoms in June.

So, without additional QT, there shouldn’t be a recession call in 2023.

See: “History and forms. Irving Fisher (1925) was the first to use and discuss the concept of a distributed lag. In a later paper (1937, p. 323), he stated that the basic problem in applying the theory of distributed lags “is to find the ’best’ distribution of lag, by which is meant the distribution such that … the total combined effect [of the lagged values of the variables taken with a distributed lag has] … the highest possible correlation with the actual statistical series … with which we wish to compare it.”

Thus, we wish to find the distribution of lag that maximizes the explanation of “effect” by “cause” in a statistical sense”. And “The Lag from Monetary Policy Actions to Inflation: Friedman Revisited” 2002 “We reaffirm Friedman’s result that it takes over a year before monetary policy actions have their peak effect on inflation… Similarly, advances in information processing and in financial market sophistication do not appear to have substantially shortened the lag”

“At the Dec. 27–29, 1971, American Economic Association meetings, Milton Friedman (1972) presented a revision of his prior work on the lag in effect of monetary policy (e.g. Friedman 1961). His new conclusion was that ‘monetary changes take much longer to affect prices than to affect output’; estimates of the money growth/CPI inflation relationship gave ‘the highest correlation… [with] money leading twenty months for M1, and twenty-three months for M2’ (p. 15)”

spencer

Jul 7 2023 at 9:06am

Link: Daniel L. Thornton, May 12, 2022:

“However, on March 26, 2020, the Board of Governors reduced the reserve requirement on checkable deposits to zero. This action ended the Fed’s ability to control M1.”

Now we are lost without a rudder or an anchor.

As I said in response to Powell removing legal reserves: “The FED will obviously, sometime in the future, lose control of the money stock.” May 8, 2020. 10:38 AMLink

Comments are closed.