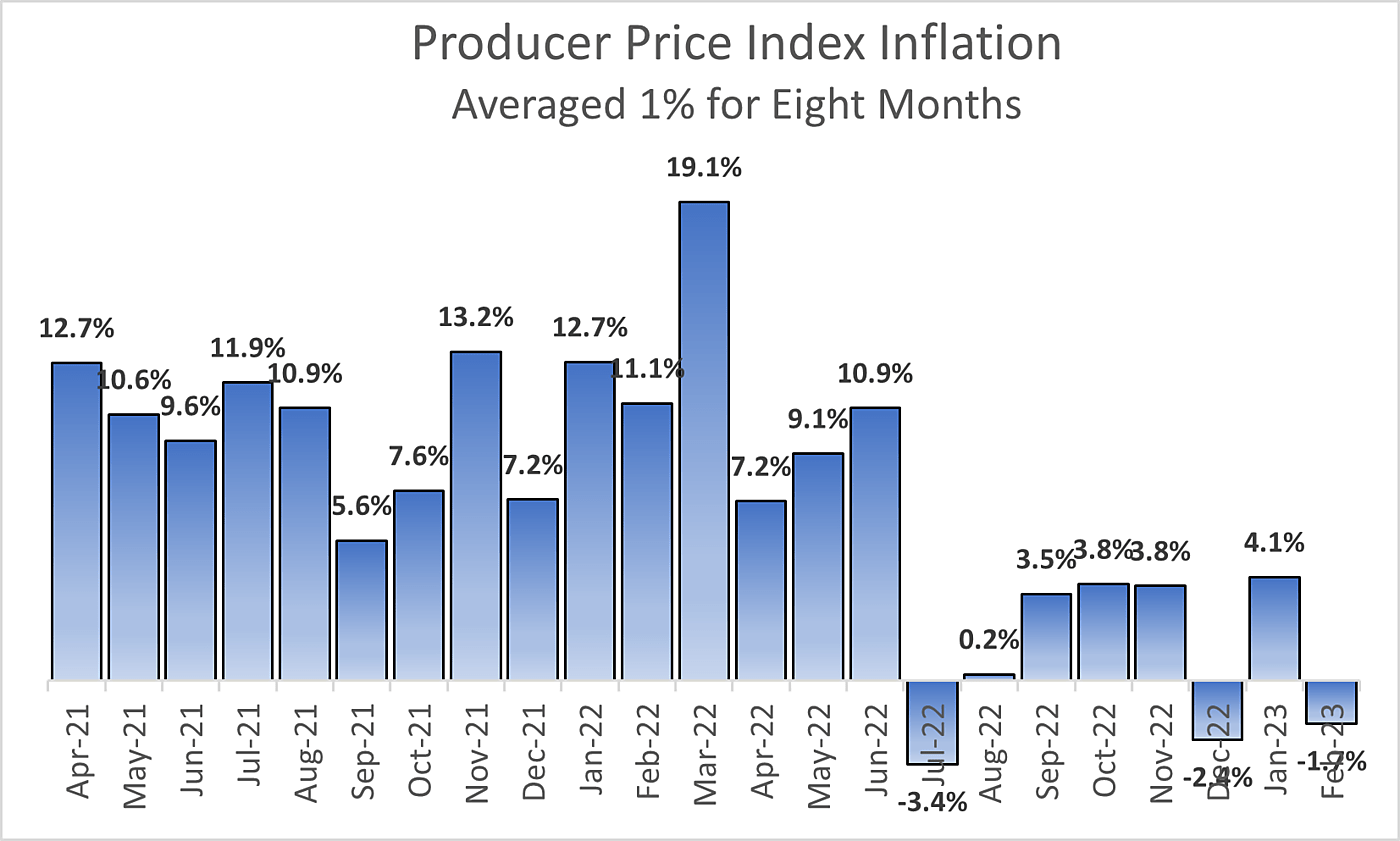

Cato Institute economist Alan Reynolds points out, in “Producer Price Inflation Averaged One Percent for Eight Months,” Cato at Liberty, March 21, 2023, that, as the title suggests producer price inflation is very low.

So why does inflation measured by the Consumer Price Index look so high?

