The Great Inflation lasted from 1966 through 1981, or perhaps the early 1990s, if you wait until inflation had reached a roughly 2% trend. But I’ll focus on 1982 as the traditional end date for the Great Inflation.

Soon after the Great Inflation got underway, policymakers began looking for solutions. Ever since 1934, the $35/oz. gold price peg had provided a sort of anchor for prices. Yes, it was a weak anchor, as the gold standard was gradually being dismantled, but it still had some ability to hold down inflation expectations. Once that price peg was lifted in March 1968, LBJ looked for alternative solutions. His first choice was MMT. Then Nixon tried statism (or socialism, if you want to troll the Sanders/AOC supporters). Then Carter tried Keynesianism. They all failed. Then Reagan tried monetarism. He succeeded. This is their story.

In 1968, LBJ raised taxes sharply as a way to slow inflation, the MMT solution. In one sense this policy was a smashing success, as the budget swung into surplus during the 1968-69 fiscal year (which went from July to July in those days). That was a mind-boggling accomplishment at the time. When does a country balance its budget in the midst of a major war, and when it is also rapidly scaling up the “Great Society”? (Everything from expanded welfare, to Medicare, Medicaid, housing programs, moon landing, etc.) That’s crazy!

Unfortunately, it was a complete failure at holding down inflation, which continued to accelerate. That’s because it was based on the false model that fiscal policy determines inflation, whereas in fact it is monetary policy that determines inflation.

In August 1971, Nixon adopted wage/price controls. These did briefly slow measured inflation, but by 1973, inflation was soaring to new highs even as shortages were developing. Nixon ended the controls during 1974. (And no, the 1972-81 inflation was not about oil, as NGDP grew at 11%/year and RGDP grew by a bit over 3%/year. It was money.)

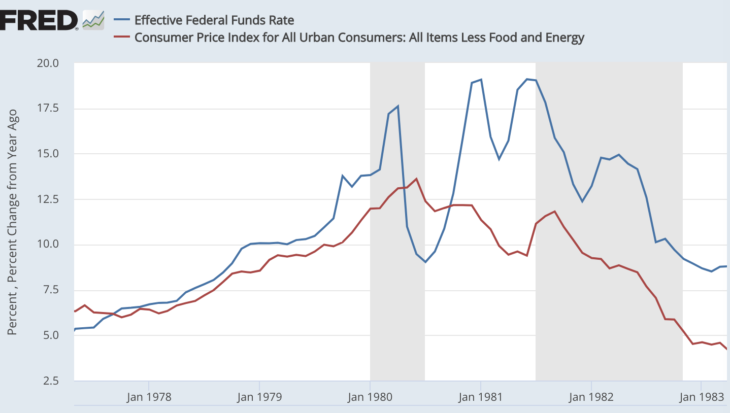

During 1979-81, Carter’s Fed adopted a high interest rate policy to control inflation. Almost everyone in the world, both left and right, gets this wrong. They draw a sharp break between the period before August 1979, when G. William Miller led the Fed, and the next 8 years, when Volcker led the Fed. Actually, the 1979-81 policy that led to America’s highest inflation rates since WWII was produced by both Miller and Volcker; the actual policy break toward tight money occurred in mid-1981.

Keynesians have a bad habit of reasoning from a price change, assuming that inflation comes from an overheating economy (it comes from easy money), and they also have a bad habit of assuming that high interest rates represent tight money (sometimes, not always). They wrongly see high interest rates as a way to control inflation. That’s like saying “High oil prices are a good way to reduce oil consumption.” Not if the high oil prices are caused by public policies that boost oil demand. People need to stop reasoning from a price change.

During 1979-80, the high interest rates were caused by an easy money policy, which boosted interest rates via the income and Fisher effects (mostly the latter.) That’s why this Keynesian policy failed. For you econ nerds, the Fed shifted the IS curve to the right (via bad signaling), boosting interest rates, while it wrongly believed that it was shifting the LM curve to the left, an alternative way to create high interest rates.

The Volcker policy failed so spectacularly that NGDP growth reached an annual rate of 19.2% during 1980Q4 and 1981Q1. Those are Latin American rates. You might argue that it was just a question of giving the policy enough time to work. After all, inflation did eventually come down. But that argument won’t fly, as even the financial markets were freaking out about high inflation. Thirty-year bond yields reached nearly 15% in mid-1981, as people lost all faith in the future value of the US dollar. Policy may affect inflation with a lag, but it affects market expectations immediately.

Then in mid-1981, Volcker switched to a tight money policy. Monetarists had told Volcker to forget about interest rates and control the M1 money supply. That’s still not a good policy, but it’s far less bad than targeting interest rates during high inflation periods. By late 1981, the monthly inflation numbers had fallen to about 5%, and by late 1982 we had reached the 4% range maintained throughout the remainder of the 1980s. The Great Inflation was over. Monetarism ended the Great Inflation.

When there is high inflation, the world will always (eventually) turn to monetarism for an answer. In the early 1920s, hyperinflation roared through several European countries. Wicksell and Keynes suddenly stopped talking about monetary policy in terms of interest rates and starting talking about the money supply as the key variable. Keynes’s Tract on Monetary Reform of 1923 is a monetarist book.

[I mention Wicksell and Keynes, as they are the two most important advocates of the interest rate approach to monetary policy in all of world history.]

So there are lessons here. If you want to control high inflation, do not rely on tax increases (MMT), price controls (statism) or high interest rates (Keynesianism). Rather, adopt a tight money policy. That always works, and it’s the only policy that works. Tight money might raise interest rates, or it might lower rates (as in Switzerland during January 2015), but it will always lower inflation.

