In a recent podcast with David Beckworth, Noah Smith argued that macroeconomics was still in its infancy. Smith suggested that we needed stronger microfoundations in order to develop rigorous scientific models of the economy.

I have a different view. Old Keynesian economics reached a dead end in the 1970s. This led to two major innovations—the expectations revolution and the push for microfoundations. The New Keynesian economics that developed in the 1980s did a much better job of accounting for expectations of variables such as inflation. Since then, various studies have tried to develop strong “microfoundations”, which means a better explanation of how individual people make decisions to consume, save, invest, and work.

Nonetheless, I don’t see much evidence for progress in macroeconomics, at least if you define macro as developing useful general equilibrium models of the macroeconomy. Instead of being in its infancy, macro seems to be suffering from senility. In my view, things have reached a dead end and further progress would be more likely to occur if we abandoned the basic Keynesian framework and adopted an entirely different approach to macro. I’d prefer we stop trying to model consumption, investment, and the other components of spending, and move to a more monetarist approach. I see macro as being analogous to an inefficient conglomerate than needs to be split up into two independent firms. Here’s how I’d do the split:

Macro 1: A model of nominal variables such as the price level or (better yet) NGDP, including short run fluctuations and long run trends.

Macro 2: A model of real GDP and employment, including short run fluctuations and long run trends.

The term “nominal” means in money terms, and my proposed Macro 1 would be policy regime dependent. I’ll give three quick examples:

Gold standard: Back in 1985, Robert Barsky and Larry Summers modeled the price level under a gold standard. Here’s the abstract:

This paper provides a new explanation for Gibson’s Paradox — the observation that the price level and the nominal interest rate were positively correlated over long periods of economic history. We explain this phenomenon in terms of the fundamental workings of a gold standard. Under a gold standard, the price level is the reciprocal of the real price of gold. Because gold is a durable asset, its relative price is systematically affected by fluctuations in the real productivity of capital, which also determine real interest rates. Our resolution of the Gibson Paradox seems more satisfactory than previous hypotheses. It explains why the paradox applied to real as well as nominal rates of return, its coincidence with the gold standard period, and the co-movement of interest rates, prices, and the stock of monetary gold during the gold standard period. Empirical evidence using contemporary data on gold prices and real interest rates supports our theory.

A greatly underrated paper.

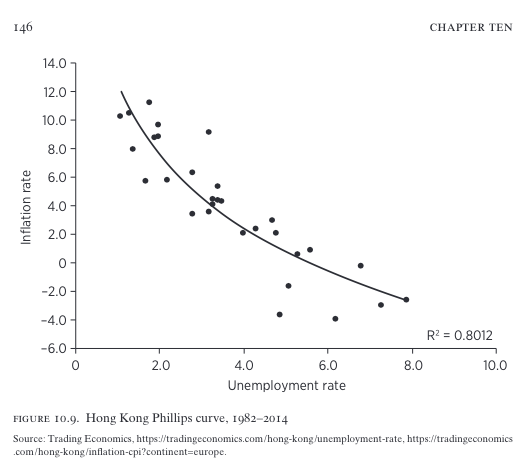

Fixed exchange rate regime: Under a fixed exchange rate regime, global shocks can impact the equilibrium real exchange rate. If the nominal exchange rate is fixed by the government, then the domestic price level must move to generate the appropriate move in the real exchange rate. This model applies to Hong Kong in the post-1983 period.

Unconstrained fiat regime: This is the one that most of us care about. I prefer the market monetarist model, where Fed policy determines the path of nominal aggregates such as NGDP. Even if not directly targeting NGDP, achievement of the dual mandate requires fairly stable growth of NGDP, at roughly 4%/year. Large fluctuations in NGDP growth are caused by monetary policy errors (except in the rare case where much lower employment is desired, i.e., the spring of 2020.) The Fed determines the trend rate of NGDP growth, which means that undershoots like 2008-09 and overshoots like 2021-22 are caused by Fed policy mistakes. Consumption, investment, fiscal policy, trade, animal spirits, etc., play almost no role in determining the path of NGDP. It’s all about monetary policy targets and policy mistakes.

