Over at TheMoneyIllusion I have a new post that (among other things) discusses this claim:

Blanchard was prompted to recite his faith in the power of the Phillips Curve by former Fed governor Jeremy Stein, who wondered how central banks were supposed to raise their inflation target to 4 per cent when they are still undershooting the current target of 2 per cent. Blanchard seemed to think the answer was easy: keep rates low, unemployment will fall, and inflation will necessarily accelerate.

Larry Summers — Blanchard’s co-host at the conference and co-author of one of the papers — found this hopelessly inadequate. He pointed to Japan’s long experience with full employment, large government budget deficits, aggressive monetary expansion…and total price stability. If they haven’t managed to get inflation, how could anyone? Blanchard had no answer but to repeat his catechism.

I point out that this is a very strange assertion, as the Fed is currently engaged in raising interest rates with the express purpose of holding down inflation. They fear that if they don’t raise rates, then inflation will overshoot 2%. That may be wrong, but inability to raise inflation has nothing to do with current Fed policy.

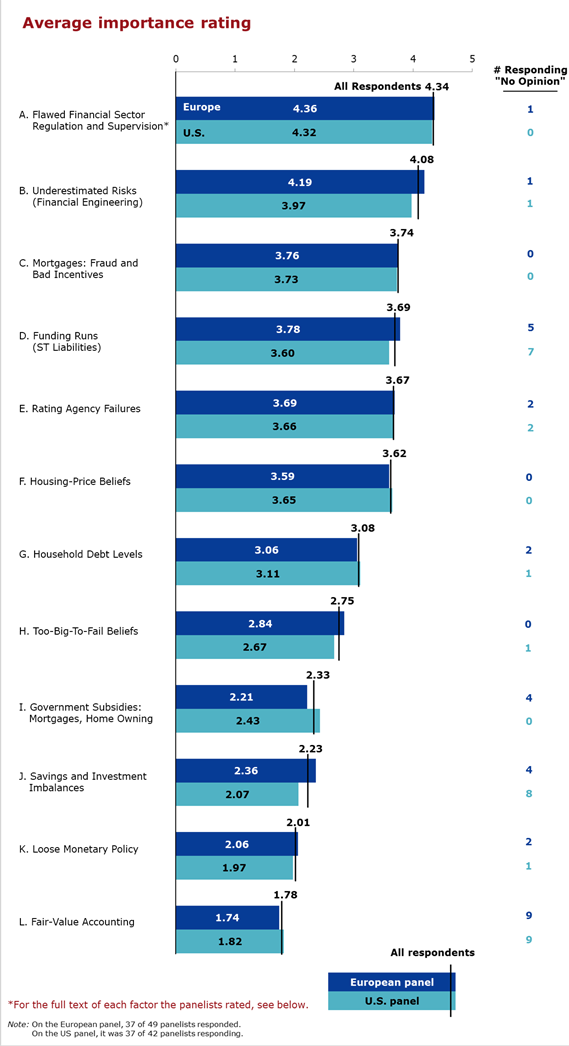

Caroline Baum sent me an equally maddening survey of elite economists, conducted by the University of Chicago. The survey asked them to rate the relative importance of 12 different factors in the 2008 financial crisis. For some strange reason “tight money” was not even mentioned, despite the fact that 2008 saw a steep plunge in NGDP growth, and we were not even at the zero bound. Those stylized facts are almost a textbook definition of a tight money policy reducing aggregate demand, and yet this hypothesis was so far off the radar screen that it wasn’t even mentioned as an option.

Modern macroeconomics doesn’t just have the wrong answers, we are not even asking the right questions.

It occurs to me that Stein’s strange claim about monetary policy ineffectiveness and the UC’s glaring omission in their survey have a common root explanation—a belief in central bank infallibility. Of course I’m exaggerating a bit, I’m sure most economists don’t actually view the Fed as infallible, but bear with me for a moment.

Suppose it were true that central banks adopted polices that were right in the mainstream, close the consensus of elite macroeconomists. In that case, it would be natural to view any policy mistakes as not resulting from “monetary policy shocks”, but rather from other “exogenous shocks.” Most elite macroeconomists thought that Bernanke’s Fed adopted sensible policies during 2008, so they naturally viewed the bad outcome as resulting from some sort of other factors.

