This set of twitter comments caught my eye:

I agree with all three comments. Nonetheless, it might be helpful to explain this issue in my own way. Here are three claims:

1. There is no such thing as the “true” elasticity of aggregate demand.

2. It is possible for aggregate demand to be appropriate, even when NGDP growth is unusually high.

3. In this particularly case, however, the fast growth in NGDP is indicative of excessive AD.

Let’s take the three claims one at a time:

1. I prefer to define AD as a rectangular hyperbola, where at each point along the AD curve the total nominal expenditure (i.e., P*Y) is exactly the same. In that case, the elasticity of aggregate demand is always exactly one. But many economists define AD in a different fashion, and end up with a different estimate of the elasticity of aggregate demand. So if someone asked me, “What’s the actual elasticity of AD?” I’d respond, “How are you defining AD?” It depends what you are holding constant along a given AD curve.

2. Suppose Kuwait’s NGDP is 50% oil and 50% other goods and services. Also assume that 5% of Kuwaiti workers produce oil and 95% of Kuwaiti workers produce other goods and services. Now assume that global oil prices double almost overnight. Should Kuwait’s central bank maintain a stable NGDP? I’d say no, as doing so would require a big reduction in non-oil nominal output. Because 95% of workers are in the non-oil sector, and because nominal wages are sticky, this would result in much higher unemployment. It would probably make more sense for Kuwait to target aggregate nominal labor income.

3. Clearly the Kuwaiti example has some bearing on the recent events in the US. We produce a lot of oil and the price of oil has recently doubled. Nonetheless, the recent NGDP data in the US does seem to correctly indicate that there is excessive aggregate demand. We know this because we also see signs of excessive demand in other indicators such as rapid nominal wage growth and high job vacancies, which are not distorted by oil prices.

To conclude, fast growth in NGDP doesn’t always signal excessive AD. But in the case of the US, fast and above trend NGDP growth is almost always is an accurate signal of overheating.

We shouldn’t be wasting time trying to figure out some mythical concept like the “true” elasticity of AD. Instead, we should focus on what sort of path of nominal spending produces a stable economy.

READER COMMENTS

Roger Sparks

Jul 19 2022 at 12:04am

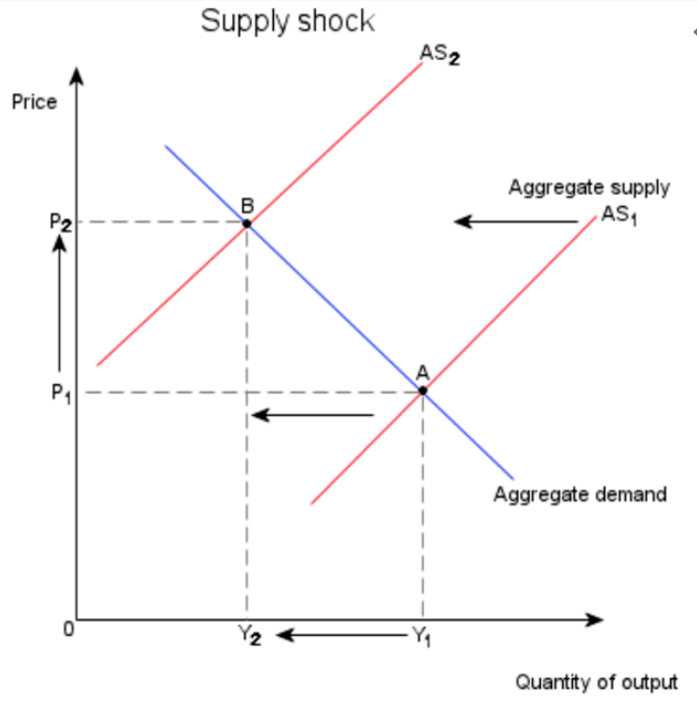

Let’s think through the AD-AS model logically.

The intersection of the AD-AS curves defines GDP. This point resets with every GDP measurement. It is the only measured point on the graph.

The two AD-AS curves represent the opposite reactions to price displayed by buyers and suppliers.

Debt plays a big role in setting the location of the GDP point. Increased levels of debt absorbed by government can fund purchases(demand) by consumers or business expansion. Increased government debt can fund lower prices needed by suppliers (how about the covid vaccine?).

If we only looked at food sales, we could probably make a reasonable estimation of the slopes of both AD-AS curves. I’m not sure how we could predict the slopes when government plays a large role in supporting fundamentals underlaying both curves.

I am thinking that, with only one known point on the graph and debt playing a role in both curves, we can draw the curves with a lot of freedom. I wholeheartedly concur with your concluding recommendation.

John Hawkins

Jul 19 2022 at 4:53am

Your explanation in (2) makes it sound like you’re theoretically in favor of a “productivity norm” (perhaps with positive drift to handle micro- issues with labor contracts), but then settle for practicality’s sake on NGDP targeting, is that fair?

Scott Sumner

Jul 19 2022 at 12:38pm

The Kuwait hypothetical also creates problems for a productivity norm. I’d prefer something closer to per capita nominal labor income.

Daniel R. Grayson

Jul 19 2022 at 8:25am

Re: “I prefer to define AD as a rectangular hyperbola”

Shouldn’t AD be a number?

Henri Hein

Jul 19 2022 at 12:26pm

Yes, but an unknown number is a shape.

Scott Sumner

Jul 19 2022 at 12:39pm

“Shouldn’t AD be a number?”

Yes, that’s my point. It’s P*Y.

Kevin Erdmann

Jul 19 2022 at 1:26pm

Huh. Forward inflation expectations and job openings really have trended right together.

https://fred.stlouisfed.org/graph/?g=RX1z

David S

Jul 20 2022 at 9:29am

Interesting graph. Since I’m a dumb chartist I want to believe that the recent curve downward is a consistent correction in the labor markets. As the big grey band of the Great Recession shows, that “correction” can be wicked bad if prolonged.

Comments are closed.