Reynolds explains:

Although market rents have been falling since last summer, BLS estimates of rents on old and new leases still keep soaring in CPI monthly reports—at a 9.6 percent annual rate for the past three months!

That statistical snafu made inflation in 2021 look lower than it really was, because shelter inflation was largely based on depressed 2020 pandemic rents. Today, the lagged BLS rent estimates have the opposite effect of greatly exaggerating inflation in early 2023 because reported shelter inflation (a third of the CPI) is still largely based on leases from the peak inflation of early 2022.

Once we exclude shelter from CPI inflation, the resulting “CPI less shelter” is about like the PPI. CPI‐less shelter has averaged just 1.1 percent since last June, as shown in my March 14 blog post.

This is astounding. Unless Alan has, or I have, overlooked something, this means that inflation is already quite low.

READER COMMENTS

Scott Sumner

Mar 21 2023 at 7:33pm

I do think there’s been a brief lull in high inflation, but I would urge caution.

One way of thinking about this sort of exercise is as a way of predicting future inflation. Thus measured housing inflation will likely come down over time, reflecting the recent decline in “spot rents”. But if we use that approach, we would also note that goods inflation is likely to rise. Part of the low inflation in recent months has been a big drop in goods prices due to the ending of supply bottlenecks and lower oil prices. Those prices are unlikely to continue declining, at least at such a rapid pace.

The (fast-rising) NGDP figures suggest that the underlying rate of inflation (when all the noise is removed) is still way too high.

David Henderson

Mar 22 2023 at 10:43am

I think you’re right. My only point here is to report the facts: the CPI is very misleading.

Alan Reynolds

Mar 22 2023 at 8:16pm

Nominal growth of Final Sales to Private Domestic Purchasers is a relevant measure of domestic demand which excludes government spending, ephemeral inventory swings and foreign demand. Final Sales to Private Domestic Purchasers (LA0000031Q027SBEA) | FRED | St. Louis Fed (stlouisfed.org)

It slowed to a 3.9% annual growth rate in Q4-2022, down steadily from 10.2% in the first. Do advocates of a more-inclusive NGDP target prefer a growth rate lower than 3.9%? Would they regard one or two quarters as a transitory “lull” and ask us to wait for a full year before noticing any change?

The only sustained acceleration of prices since June 2022 has been in rent and owner-equivalent rent, which (as even Jay Powell concedes) is a failure of BLS survey and estimating methods, having nothing to do with contemporary demand (NGDP) or current home prices or rents. Such Shelter is a third of the CPI and 42% of Core CPI.

https://www.cato.org/sites/cato.org/files/styles/pubs_2x/public/2023-03/CPI%20LESS%20RENT%20AVERAGED%201.1%25%20FOR%208%20MONTHS.png

I welcome any criticism of any facts I present. But ignoring them is not helpful.

Andrew_FL

Mar 22 2023 at 10:26am

In addition to what Scott said, I would add that the PPI seems to be very sensitive to oil prices. The PPI “Final Demand” indices show much less dramatic swings and especially Final Demand less Energy. Both do suggest inflation has slowed down significantly since last March, but with nominal demand still strong it’s too early to be confident that high inflation is gone just yet.

David Henderson

Mar 22 2023 at 10:44am

True.

Alan Reynolds

Mar 22 2023 at 8:35pm

Opinions about fact are not facts. My graph was the PPI for Final Demand – it forms an important part of the PCE Inflation estimates.

Taking out food and energy leaves monthly PPI inflation volatile (as in my graph) but still very low on average since August. Producer Price Index by Commodity: Final Demand: Final Demand Less Foods and Energy (PPICOR) | FRED | St. Louis Fed (stlouisfed.org)

For those who insist on measuring inflation as a year-to-year 12-month average, excluding energy will now hugely distort the numbers from March to August because crude oil was way above $100 last year and closer to $70 lately.

Switching to core now (Powell begged us not to do that last June) is almost fraudulent.

Spencer

Mar 22 2023 at 11:42am

2% inflation? Nice try.

Eric J Pentecost

Mar 26 2023 at 4:55am

Cost push inflation can not be fixed by raising interest rates, without raising unemployment. Indeed raising interest rates to cut demand pull inflation only really works in the longer term, by appreciating the pound which depresses foreign demand for our goods and by hitting thr housing market.

Comments are closed.