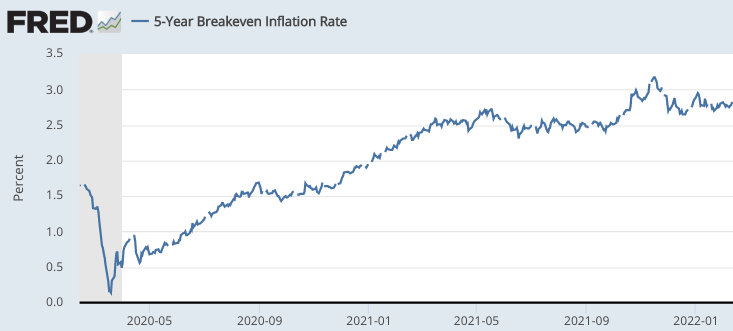

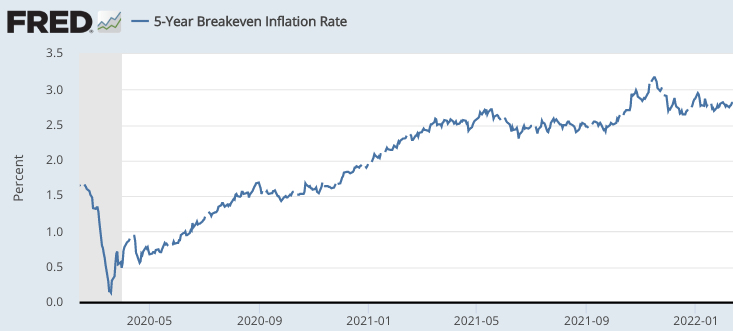

Many people are surprised by my claim that monetary policy is gradually getting more expansionary, even as interest rates start to rise and QE is being scaled back. But these instrument settings don’t tell us much about the stance of monetary policy. Instead, we need to look at the goal variables. The 5-year TIPS spread has been fairly stable over the past 10 months, at a relatively high level:

If the Fed were an inflation targeting central bank, then this would suggest little change in the stance of monetary policy over the past 10 months. But the Fed is not an inflation targeting central bank; it’s an average inflation targeting central bank. And the expected average inflation rate during the 2020s has been rising in recent months.

The actual PCE inflation rate over the past year is 5.8%, far above the Fed’s 2% target. To make this high inflation “transitory”, inflation must average roughly 1.6% during the other 9 years of the decade. Inflation was quite low in 2020 (1.3%), so we need about 1.7% per year for the rest of the decade. This means that the gap between expected PCE inflation (about 2.6%, equivalent to 2.85% for the CPI) and the appropriate target (about 1.7% PCE inflation) has been widening over the past 10 months. Unfortunately, Fed chair Powell has recently seemed to waver on the Fed’s average inflation targeting commitment, suggesting that they have no intention of balancing years of above 2% inflation with periods of below 2% inflation. This could lead to a dangerous loss of credibility in Fed policy.

This is not to suggest that inflation averaging 2% for the rest of the decade would be a policy disaster; that would still be a better outcome than most previous decades. But the longer the Fed waits to get inflation under control, the more painful will be the adjustment process. Policy credibility is the Fed’s most powerful policy tool. Without it things get much more difficult.

READER COMMENTS

Rodrigo Escalante

Feb 12 2022 at 7:26pm

Should we expect an emergency rate hike from the fed? Is it something they would do? It would seem a bit odd that they hold an emergency meeting and decide to do nothing. Is this our 2008 post Lehman fed meeting moment? Is the fed on its way to being stuck in a 1970s? My father who is about your age still believes that as the fed raises short term rates longer term rates should follow. I try to explain the oposite should happen if the fed were engaging in policy tightening but I am afraid the outcome of the next meeting might be exactly that if they only do 25bps and keep with their transitory rhetoric.

Scott Sumner

Feb 12 2022 at 7:36pm

Yes, many people are confused on that point.

David S

Feb 12 2022 at 7:30pm

The topic of Fed mistakes on Scott’s bad blog and good blog seemed to have converged, but that’s okay–I think shouting from the rooftops is appropriate. I’m resigned to a Fed engineered recession at some point this year or next year. Sooner and milder would be better than later and harsher.

It’s curious how the history of Fed policy over the last 6 months, and probably the next 9 months, might turn out to a near mirror image of 2007-2009. The Bernanke Fed focused on the wrong signals and ran money too tight for too long. The Powell Fed is doing nearly the exact opposite, and not giving clear signals that the foot-dragging will change to firm actions. Why the hell is QE still running? Why didn’t Powell adopt a more hawkish tone in November? Or December? Or January?

And for anyone who says that monetary policy is useless, look at the Economist article on Uganda—granted, not a wonderful country in many ways, but if they could drop inflation from 200% to 2% in the space of a few years we should be able to drop PCE from 6% to 3% in a few months. We can’t rely on anti-vax truckers in Canada to cool things down.

Scott Sumner

Feb 12 2022 at 7:37pm

I have a new piece coming out at the Hill explaining why the Fed screwed up.

