I fear readers will complain that I am beating a dead horse, but I continue to see confusion over monetary policy. In the FT, Andy Haldane has a piece discussing the effectiveness of forward guidance:

Central banks have so far used forward guidance, with a bias to future tightening, to achieve this disciplining effect. And for a fleeting period over the summer, this seemed to be working, with interest rate expectations suggesting rises were more likely than not in the US, UK and eurozone during 2024 and with no rate cuts expected until 2025 at the earliest.

But, like my own attempts with my children, the disciplining effects of these so-called “open mouth” operations has been shortlived. Although central banks’ tighter for longer rhetoric remains largely unchanged, financial markets now expect significant rate cuts in the US, euro-area and UK during the first half of 2024.

I have exactly the opposite view. It is true that if forward guidance were effective, then markets would expect policymakers to maintain a restrictive stance until inflation is under control. But a restrictive stance does not mean high interest rates, it means interest rates above the natural rate.

If current forward guidance is effective, then inflation expectations should moderate. This will cause a fall in the future expected natural rate of interest (in nominal terms), and a reduction in the future expected policy rate.

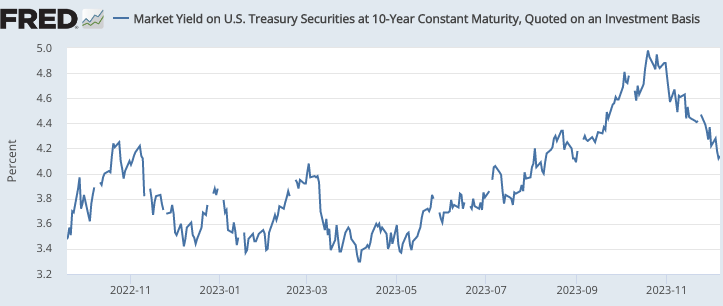

I was more pessimistic about inflation a month ago, when I saw 10-year bond yields rise above 5%. Now that they are back down to 4.2%, I’m becoming a bit more optimistic about the prospects for controlling inflation—and by implication, future rate cuts.

PS. Otherwise, it’s a good article. Haldane does a nice job of discussing the intuition behind the time inconsistency problem. I just think he’s misinterpreted what the recent fall in rates tells us about forward guidance.

READER COMMENTS

Ahmed Fares

Dec 12 2023 at 10:45pm

Maybe it’s just terminology, but from what I’ve read, the central bank sets policy for the neutral rate (short-term r-star), which oscillates around the natural rate (long-term r-star). This from Wikipedia:

Having said that, a mistake that economists make is thinking that other people think like economists. They don’t. The average person has no clue what monetary policy is. They only notice it, for example, when their mortgage renewal comes up, and their 3% interest rate is now 8%. A sample from Canadian media about the upcoming “mortgage renewal cliff”:

So what matters is not just the stance of monetary policy, but how many people are actually affected by it.

Thomas L Hutcheson

Dec 13 2023 at 10:17pm

The neutral rate of interest is an odd concept. Why would the Fed use a model to estimate r* and then use r* to decide on how to set one of many possible policy instruments? Why not go straight to modeling how alternative instrument settings affect the inflation-employment outcomes it is targeting?

It sounds like saying that a driver takes account of vibration of the steering wheel to estimate “bumpiness” and then used “bumpiness” to decide on how hard to push on the accelerator or brake. Doesn’t a driver just take account of vibration the steering wheel to decide how to operate the accelerator or brake? Brad DeLong uses this language but I’ve never seen him explain why.

Ahmed Fares

Dec 14 2023 at 2:58pm

A good Fed article here about r* titled: “Gazing at r-star: Gauging U.S. monetary policy via the natural rate of interest”.

Note the last paragraph, which mentions r**, the neutral rate of interest for the financial markets. There is a risk that you crash into r** before you hit r*.

https://www.dallasfed.org/research/economics/2023/0703

Thomas L Hutcheson

Dec 12 2023 at 11:16pm

If “forward guidance” refers to the future setting of a monetary policy instrument, the EFFR, say, then it is inconsistent with policy setting being data driven and should be avoided. The only “forward guidance about future instrument setting that is legitimate would be “we will set the values of any and all of our instruments at what ever levels at that time that seem in our judgment most like to achieve our target inflation rate.” I’d hope, however, what they really meant was “to achieve a trajectory of real income minimizing inflation rates coming to rest at our target rate that we also believe to be consistent with income maximization.”

Now it might be desirable to share the results of the (implicit) model on which any given Fed announcement is based, on the future instrument settings are currently expected with current exogenous variables and FOMC members’ speculation about future exogenous variables that had lead to the just announced settings and the inflation and employment outcomes the members expect, but that would run the risk of being taken as a commitment to enact those settings even if the values of exogenous variables in the future diverged from those currently expected. In other words it might be mis-interpreted as “forward guidance.”

Bobster34

Dec 13 2023 at 12:07pm

Scott, does this mean that monetary policy does work with lags?

Scott Sumner

Dec 13 2023 at 8:09pm

There are very short lags for NGDP, a bit longer for wages and prices. But lags are far shorter than the media suggests.

Brent Buckner

Dec 14 2023 at 8:29am

And as Dr. Sumner has noted, a significant proportion of what seem to be lags in monetary policy effectiveness may actually be lags in *measurements*:

https://www.econlib.org/good-news-on-inflation-2/

Comments are closed.