Hoover Institution economist (and colleague) John Cochrane has an excellent long post on dollarization in Argentina.

One highlight:

Dollarization is no panacea. It will work if it is accompanied by fiscal and microeconomic reform. It will be of limited value otherwise. I’ll declare a motto: All successful inflation stabilizations have come from a combination of fiscal, monetary and microeconomic reform. (italics in original)

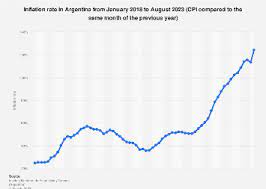

That reminds me of what Michael K. Salemi wrote about what has been learned about ending hyperinflations. He wrote the entry “Hyperinflation” in The Concise Encyclopedia of Economics. While Argentina is far from having hyperinflation, which, as Salemi notes, is typically used “to describe episodes when the monthly inflation rate is greater than 50 percent,” Argentina does have very high inflation, in excess of 100% in the last 12 months. So the same principles for ending hyperinflation apply for ending, or at least substantially reducing, Argentina’s inflation.

Here are Salemi’s two key paragraphs on ending hyperinflations:

How do hyperinflations end? The standard answer is that governments have to make a credible commitment to halting the rapid growth in the stock of money. Proponents of this view consider the end of the German hyperinflation to be a case in point. In late 1923, Germany undertook a monetary reform, creating a new unit of currency called the rentenmark. The German government promised that the new currency could be converted on demand into a bond having a certain value in gold. Proponents of the standard answer argue that the guarantee of convertibility is properly viewed as a promise to cease the rapid issue of money.

An alternative view held by some economists is that not just monetary reform, but also fiscal reform, is needed to end a hyperinflation. According to this view, a successful reform entails two believable commitments on the part of government. The first is a commitment to halt the rapid growth of paper money. The second is a commitment to bring the government’s budget into balance. This second commitment is necessary for a successful reform because it removes, or at least lessens, the incentive for the government to resort to inflationary taxation. If the government commits to balancing its budget, people can reasonably believe that money growth will not rise again to high levels in the near future. Thomas Sargent, a proponent of the second view, argues that the German reform of 1923 was successful because it created an independent central bank that could refuse to monetize the government deficit and because it included provisions for higher taxes and lower government expenditures. Another way to look at Sargent’s view is that hyperinflations end when people reasonably believe that the rate of money growth will fall to normal levels both now and in the future.

My EconLog co-blogger Scott Sumner also has insights about dollarization.

READER COMMENTS

robc

Nov 27 2023 at 9:28am

In a reverse from my comment in the previous article, I thought this was a Scott Sumner piece until I saw the byline.

Did you all swap brains over the holiday weekend?

Thomas L Hutcheson

Nov 27 2023 at 10:37am

It was OK, but seems to ignore the advantage of having an independent monetary policy that can facilitate adjustments in relative prices to real shocks. The whole part about the advantages of a standard of value was just weird. Weights and measures are not SUPPOSED to change with circumstances, the settings of monetary policy instruments are.

Dollarization, notwithstanding its costs however, may be the only way to constrain the production of fiscal shocks that are too big for monetary policy to handle.

Ken

Nov 28 2023 at 10:50am

The dollar may not be the stable value Argentina needs in our ever changing financial world but building to a future constant exchange rate would create immense credibility.

Dave Berry

Nov 28 2023 at 5:07pm

Just to point out that the austerity caused by the reform of the German currency was helpful in the rise of the Nazis and subsequent events.

Jack chia

Nov 28 2023 at 6:31pm

Dollarization is the best solution to stabilize the economy of Argentina by depriving the government of its right to print money at its own will, accompanied by privatizing state-owned enterprises and all government departments better to be run by private enterprises, leaving only those key departments, such as foreign affair, national security and defense, etc. necessarily run by the government to keep the cost of running the government as lowest as possible.

The benefits will enforce any future government to have at least balanced budgets in the years beyond, and force its people free to earn their living without relying on the welfare provided by the government, accompanied by fair and simple taxation system to provide just enough revenue for running the small government.

Welfare should be dealt with by private run organizations, such as churches, food banks, etc.

Retirement benefits should be dealt with by individual employers’ run superannuation fund with equal contributions made by both of employer and its employees based on the laws passed by the parliament.

Education should be all privatized with education vouchers distributed directly to those eligible students funded by private education fund institutions.

In short, it should not rely on the government to do everything for its people, and should instead be dealt with by its people on their own.

It is of course, a huge task but worth to do it!

Umanah

Nov 29 2023 at 6:10pm

I think you are right, Jack! The only worry will be the patience of the people to withstand the pain that has to come before repair is complete. The political will to stay the course will prove challenging to say the least.

Carlos Obiano

Nov 29 2023 at 6:49am

The problem is in the high degree of corruption exhibited during the last 70 years in that country. Everybody is and, in that view follow this comment, and was in any level of the population a wise person, they knew more than the other citizen, how to avoid paying taxes and how to milk the system. Now the gravest of all is coming. “Accountability”

Who will last in their plans to rescue that wonderful country?

Felix Fujishiro

Nov 29 2023 at 2:57pm

I agree, dollarization will not necessarily be a panacea for Argentines, and indeed may bring them unbearable economic pain. Outsourcing their monetary policy to the U.S. Fed has serious risks, since the Fed has no mandate or responsibility for the employment level or to control inflation in any country other than the U.S.

Dollarization would also mean that Argentina would be unable to deflate their currency for competitive reasons. That was the box Greece and Italy were in once they outsourced their monetary policy by converting to the euro. Why wouldn’t we expect that Argentina will experience a similar kind of economic pain that those countries did?

Jim Glass

Nov 30 2023 at 9:46pm

“Argentina’s Milei on Dollarization, Central Bank, China (Full interview in english)” — Bloomberg

https://www.youtube.com/watch?v=fhqq3zDW6E0

Hugely more literate and informed than Trump & Co.

Cynthia Richards

Dec 5 2023 at 11:34pm

Inflation in Argentina is a cheap bonus for other western countries but the peso’s value to the euro or dollar is just the result of Argentina’s governmental policy of free education and medical care for all in addition to its lack of domestic accountability for infrastructure and taxation. The problem lies within.

Comments are closed.