BC

Feb 13 2022 at 3:11am

“It’s curious how the history of Fed policy over the last 6 months, and probably the next 9 months, might turn out to a near mirror image of 2007-2009”

Very long term average inflation targeting. 🙂

Andrew_FL

Feb 13 2022 at 9:42am

December 2021 PCEPI is exactly on 2% trend if you start your trend line between August & September 1990! 😉

Max More

Feb 13 2022 at 6:29pm

They are not anti-vax truckers. They are anti-vax mandate truckers. Why do people have such a hard time making this distinction?

Laron

Feb 12 2022 at 8:42pm

I don’t disagree but doesn’t this also depend on the details of “average”? I don’t recall if the Fed clarified the time duration or frequency of the average calculation, or did they?

I worry that Powell et al will just fall back on whatever calculation is politically expedient at the time no matter how bad it gets.

Scott Sumner

Feb 12 2022 at 10:39pm

Laron, The problem with that view is that the policy would then be completely ineffective. In that case, we’d be back to simple inflation targeting. That may happen, but the Fed would not then be able to claim success.

BC

Feb 13 2022 at 3:17am

That was the problem with not defining what “flexible” meant. It seems like the less clarity, the more discretion that the Fed could retain, but also the less credible the policy. The Fed seems to like to retain flexibility/discretion.

Laron

Feb 13 2022 at 1:25pm

Yup, that’s exactly my concern.

vince

Feb 13 2022 at 3:02pm

Rightfully. Abracadabra! The Fed chooses Sept 2008 as the starting point. To January 2022 the average inflation rate is 1.9%!

Craig

Feb 13 2022 at 5:49pm

“The 5-year TIPS spread has been fairly stable over the past 10 months, at a relatively high level”

At a high level, but still well below the current 7.5% Y/Y CPI reading. Actually I would love to see a chart of 5 year breakeven vs. CPI over the past 20 years. Look at the bond market they say, the bond market doesn’t really expect much inflation given this fact, ie the fact that the breakeven is below the CPI. Meanwhile if somebody bought a 1 year a year ago they got absolutely hammered. [Who’s buying these bonds? I wouldn’t buy these bonds at the current nominal yields if inflation were guaranteed to be zero. As an aside the interest is taxable too] The asset purchases as of February 13th, 2022 continue. The current breakeven rate is the result of a negative yield input (TIPS) and a slightly positive yield 5 year coming up with the bizarre situation where the market is expecting inflation above the yields of the bonds they’re buying. The problem with looking at the bond market as a barometer of inflation and of future market expectations of inflation in the face of QE is that the prices of the bonds are being directly manipulated by the Fed itself. As a result, the bond prices carry with them fundamentally less useful information since they are not the result of a genuine market process. Let’s not fight the Fed, can’t win that fight, so let’s play another game of “Let’s guess what JP will do next” Will the Fed defend the dollar, will the taper cause the tantrum? We’ll see, but at the end of the day it seems obvious to me the world’s largest debtor is playing a game of “Let’s see how much of a haircut we can give our creditors.” Ultimately that is what JP has been doing; he’s the US’ biggest asset, he’s been selling real negative interest rate bonds and I suspect they’re going to keep doing that until the bond vigilantes show up and say, “Yeah….no….no thanks” #deadbeatnation

Chris Oldman

Feb 14 2022 at 9:39am

Your thoughts on monetary policy are always interesting. I’m curious, though, do you really believe (and does the market believe) the Fed’s policy is to average inflation over any specific period, as you’ve said? My impression when they made the change, was more that their policy was changed from ‘We’re shooting for as close to 2% inflation without going over’ to ‘We’re shooting for as close to 2% inflation as we can get.’

Scott Sumner

Feb 15 2022 at 6:12pm

I do think they were shooting for above 2% inflation in 2021, to make up for the low inflation in 2020.

Devin Lavelle

Feb 15 2022 at 4:16pm

What’s the time horizon we are targeting for it to average out over?

The average inflation over the past 5 years has been a modest 2.23% Over the last 10 years, it’s been 2.07%. Those figures include 2021’s high inflation. The 9 years prior to 2021 averaged 1.67%.

(https://www.minneapolisfed.org/about-us/monetary-policy/inflation-calculator/consumer-price-index-1913-)

Why shouldn’t we just consider this period to be evening out over the prior periods when the country fell short of its average inflation target?

Scott Sumner

Feb 15 2022 at 6:11pm

I believe it makes sense to start the clock at the beginning of 2020. I recall a Fed official said something similar.

bill

Feb 15 2022 at 6:19pm

The highlight below is mine. I wonder how the Fed really interprets the commitment we thought it made?

https://www.stlouisfed.org/on-the-economy/2021/july/inflation-expectations-fed-new-monetary-frameworkKey paragraph: Perhaps more than ever, this strategy requires the Federal Reserve to pay attention to inflation forecasts, particularly with an eye toward any indications that inflation is rising above 2% and perhaps staying there, on average, for longer than desired. As an example, suppose that inflation were currently predicted to average above 3% for the next five years. While FAIT doesn’t explicitly define the time frame over which inflation is averaged, five years seems to be too long, and we would expect the Federal Reserve to eventually enact tighter monetary policy to prevent this from occurring.

Comments are closed.