PS. There is some debate over the actual “concrete steps” used by Volcker to control inflation, an issue people obsess over far too much. The monetarists recommended money supply targeting at a steady growth rate, but Volcker did not in fact adopt that policy. M1 money growth did slow during the period from April 1981 to mid-1982, however, which is when inflation came down. What’s important is that Volcker’s Fed adopted a tight money policy in mid-1981, and that this is what brought inflation down. Interest rates, M1, exchange rates and all the rest will adjust as needed, as long as you adopt a tight enough policy to control inflation.

PPS. If you insist on concrete steps, here’s one option. Do enough open market sales of bonds until market expectations of inflation fall to your target range. (Obviously I’d prefer NGDP targeting over inflation targeting.) Let interest rates go wherever they want to go.

READER COMMENTS

Brian Donohue

Mar 6 2019 at 2:22pm

Excellent!

Benjamin Cole

Mar 6 2019 at 7:21pm

Aside from the little bit of Reagan hagiography, this was an accurate post .

Ronald Reagan was displeased enough with Volcker to publicly propose that the Federal Reserve be placed into the Treasury Department where it would answer to presidential directives. I happen to agree with Reagan on this particular proposal.

It is also worth remembering that as measured by the PCE deflator, annual inflation rates never got up much above 9% in the 1970s and 80s. Also, back then, many “serious” people thought any inflation rate below 5% or perhaps 4% was good enough.

The curious peevish fixation on a minute rate of inflation, at least among American economists ( not so much in China or Australia) happens later, in the late 1990s and 2000s, and then became orthodoxy.

In the mid-1990s, Milton Friedman chastised the Fed for being too tight, when the consumer price index was north of 3%.

Are there any major economies where a central bank’s 2% inflation target has resulted in robust economic growth?

Brett

Mar 7 2019 at 1:27am

Wouldn’t that work under MMT too? There’s no reason why the government running an MMT regime couldn’t have the (presumably politicized) central bank soak up tons of money with bonds with market-set interest rates until expectations drop.

LK Beland

Mar 7 2019 at 11:44am

Great post.

It also ties in nicely with the point that you made about the “hot potato effect”. High-powered money is quite effective when interest rates are high, which explains why monetarism works under those conditions.

Things are a bit trickier at low-to-negative interest rates, as high-powered money becomes ineffective. Under those conditions, market monetarism seems to provide reasonable guidance, as do some new Keynesian models (e.g. target-the-forecast à la Lars Svensson).

jj

Mar 7 2019 at 11:48am

Scott, can you explain this statement further:

So we know there was ipso facto an easy money policy, as seen in the results — high NGDP growth — but what were the signals, OR concrete steps, that defined this policy?

If the market knew the Fed’s objective was to reduce inflation, how badly did Volker mangle the signaling to give the market the opposite idea? Did he say “We want lower inflation; we will achieve this by printing money”? Or was it concrete steps: he said they were targeting higher interest rates, but then secretly told the OMO desk to start buying treasuries instead of selling, kicking things off in the wrong direction?

There’s a nice analogy here with electric motors, by the way. Synchronous AC motors such as the one driving your microwave turntable will randomly turn in either direction when started up, depending on initial conditions. So when you apply power, you know it’s going to start moving, but not which direction it’ll go.

Scott Sumner

Mar 7 2019 at 12:20pm

Brett, You said:

“Wouldn’t that work under MMT too?”

I’m not sure what that sentence means. If you are asking whether MMTers believe it would work, I think the answer is no. I have no idea what an “MMT regime” is, so I can’t comment on that.

JJ, The most important concrete step was increasing the money supply much faster than money demand.

Rajat

Mar 7 2019 at 4:11pm

Actually, MMT can incorporate statism too – bonus!

https://ftalphaville.ft.com/2019/03/01/1551434402000/An-MMT-response-on-what-causes-inflation/

Michael Watts

Mar 7 2019 at 6:29pm

It’s time for me to ask about what appears to be a basic term. Can you tell me what is meant by an “overheating economy”?

Wikipedia says:

Overheating of an economy occurs when its productive capacity is unable to keep pace with growing aggregate demand. It is generally characterised by a below-average rate of economic growth, where growth is occurring at an unsustainable rate. Boom periods are often characterised by overheating in the economy. An economy is said to be overheated when inflation increases due to prolonged good growth rate and the producers produce in excess thereby creating excess production capacity.

I can’t make heads or tails of this. It appears to call a “below-average rate of economic growth” “unsustainable”, but that can’t be true. It says that an economy is overheated when “producers produce in excess thereby creating excess production capacity”… but that overheating occurs when “productive capacity is unable to keep pace with growing aggregate demand”. I would have called those opposite circumstances.

Scott Sumner

Mar 7 2019 at 6:45pm

Michael, You are right that:

“producers produce in excess”

Is a poor definition, very confusing. The other definition (aggregate demand rising faster than productive capacity) is better. But I don’t thin this phrase has any precise meaning, and different people may define it differently

Garrett

Mar 7 2019 at 9:54pm

“Overheating economy” strikes me as a term similar to “bubble,” something people say a lot to each other without realizing they don’t agree on the specific definition.

Scott Sumner

Mar 8 2019 at 10:40am

I agree.

jj

Mar 8 2019 at 6:20pm

Scott, but HOW did the Fed increase the money supply in 1979-80? Was it by OMO in their efforts to raise interest rates? That would be bizarre, the Fed knew that they wanted to be selling T-bills, not buying. And the market knew the Fed knew.

Do you have any data about what exactly the Fed was doing in 79-80?

Comments are closed.