After completing a course in macro 1, students can move on to macro 2. The path of NGDP then becomes an input into the determination of real variables such as RGDP and employment. Due to sticky wages and prices, NGDP shocks affect real variables in the short run, but not the long run. Other “real” shocks (wars, Covid, oil embargoes) can also affects RGDP in the short run. Only real factors such as population and productivity growth explain RGDP growth in the long run.

What’s left to be done? To achieve a better monetary policy, we need to develop financial instruments linked to the key macro variables such as NGDP, traded in highly liquid markets. These real time market forecasts can then guide monetary policymakers.

How about the real side of macro? How to we make progress in that area? Here I’d emphasize that we cannot make progress on understanding real shocks until we can measure them. And we cannot measure real shocks until we can eliminate nominal shocks. For instance, Noah Smith believes that 2008-09 was a real shock—a severe financial crisis caused the Great Recession. I believe it was a nominal shock—a tight money policy by the Fed caused NGDP growth to fall from its 5% trend to negative 3%. In my view, the financial crisis was 75% endogenous. Until we get a monetary policy that produces stable NGDP growth, we’ll never be able to figure out who’s right. We won’t be able to determine how much of the business cycle is real and how much is due to nominal shocks. Take away the nominal shocks and what’s left of the cycle is real.

Macro will have grown up and become a mature field when all we teach is real business cycle theory. Not because RBC theory is correct (it’s currently false), rather because it will have become correct.

PS. Smith rightly mocks the NeoFisherians for suggesting that a low interest rate policy is a tight money policy. But the Keynesians are equally guilty when they claim that a low interest rate policy is an easy money policy. If Turkey refutes NeoFisherianism, doesn’t Japan refute Keynesianism? Interest rates are not monetary policy. Never reason from a price change.

PPS. You might wonder if I have any empirical evidence to support my thesis that macro should split into two fields. If I am correct, then the Phillips Curve should apply to the gold standard and to Hong Kong, but not to the post-1968 fiat money regime in America. And that’s exactly what we find. Phillip’s study looked at the relationship between inflation and unemployment during a period where the price of gold was mostly fixed. The same sort of relationship holds for Hong Kong post-1982:

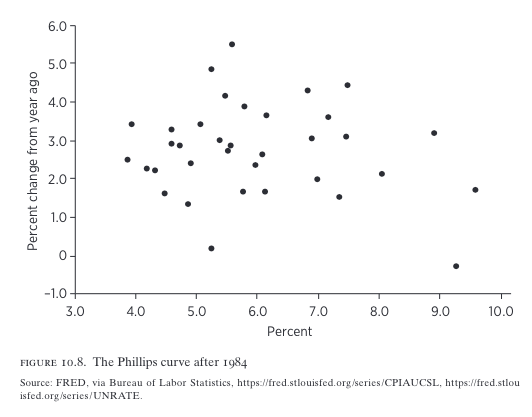

But the relationship doesn’t hold for the US in recent decades. The Fed has been trying to eliminate demand shocks, making real shocks relatively more important:

Again, never reason from a price (level) change.

READER COMMENTS

John Hall

Dec 11 2022 at 10:22pm

Great post.

I spent a little bit of time recently looking into how DSGE models incorporate money. They aren’t that impressive. Money in the utility function approaches capture that people hold real cash balances, but I don’t think that’s really the capturing the actual behavior. Cash in advance models seem to make a little more sense, but it really isn’t just that some goods are cash goods. Every non-barter transaction involves money.

One other approach is so called New Monetarism, which tries to have better micro foundations for money that result in it existing endogenously. The latest models have a centralized market that is like a current DSGE with a decentralized market added on where money is allowed to develop endogenously. However, these models don’t seem to be much better than DSGE models since the decentralized market is small.

So neither approach is really all that great, but I like that the New Monetarists are trying to come up with stronger micro foundations for money. The problem is that any model that includes money with a special role also needs to take into account monetary and fiscal policy.

D F Linton

Dec 12 2022 at 7:58am

Isn’t path-dependence also a real factor? If a nominal shock destroys a company or a product or redirects a career, won’t than change the future of RGDP?