In one sense, this is not particularly surprising. I have enormous respect for Ben Bernanke, who was a highly skilled central banker. Thus one’s first reaction is not to view the Fed as an out of control rampaging elephant, causing also sorts of harm to the economy. Rather at first glance it seems more like a medical doctor, trying with varying success to cure the ills of the macroeconomy.

This “infallibility” view is further strengthened by the widespread tendency to misdiagnose low and/or falling interest rates as easy money. Since rates fell sharply in 2008, that made economists even less likely to blame the Fed.

And I think Stein is making the same sort of mistake. He sees central banks like the Fed continually undershooting their inflation target. He also has enormous respect for the competence of the Fed. (Heck, he used to work there.) Therefore instead of blaming the Fed for the undershoot, he looks for macro models where there is literally nothing the Fed can do to raise the inflation rate.

While this is very understandable from one perspective, from another it is very, very strange. Consider:

1. It’s very odd for social scientists to make policymaker infallibility a central axiom of their core theoretical model. That’s the sort of blind faith you’d associate with uneducated voters sticking with a charismatic but demagogic politician despite numerous well-documented failures. Scientists are supposed to be skeptics–always looking to improve their models.

2. It’s not just me who thinks the Fed is not trying to raise inflation right now, virtually everyone agrees that the Fed is raising rates with the express purpose of holding down inflation. This isn’t some sort of weird market monetarist claim, it’s generally accepted by everyone. So why assume that policy is ineffective?

3. Many economists blame the Fed for the Great Contraction, despite the fact that the Fed cut rates to very low levels and also did QE. That perception of 1929-32 may or may not be true, but given that the stylized facts were quite similar in 2008, why is it not even being contemplated as a hypothesis? Why not at least ask economists if the Fed might have made the same mistakes (to a much lesser degree) in 2008 as in 1929-32, given that the stylized facts were so similar? What is the specific data point that you’d cite to argue that the tight money theory of the Great Recession is not even worth investigating? I don’t get it.

4. Before the Great Recession, Western economists blamed the Japanese central bank for the persistent deflation in Japan. Why is the Fed viewed as infallible, but not the BOJ?

The widespread assumption that the Fed could not possibly have caused the Great Recession is now actually distorting macro theory. It’s causing economists to abandon solid well-established New Keynesian theories, and seek out more dubious fringe ideas, such as non-monetary theories of inflation and NGDP growth.

HT: Kevin Erdmann

READER COMMENTS

Mark Bahner

Oct 19 2017 at 5:28pm

Hi Scott,

Good stuff again…here and at TheMoneyIllusion. This is really basic and incredibly important stuff, so it’s really shocking and scary how far off people seem to be.

You write:

I do note that they mention “Loose Monetary Policy” (my italic). And it should at least give you comfort that it was near the bottom in importance. 😉

It would be very interesting to hear from those economists about what they were thinking about that particular aspect…”loose monetary policy.”

On the other hand, I guess another way of looking at it is that the absence (my italic again) of “loose monetary policy” was hugely important.

BC

Oct 19 2017 at 6:36pm

“It’s causing economists to abandon solid well-established New Keynesian theories, and seek out more dubious fringe ideas, such as non-monetary theories of inflation and NGDP growth.”

Are we sure that the cause and effect are not reversed? Perhaps, some folks favored more fiscal expansion, financial regulation, etc. even before the Great Recession. If the main cause of the Great Recession was monetary policy, then the Great Recession does not provide a justification for those other non-monetary policies. So, when people create stories for why the Great Recession is a good argument for those other policies, then those stories naturally exclude monetary policy as a cause of the Great Recession.

Thomas Sewell

Oct 19 2017 at 8:43pm

There is a significant bias in American academic quarters toward central policy solutions. Someone would need to overcome that bias towards the Fed before they could cognitively consider Fed actions may sometimes be the problem and not the solution, to paraphrase an early 80s U.S. President.

Jeff

Oct 20 2017 at 8:19pm

It’s not that the Fed is infallible, it’s just that they’re never to blame for anything. Except for the Depression, and that was not acknowledged until long after the people who worked there back then had long since retired. The First Law of Bureaucracy is still: Above all, avoid accountability.

So inflation and deflation are never the result of monetary policy. They just happen, and the heroic Fed staff is always fighting one or the other.

You would think eventually we would wise up.

Comments are closed.