Scott Sumner

Dec 12 2022 at 1:44pm

All models abstract from reality in some ways. Path dependency exists, but I’m not sure it has important policy implications. If anything, it supports the argument for level targeting.

D. F. Linton

Dec 13 2022 at 8:58am

You said “Due to sticky wages and prices, NGDP shocks affect real variables in the short run, but not the long run” not “In this simplified model, …” or even “…but in the long run the effect is thought to be negligible.”

Scott Sumner

Dec 13 2022 at 12:28pm

Fair point.

Todd Ramsey

Dec 12 2022 at 9:15am

Clear, well-explained post. Thank you.

Spencer

Dec 12 2022 at 10:48am

There’s a lot of confusion between micro and macro. Take the FRB-STL:

…

“When deposits are removed from the banks, the banks have less money to lend, and liquidity dries up.” From the St. Louis FED – “Liquidity Dries Up”

…

If there was only one bank, analogous to the system, the shifting / shuffling of deposits has no effect on the aggregated data. The liquidity and solvency of an individual bank is at odds with the liquidity and solvency of the system, of the distribution of reserves.

…

On a macro level, savers never transfer their savings outside the banks, unless they are hoarding currency or convert to another national currency, e.g., FDI.

…

Unlike the nonbanks, the commercial banks suffer no disintermediation when savers decide to shift their savings to another type of investment. Shifting from time deposits in the commercial banks to nonbank types of investments has no effect on the total assets or the volume of earning assets of the commercial banks. It merely involves a transfer in the ownership of pre-existing deposit liabilities, from time to demand deposits within the payment’s System.

Spencer

Dec 12 2022 at 10:55am

re: “Only real factors such as population and productivity growth explain RGDP growth in the long run.”

…

That, of course, is false. The utilization of bank credit to finance real investment or gov’t deficits does not constitute a utilization of savings since bank financing is accomplished by the creation of new money.

…

Lending by the banks is inflationary. Lending by the nonbanks is noninflationary. Thus, lending by the banks increases nominal variables. And lending by the nonbanks increases real variables.

Michael Sandifer

Dec 12 2022 at 1:06pm

My model for imputing NGDP growth in stock prices is part of what led me to the conclusion that the US economy may not have been in equilibrium for decades. Now, on today’s Macro Musings podcast, Joe Gagnon discusses a new working paper that makes a very similar argument.

https://macromusings.libsyn.com/joe-gagnon-on-25-years-of-excess-unemployment-and-the-phillips-curve-debate

As I’ve said for years, I think my model has a chance to become standard macro at some point, though even if Gagnon is correct, it doesn’t necessarily mean my model is valid.

I just happened to touch upon this issue a bit in my blog post last night, complete with an SRAS/SRAD graph. It’s nice to finally see an economist address whether we should take this model literally and seriously.

Monte

Dec 12 2022 at 4:14pm

Macroeconomics is ageless. Different schools of thought may fall out of fashion and stagnate, but then a familiar pattern emerges: A major event takes place (Industrial Revolution, Great Depression, stagflation), a book is written, a star is born, and a revolution occurs (ie. Classical economics, Keynesianism, monetarism). Rinse and repeat.

Prof. Sumner’s proposed re-modeling of the Keynesian framework in macro is interesting, but what economics needs now more than anything else is a scientific revolution that could potentially bring it closer to a hard science. Might A.I. be the answer?

Thomas Lee Hutcheson

Dec 13 2022 at 7:00am

Wasn’t the sharp fall in price expectations in early 2020 a Fed error? And which we saw in the development of shortages rather than price spikes for items in “shortage?”

Thomas Lee Hutcheson

Dec 13 2022 at 7:03am

Aren’t “shocks” anything that cause large shift in relative prices to equilibrate?

Scott Sumner

Dec 13 2022 at 12:30pm

I’d say that’s one effect of shocks.

Thomas Lee Hutcheson

Dec 13 2022 at 4:21pm

But the one that the central bank has to accommodate by allowing the price level (average of all prices) to rise given some prices are downwardly sticky?

Scott Sumner

Dec 14 2022 at 12:00pm

They should ignore the price level and focus on slow but steady NGDP growth.

Comments are closed.